Nordstrom 2011 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2011 Nordstrom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

|

|

Nordstrom, Inc. and subsidiaries 25

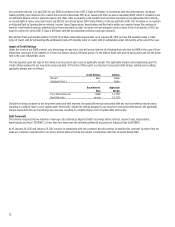

SELLING, GENERAL AND ADMINISTRATIVE EXPENSES — 2010 VS 2009

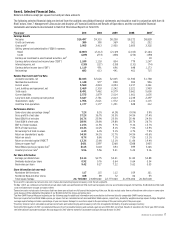

Total Credit SG&A decreased $83 in 2010 compared with 2009, due primarily to lower bad debt expense, partially offset by increases in operational

and marketing expenses. The decrease in bad debt expense reflected continued improvement in our portfolio trends which are further discussed

below. The increase in operational and marketing expenses was primarily driven by increased information technology expenses, higher collection

agency fees from higher recoveries and expenses related to our Fashion Rewards program.

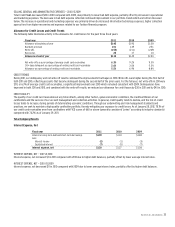

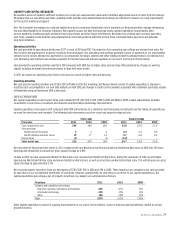

Allowance for Credit Losses and Credit Trends

The following table illustrates activity in the allowance for credit losses for the past three fiscal years:

Fiscal year 2011 2010 2009

Allowance at beginning of year $145 $190 $138

Bad debt provision 101 149 251

Write–offs (153) (211) (209)

Recoveries 22 17 10

Allowance at end of year $115 $145 $190

Net write–offs as a percentage of average credit card receivables 6.3% 9.2% 9.5%

30+ days delinquent as a percentage of ending credit card receivables 2.6%

3.0% 5.3%

Allowance as a percentage of ending credit card receivables 5.5% 6.9% 8.8%

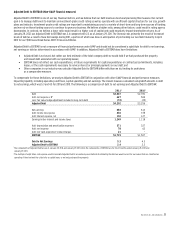

CREDIT TRENDS

During 2011, our delinquency and net write-off results continued the improvements that began in 2010. Write-offs were higher during the first half of

both 2011 and 2010, reflecting accounts that became delinquent during the second half of the prior years. For the full year, net write-offs in 2011 were

$131, or 6.3% of average credit card receivables, a significant improvement over 2010 which remained consistent with 2009. Delinquencies have

improved in both 2011 and 2010, and combined with the write-off results, we reduced our allowance for credit losses by $30 in 2011 and by $45 in 2010.

CREDIT QUALITY

The quality of our credit card receivables at any time reflects, among other factors, general economic conditions, the creditworthiness of our

cardholders and the success of our account management and collection activities. In general, credit quality tends to decline, and the risk of credit

losses tends to increase, during periods of deteriorating economic conditions. Through our underwriting and risk management standards and

practices, we seek to maintain a high quality cardholder portfolio, thereby mitigating our exposure to credit losses. As of January 28, 2012, 78.1% of

our credit card receivables were from cardholders with FICO scores of 660 or above (generally considered “prime” according to industry standards)

compared with 76.2% as of January 29, 2011.

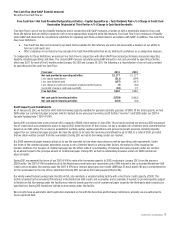

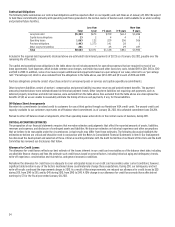

Total Company Results

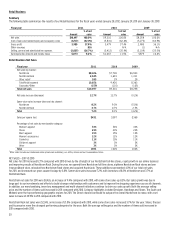

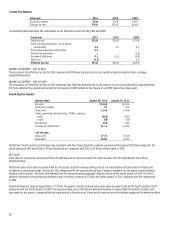

Interest Expense, Net

Fiscal year 2011 2010 2009

Interest on long–term debt and short–term borrowings

$139 $133 $148

Less:

Interest income (2)

(1)

(3)

Capitalized interest (7)

(5)

(7)

Interest expense, net $130 $127 $138

INTEREST EXPENSE, NET — 2011 VS 2010

Interest expense, net increased $3 in 2011 compared with 2010 due to higher debt balances, partially offset by lower average interest rates.

INTEREST EXPENSE, NET — 2010 VS 2009

Interest expense, net decreased $11 in 2010 compared with 2009 due to lower average interest rates, partially offset by higher debt balances.