LinkedIn 2013 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2013 LinkedIn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

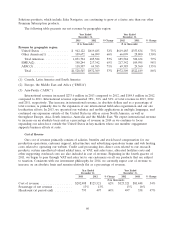

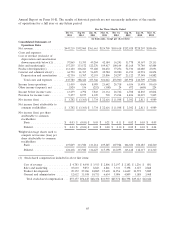

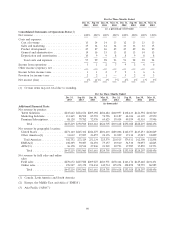

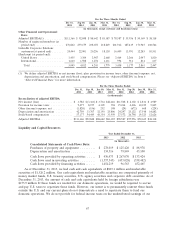

Item 7A. Quantitative and Qualitative Disclosure about Market Risk

We have operations both within the United States and internationally, and we are exposed to market

risks in the ordinary course of our business. These risks include primarily interest rate, foreign exchange

risks and inflation.

Interest Rate Fluctuation Risk

We had cash, cash equivalents, and marketable securities of $2,329.3 million and $749.5 million as of

December 31, 2013 and 2012, respectively. This amount was invested primarily in money market funds

and highly liquid investment grade fixed income securities. The cash, cash equivalents and marketable

securities are held for working capital purposes. Our investment policy and strategy is focused on the

preservation of capital and supporting our liquidity requirements. We do not enter into investments for

trading or speculative purposes. At December 31, 2013, the weighted-average duration of our investment

portfolio was less than one year.

Our fixed-income portfolio is subject to fluctuations in interest rates, which could affect our results of

operations. Based on our investment portfolio balance as of December 31, 2013, a hypothetical increase in

interest rates of 1% (100 basis points) would have resulted in a decrease in the fair value of our portfolio

of approximately $13.8 million, and a hypothetical increase of 0.5% (50 basis points) would have resulted

in a decrease in the fair value of our portfolio of approximately $6.9 million.

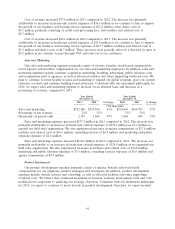

Foreign Currency Exchange Risks

We have foreign currency exchange risks related to our revenue and operating expenses denominated

in currencies other than the U.S. dollar, principally the British Pound Sterling, the Euro, the Australian

dollar, the Canadian dollar, the Indian rupee and the Singapore dollar. The volatility of exchange rates

depends on many factors that we cannot forecast with reliable accuracy. We have experienced and will

continue to experience fluctuations in our net income as a result of gains (losses) related to remeasuring

certain monetary assets and liabilities that are denominated in currencies other than the U.S. dollar. In

the event our foreign currency denominated assets, liabilities, sales or expenses increase, our operating

results may be more greatly affected by fluctuations in the exchange rates of the currencies in which we

do business.

We enter into foreign currency derivative contracts to hedge against assets and liabilities for which we

have foreign currency exposure to minimize the risk that our earnings will be adversely affected by

exchange rate fluctuations. Our foreign currency derivative contracts are not designated as hedging

instruments. These derivative instruments are carried at fair value with changes in the fair value recorded

to other income (expense), net in our consolidated statements of operations. These contracts do not

subject us to material balance sheet risk due to exchange rate movements because gains and losses on

these derivatives are intended to offset gains and losses on the hedged foreign currency denominated

assets and liabilities.

As of December 31, 2013, we had outstanding foreign currency derivative contracts with a total

notional amount of $94.8 million. If overall foreign currency exchange rates appreciated (depreciated)

uniformly by 5% against the U.S. dollar, our foreign currency derivative contracts outstanding as of

December 31, 2013 would experience a loss (gain) of approximately $4.6 million.

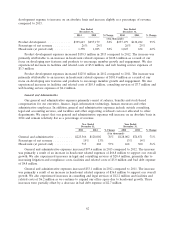

Inflation Risk

We do not believe that inflation has had a material effect on our business, financial condition or

results of operations. If our costs were to become subject to significant inflationary pressures, we may not

be able to fully offset such higher costs through price increases. Our inability or failure to do so could

harm our business, financial condition and results of operations.

70