NetFlix 2011 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2011 NetFlix annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

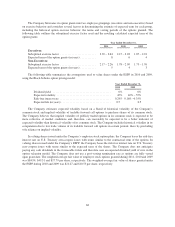

The 8.50% Notes include, among other terms and conditions, limitations on the Company’s ability to create,

incur, assume or be liable for indebtedness (other than specified types of permitted indebtedness); dispose of

assets outside the ordinary course (subject to specified exceptions); acquire, merge or consolidate with or into

another person or entity (other than specified types of permitted acquisitions); create, incur or allow any lien on

any of its property or assign any right to receive income (except for specified permitted liens); make investments

(other than specified types of investments); or pay dividends, make distributions, or purchase or redeem the

Company’s equity interests (each subject to specified exceptions). At December 31, 2011 and 2010, the

Company was in compliance with these covenants.

Based on quoted market prices, the fair value of the 8.50% Notes was approximately $206.5 million and

$225.0 million as of December 31, 2011 and 2010, respectively.

Credit Agreement

In September 2009, the Company entered into a credit agreement which provided for a $100 million three-

year revolving line of credit. Loans under the credit agreement bore interest, at the Company’s option, at either a

base rate determined in accordance with the credit agreement, plus a spread of 1.75% to 2.25%, or an adjusted

LIBOR rate plus a spread of 2.75% to 3.25%. In October 2009, the Company borrowed $20.0 million under the

credit agreement. The proceeds, net of issuance costs, to the Company were approximately $19.0 million. In

connection with the issuance of the 8.50% Notes, the Company repaid all outstanding amounts under and

terminated the credit agreement. Issuance costs related to the line of credit were included in interest expense in

the year ended December 31, 2009.

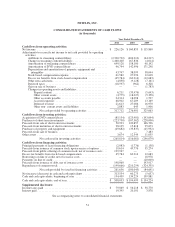

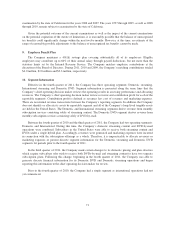

5. Commitments and Contingencies

Lease obligations

The Company leases facilities under non-cancelable operating leases with various expiration dates through

2018. The facilities generally require the Company to pay property taxes, insurance and maintenance costs.

Further, several lease agreements contain rent escalation clauses or rent holidays. For purposes of recognizing

minimum rental expenses on a straight-line basis over the terms of the leases, the Company uses the date of

initial possession to begin amortization, which is generally when the Company enters the space and begins to

make improvements in preparation of intended use. For scheduled rent escalation clauses during the lease terms

or for rental payments commencing at a date other than the date of initial occupancy, the Company records

minimum rental expenses on a straight-line basis over the terms of the leases in the Consolidated Statements of

Operations. The Company has the option to extend or renew most of its leases which may increase the future

minimum lease commitments.

Because the terms of the Company’s original facilities lease agreements required the Company’s

involvement in the construction funding of the buildings at its Los Gatos, California headquarters site, the

Company is the “deemed owner” (for accounting purposes only) of these buildings. Accordingly, the Company

recorded an asset of $40.7 million, representing the total costs of the buildings and improvements, including the

costs paid by the lessor (the legal owner of the buildings), with corresponding liabilities. Upon completion of

construction of each building, the Company did not meet the sale-leaseback criteria for de-recognition of the

building assets and liabilities. Therefore the leases are accounted for as financing obligations.

In the first quarter of 2010, the Company extended the facility leases for the Los Gatos buildings for an

additional five year term after the remaining term of the original lease, thus increasing the future minimum

payments under lease financing obligations by approximately $14 million. The leases continue to be accounted

for as financing obligations and no gain or loss was recorded as a result of the lease financing modification. At

December 31, 2011, the lease financing obligation balance was $34.1 million, of which $2.3 million and $31.8

million were recorded in “Accrued expenses” and “Other non-current liabilities,” respectively, on the

61