Nordstrom 2001 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2001 Nordstrom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

|

|

Blk + 1 pms PAGE 21 pms

550

Cyan Mag Yelo Blk

20200324 NORDSTROM

2001 Annual Report • VERSION

8.375 x 10.875 • SCITEX • 175 lpi • Kodak 80# Cougar

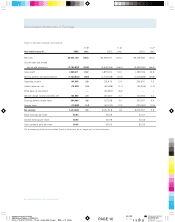

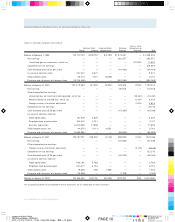

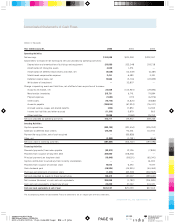

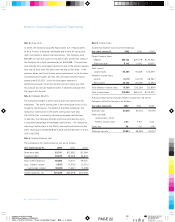

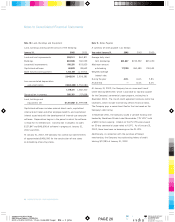

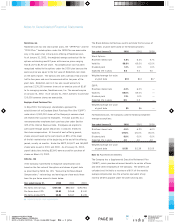

Notes to Consolidated Financial Statements

NORDSTROM INC. AND SUBSIDIARIES 21

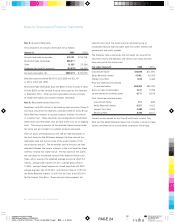

Deferred Lease Credits: The Company receives developer

reimbursements as incentives to construct stores in certain

developments. The Company capitalizes certain property, plant

and equipment for these stores during the construction period.

At the end of the construction period, developer reimbursements

in excess of construction costs are recorded as deferred lease

credits and amortized as a reduction to rent expense, on a straight-

line basis over the life of the applicable lease or operating covenant.

Construction costs in excess of developer reimbursements are

recorded as prepaid rent and amortized as rent expense on

a straight-line basis over the life of the applicable lease or

operating covenant.

Fair Value of Financial Instruments: The carrying amount of

cash equivalents and notes payable approximates fair value.

The fair value of long-term debt (including current maturities),

using quoted market prices of the same or similar issues with

the same remaining term to maturity, is approximately $1,378,000

and $1,041,000 at January 31, 2002 and 2001.

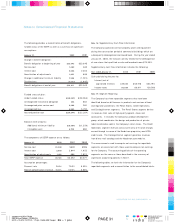

Derivatives Policy: The Company limits its use of derivative

financial instruments to the management of foreign currency

and interest rate risks. The effect of these activities is not material

to the Company’s financial condition or results of operations.

The Company has no material off-balance sheet credit risk,

and the fair value of derivative financial instruments at

January 31, 2002 and 2001 is not material.

Recent Accounting Pronouncements: In February 2001, the

Company adopted Statement of Financial Accounting Standards

(“SFAS”) No. 133, “Accounting for Derivative Instruments and

Hedging Activities,” as amended by SFAS No. 137 and No. 138.

It requires the fair value of all derivatives to be recognized as either

assets or liabilities and specifies accounting for changes in their

fair value. Adoption of this standard did not have a material

impact on the Company’s financial statements.

In March 2001, the Company adopted SFAS No. 140 “Accounting

for Transfers and Servicing of Financial Assets and Extinguishments

of Liabilities,” a replacement of SFAS No. 125 with the same title.

It revises the standards for securitizations and other transfers of

financial assets and collateral and requires certain additional

disclosures, but otherwise retains most of SFAS No. 125’s

provisions. Adoption of this standard did not have a material

impact on the Company’s financial statements.

The Emerging Issues Task Force (“EITF”) has reached a

consensus on Issue No. 99-20, “Recognition of Interest Income

and Impairment on Purchased and Retained Beneficial Interests

in Securitized Financial Assets,” which provides guidance on how

a transferor that retains an interest in securitized financial assets,

or an enterprise that purchases a beneficial interest in securitized

financial assets, should account for related interest income

and impairment. Adoption of this accounting issue in the quarter

ended July 31, 2001, did not have a material impact on the

Company’s financial statements.

In July 2001, the FASB issued SFAS No. 141 “Business

Combinations.” SFAS No. 141 requires that the purchase

method of accounting be used for all business combinations

initiated after June 30, 2001, and establishes specific criteria

for the recognition of goodwill separate from other intangible

assets. Adoption of the accounting provisions of SFAS No. 141

in February 2002 did not have a material impact on the

Company’s financial statements.

At February 1, 2002, the Company implemented SFAS No. 142

“Goodwill and Other Intangible Assets.” Under SFAS No. 142,

goodwill and intangible assets having indefinite lives will no longer

be amortized but will be subject to annual impairment tests.

Other intangible assets will continue to be amortized over their

estimated useful lives. Prior to the adoption of SFAS No. 142,

the Company’s intangible assets were amortized over their

estimated useful lives on a straight-line basis ranging from 10

to 35 years. Accumulated amortization of intangible assets was

$5,881 and $1,251 at January 31, 2002 and 2001. The Company

is currently evaluating the impact of SFAS No. 142 on its earnings

and financial position.

In February 2002, the Company adopted SFAS No. 144,

“Accounting for the Impairment or Disposal of Long-Lived Assets.”

SFAS No. 144 retains the fundamental provisions of SFAS No. 121,

but establishes new criteria for asset classification and broadens

the scope of qualifying discontinued operations. The adoption of

this statement did not have a material impact on the Company’s

financial statements.