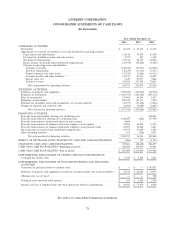

LinkedIn 2013 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2013 LinkedIn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

•Marketing Solutions—The Company earns revenue from the display of advertisements (both graphic

and text link) on its website primarily based on a cost per advertisement model. Revenue from

Internet advertising is generally recognized on a gross basis, with the exception of transactions with

advertising agencies, which are recognized net of agency discounts. The typical duration of the

Company’s advertising contracts is approximately two months.

•Premium Subscriptions—The Company sells various subscriptions to customers that allow users to

have further access to premium services via its LinkedIn.com website. The Company offers its

members monthly or annual subscriptions. Revenue from Premium Subscription services is

recognized ratably over the contractual period, generally from one to 12 months.

Amounts billed or collected in excess of revenue recognized are included as deferred revenue. Sales

tax is excluded from reported net revenue. Although historical refunds have been minimal, the Company

estimates allowances for each revenue type shown above based on information available as of each

balance sheet date. This information includes historical refunds as well as specific known service quality

issues. The Company records revenue for transactions in which it acts as an agent on a net basis, and

revenue for transactions in which it acts as a principal on a gross basis.

A majority of the Company’s arrangements for Talent Solutions and Marketing Solutions include

multiple deliverables. In accordance with authoritative guidance on revenue recognition, the Company

allocates consideration at the inception of an arrangement to all deliverables based on the relative selling

price method in accordance with the selling price hierarchy. The objective of the hierarchy is to determine

the price at which the Company would transact a sale if the service were sold on a stand-alone basis and

requires the use of: (i) vendor-specific objective evidence (‘‘VSOE’’) if available; (ii) third-party evidence

(‘‘TPE’’) if VSOE is not available; and (iii) best estimate of selling price (‘‘BESP’’) if neither VSOE nor

TPE is available.

VSOE. The Company determines VSOE based on its historical pricing and discounting practices for

the specific product or service when sold separately. In determining VSOE, the Company requires that a

substantial majority of the selling prices for these services fall within a reasonably narrow pricing range.

The Company has not historically priced its Marketing Solutions within a narrow range to establish

VSOE for such products. As a result, the Company has established VSOE for a limited number of Talent

Solutions products, and for such products, VSOE has been used to allocate the selling price to

deliverables.

TPE. When VSOE cannot be established for deliverables in multiple element arrangements, the

Company applies judgment with respect to whether it can establish a selling price based on TPE. TPE is

determined based on competitor prices for similar deliverables when sold separately. Generally, the

Company’s go-to-market strategy differs from that of its peers and its offerings contain a significant level

of differentiation such that the comparable pricing of services with similar functionality cannot be

obtained. Furthermore, the Company is unable to reliably determine what similar competitor services’

selling prices are on a stand-alone basis. As a result, the Company has not been able to establish selling

prices based on TPE.

BESP. When the Company is unable to establish selling prices using VSOE or TPE, the Company

uses BESP in its allocation of arrangement consideration. BESP is generally used to allocate the selling

price to deliverables in the Company’s multiple element arrangements. The Company determines BESP

for deliverables by considering multiple factors including, but not limited to, its pricing practices, prices it

charges for similar offerings, sales volume, geographies, market conditions, and the competitive landscape.

84