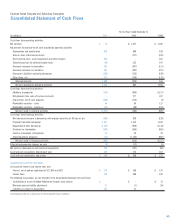

Kodak 2001 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2001 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

|

|

Company has never experienced non-performance by

any of its counterparties.

Cash Equivalents All highly liquid investments with a remaining

maturity of three months or less at date of purchase are considered to

be cash equivalents.

Marketable Securities and Noncurrent Investments The Company has

evaluated its investment policies consistent with SFAS No. 115,

“Accounting for Certain Investments in Debt and Equity Securities” which

requires that investment securities be classified as either held-to-

maturity, available-for-sale or trading. The Company’s debt and equity

investment securities are classified as held-to-maturity and available-

for-sale, respectively. Held-to-maturity investments are carried at

amortized cost and available-for-sale securities are carried at fair value,

with the unrealized gains and losses reported in Shareholders’ Equity

under the caption Accumulated Other Comprehensive Income (Loss).

At December 31, 2001, the Company had short-term investments

classified as held-to-maturity of $3 million. These investments were

included in other current assets. In addition, the Company had long-term

marketable securities and other investments classified as held-to-

maturity and available-for-sale equity securities of $1 million and $33

million, respectively, which were included in other long-term assets at

December 31, 2001.

At December 31, 2000, the Company had short-term investments

classified as held-to-maturity of $5 million, which were included in other

current assets. In addition, the Company had long-term marketable

securities and other investments classified as held-to-maturity and

available-for-sale equity securities of $5 million and $49 million,

respectively, which were included in other long-term assets at December

31, 2000.

Inventories Inventories are stated at the lower of cost or market. The cost

of most inventories in the U.S. is determined by the “last-in, first-out”

(LIFO) method. The cost of all of the Company’s remaining inventories in

and outside the U.S. is determined by the “first-in, first-out” (FIFO) or

average cost method, which approximates current cost. The Company

provides inventory reserves for excess, obsolete or slow-moving inventory

based on changes in customer demand, technology developments or

other economic factors.

Properties Properties are recorded at cost, net of accumulated

depreciation. The Company principally calculates depreciation expense

using the straight-line method over the assets’ estimated useful lives,

which are as follows:

Years

Buildings and building improvements 10–40

Machinery and equipment 3–20

Maintenance and repairs are charged to expense as incurred. Upon sale

or other disposition, the applicable amounts of asset cost and

accumulated depreciation are removed from the accounts and the net

amount, less proceeds from disposal, is charged or credited to income.

Goodwill Goodwill represents the excess of purchase price over the fair

value of the net assets acquired, and for the three-year period ended

December 31, 2001, goodwill was charged to earnings on a straight-line

basis over the period estimated to be benefited, generally ten years. See

Note 5.

Effective January 1, 2002, the Company will be accounting for

goodwill under SFAS No. 142, “Goodwill and Other Intangible Assets.”

Under SFAS No. 142 the Company will no longer amortize its goodwill

which, as of December 31, 2001, had a net balance of $948 million.

Under SFAS No. 142, the Company’s goodwill will be subject to an

impairment test, at least annually, and therefore, will only be charged to

operations to the extent it has been determined to be impaired. See the

Recently Issued Accounting Standards within Note 1.

Revenue The Company’s revenue transactions include sales of the

following: products; equipment; services; equipment bundled with

products and/or services; and integrated solutions. The Company

recognizes revenue when realized or realizable and earned, which is when

the following criteria are met: persuasive evidence of an arrangement

exists; delivery has occurred; the sales price is fixed and determinable;

and collectibility is reasonably assured. At the time revenue is

recognized, the Company provides for the estimated costs of warranties

and reduces revenue for estimated returns.

For product sales, the recognition criteria are generally met when

title and risk of loss have transferred from the Company to the buyer,

which may be upon shipment or upon delivery to the customer sites,

based on contract terms or legal requirements in foreign jurisdictions.

Service revenues are recognized as such services are rendered.

For equipment sales, the recognition criteria are generally met when

the equipment is delivered and installed at the customer site. In

instances in which the agreement with the customer contains a customer

acceptance clause, revenue is deferred until customer acceptance is

obtained, provided the customer acceptance clause is considered to be

substantive. For certain agreements, the Company does not consider

these customer acceptance clauses to be substantive because the

Company can and does replicate the customer acceptance test

environment and performs the agreed upon product testing prior to

shipment. In these instances, revenue is recognized upon installation of

the equipment.

55