Macy's 2008 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2008 Macy's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

|

|

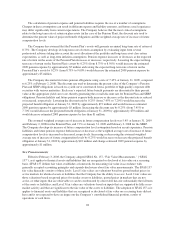

could materially increase or decrease the fair value of the reporting unit’s net assets and, accordingly, could

materially increase or decrease any related impairment charge. The first step of the impairment testing process

considers company-specific projections, the discount rate and the Company’s market capitalization around the

testing period. The second step of the impairment testing process considers third party estimates of the fair value

of certain assets and liabilities. The Company recorded an estimated goodwill impairment charge of $5,382

million during 2008. Increasing or decreasing the fair values of the net assets of each reporting unit by 5% as

compared to the values used in the preparation of these financial statements would increase or decrease the

impairment charge related to goodwill by approximately $153 million.

Self-Insurance Reserves

The Company, through its insurance subsidiaries, is self-insured for workers’ compensation and public

liability claims up to certain maximum liability amounts. Although the amounts accrued are actuarially

determined by third parties based on analysis of historical trends of losses, settlements, litigation costs and other

factors, the amounts the Company will ultimately disburse could differ from such accrued amounts.

Pension and Supplementary Retirement Plans

The Company has a funded defined benefit pension plan (the “Pension Plan”) and an unfunded defined

benefit supplementary retirement plan (the “SERP”). The Company accounts for these plans using SFAS No. 87,

“Employers’ Accounting for Pensions” (“SFAS 87”), as amended by SFAS No. 158, “Employers’ Accounting

for Defined Benefit Pension and Other Postretirement Plans – an amendment of FASB Statements No. 87, 88,

106, and 132(R)” (“SFAS 158”). Under SFAS 158, an employer recognizes the funded status of a defined benefit

postretirement plan as an asset or liability on the balance sheet and recognizes changes in that funded status in

the year in which the changes occur through comprehensive income. Under SFAS 87, pension expense is

recognized on an accrual basis over employees’ approximate service periods. Pension expense calculated under

SFAS 87 is generally independent of funding decisions or requirements.

Effective February 4, 2007, the Company adopted the measurement date provision of SFAS 158, which

requires the measurement of defined benefit plan assets and obligations to be the date of the Company’s fiscal

year-end balance sheet. This required a change in the Company’s measurement date, which was previously

December 31.

During 2006, Congress passed the Pension Protection Act of 2006 (the “Act”) with the stated purpose of

improving the funding of America’s private pension plans. The Act introduced new funding requirements for

defined benefit pension plans, introduces benefit limitations for certain under-funded plans and raises tax

deduction limits for contributions. The Act applies to pension plan years beginning after December 31, 2007.

Funding requirements for the Pension Plan are determined by government regulations, not SFAS 87 or SFAS

158. No funding contributions were required, and the Company made no funding contributions to the Pension

Plan in 2008 or 2007. As of the date of this report, the Company is anticipating making required funding

contributions to the Pension Plan totaling approximately $295 million to $370 million prior to January 30, 2010.

This includes the initiation of quarterly payments of approximately $30 million and a 2008 Plan year contribution

in September 2009 of approximately $175 million to $250 million. Management believes that, with respect to the

Company’s current operations, cash on hand and funds from operations, together with its credit facility and other

capital resources, will be sufficient to cover the Company’s Pension cash requirements in both the near term and

over the longer term.

At January 31, 2009, the Company had an unrecognized actuarial loss of $875 million for the Pension Plan

and an unrecognized actuarial gain of $19 million for the SERP. The unrecognized loss for the Pension Plan and

the unrecognized gain for the SERP will be recognized as a component of pension expense in future years in

accordance with SFAS No. 87, but are not expected to impact 2009 Pension and SERP expense.

27