Nissan 2006 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2006 Nissan annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

FINANCIAL SECTION

Nissan Annual Report 2005

70

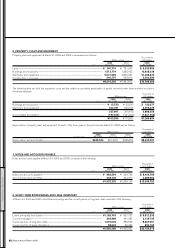

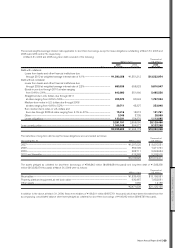

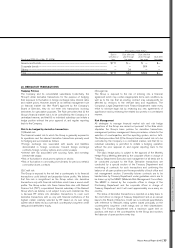

9. RETIREMENT BENEFIT PLANS

The Company and its domestic consolidated subsidiaries have defined benefit plans, i.e., welfare pension fund plans (“WPFP”), tax-qualified

pension plans and lump-sum payment plans, covering substantially all employees who are entitled to lump-sum or annuity payments, the amounts

of which are determined by reference to their basic rates of pay, length of service, and the conditions under which termination occurs. Effective

July 1, 2005, a portion of the benefit obligations under the above plans was transferred to newly established defined contribution plans. In this

connection, the pension plan assets of ¥45,762 million were also transferred to these defined contribution plans during the year ended March

31, 2006.

Certain foreign consolidated subsidiaries have defined benefit and/or defined contribution plans.

The following table sets forth the funded and accrued status of the plans, and the amounts recognized in the consolidated balance sheets as

of March 31, 2006 and 2005 for the Company’s and the consolidated subsidiaries’ defined benefit plans: Thousands of

Millions of yen U.S. dollars

2005 2004 2005

As of Mar. 31, 2006 Mar. 31, 2005 Mar. 31, 2006

Retirement benefit obligation....................................................................................................................................... ¥(1,239,004) ¥(1,217,260) $(10,589,778)

Plan assets at fair value.................................................................................................................................................... 817,371 500,815 6,986,077

Unfunded retirement benefit obligation............................................................................................................... (421,633) (716,445) (3,603,701)

Unrecognized net retirement benefit obligation at transition............................................................. 99,966 120,718 854,410

Unrecognized actuarial loss........................................................................................................................................... 120,920 154,689 1,033,505

Unrecognized prior service cost................................................................................................................................. (66,714) (66,720) (570,205)

Net retirement benefit obligation .............................................................................................................................. (267,461) (507,758) (2,285,991)

Prepaid pension cost........................................................................................................................................................... 234 445 2,000

Accrued retirement benefits.......................................................................................................................................... ¥ (267,695) ¥ (508,203) $ (2,287,991)

Certain domestic subsidiaries received the approval from the Minister of Health, Labour and Welfare in the years ended March 31, 2006, 2005,

and 2004 with respect to their application for an exemption from the obligation for benefits related to future employee services and for the return

of the past benefit obligation and related pension plan assets under the substitutional portion of the WPFP.

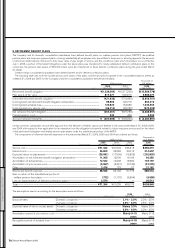

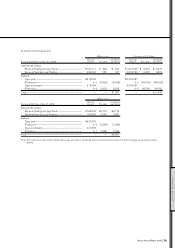

The components of retirement benefit expenses for the years ended March 31, 2006, 2005 and 2004 are outlined as follows:

Thousands of

Millions of yen U.S. dollars

2005 2004 2003 2005

For the years ended Mar. 31, 2006 Mar. 31, 2005 Mar. 31, 2004 Mar. 31, 2006

Service cost........................................................................................................................................................................... ¥41,022 ¥47,802 ¥48,418 $350,615

Interest cost .......................................................................................................................................................................... 36,809 33,288 33,012 314,607

Expected return on plan assets............................................................................................................................ (29,581) (17,999) (15,523) (252,829)

Amortization of net retirement benefit obligation at transition.................................................... 11,265 12,009 14,169 96,282

Amortization of actuarial loss.................................................................................................................................. 12,542 12,298 18,689 107,197

Amortization of prior service cost........................................................................................................................ (5,967) (5,431) (7,049) (51,000)

Other........................................................................................................................................................................................... 2,476 179 57 21,162

Retirement benefit expenses ................................................................................................................................. 68,566 82,146 91,773 586,034

Gain on return of the substitutional portion of

welfare pension fund plans................................................................................................................................... (772) (1,107) (5,594) (6,598)

Loss on implementation of defined contribution plans..................................................................... 3,570 —— 30,513

Total............................................................................................................................................................................................. ¥71,364 ¥81,039 ¥86,179 $609,949

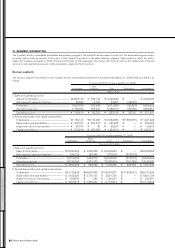

The assumptions used in accounting for the above plans were as follows:

2005 2004

For the years ended Mar. 31, 2006 Mar. 31, 2005

Discount rates Domestic companies....................................................................................................... 2.1% - 2.3% 2.3% - 2.5%

Overseas companies ....................................................................................................... 2.5% - 6.0% 2.5% - 9.5%

Expected rates of return on plan assets Domestic companies....................................................................................................... Mainly 3.0% Mainly 3.0%

Overseas companies ....................................................................................................... 3.0% - 9.0% 2.2% - 9.5%

Amortization period of prior service cost ............................................................................................................................................................... Mainly 9-15 Mainly 9-15

................................................................................................................................................................................................................................................................... years years

Recognition period of actuarial loss............................................................................................................................................................................ Mainly 9-18 Mainly 8-18

................................................................................................................................................................................................................................................................... years years