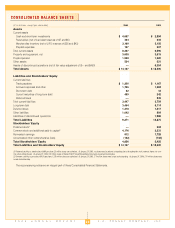

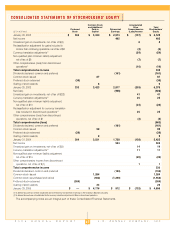

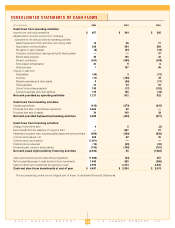

JCPenney 2004 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2004 JCPenney annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

J.C. PENNEY COMPANY, INC.2 004 ANNUAL REPORT

Notes to the Consolidated Financial Statements

29

NOTES TO THE CONSOLIDATED

FINANCIAL STATEMENTS

1SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Nature of Operations

JCPenney was founded by James Cash Penney in 1902 and has

grown to be a major retailer, operating 1,017 JCPenney

Department Stores throughout the United States and Puerto Rico

and 62 Renner Department Stores in Brazil. The Company sells

family apparel, jewelry, shoes, accessories and home furnishings

to customers through Department Stores, Catalog and the Internet.

In addition, the Department Stores provide services, such as salon,

optical, portrait photography and custom decorating, to customers.

Basis of Presentation

The consolidated financial statements present the results of J. C.

Penney Company, Inc. and its subsidiaries (the Company or

JCPenney). All significant intercompany transactions and bal-

ances have been eliminated in consolidation.

Certain debt securities were issued by J. C. Penney Corporation,

Inc. (JCP), the wholly owned operating subsidiary of the Company.

The Company is a co-obligor (or guarantor, as appropriate) regard-

ing the payment of principal and interest on JCP’s outstanding debt

securities. The guarantee by the Company of certain of JCP’s out-

standing debt securities is full and unconditional.

Use of Estimates

The preparation of financial statements, in conformity with gen-

erally accepted accounting principles (GAAP), requires manage-

ment to make estimates and assumptions that affect the reported

amounts of assets and liabilities and disclosure of contingent lia-

bilities at the date of the financial statements and the reported

amounts of revenues and expenses during the reporting period.

While actual results could differ from these estimates, manage-

ment does not expect the differences, if any, to have a material

effect on the financial statements.

The most significant estimates relate to inventory valuation

under the retail method, specifically permanent reductions to

retail prices (markdowns) and adjustments for shortages (shrink-

age); valuation of long-lived assets; valuation allowances and

reserves, specifically those related to closed stores, workers’

compensation and general liability, environmental contingencies,

income taxes and litigation; reserves related to the Eckerd dis-

continued operations; and pension accounting. Closed store

reserves are established for the estimated present value of oper-

ating lease obligations (PVOL) and other exit costs. Workers’

compensation and general liability reserves are based on actuar-

ially determined estimates of claims that have been reported, as

well as those incurred but not yet reported resulting from histori-

cal experience and current data. Environmental remediation

reserves are estimated using a range of potential liability, based

on the Company’s experience and consultation with independent

engineering firms and in-house legal counsel, as appropriate.

Income taxes are estimated for each jurisdiction in which the

Company operates. Deferred tax assets are evaluated for recov-

erability, and a valuation allowance is recorded if it is deemed

more likely than not that the asset will not be realized. Litigation

reserves are based on management’s best estimate of potential

liability, with consultation of in-house and outside counsel.

Related to pension accounting, the selection of assumptions,

including the estimated rate of return on plan assets and the dis-

count rate, impact the actuarially determined amounts reflected

in the Company’s consolidated financial statements.

Fiscal Year

The Company’s fiscal year has historically ended on the last

Saturday in January. Effective as of January 29, 2005, the

Company changed its fiscal year end to the Saturday closest to

January 31, to be in alignment with the fiscal calendar used by

the majority of national retail companies. This change had no

impact on fiscal 2004 reported results, nor will it have any impact

on fiscal 2005 financial statements. Fiscal 2006 will contain 53

weeks, instead of in 2008, when it would have occurred under the

Company’s historical reporting calendar. Unless otherwise stat-

ed, references to years in this report relate to fiscal years rather

than to calendar years.

Fiscal Year Ended Weeks

2004 January 29, 2005 52

2003 January 31, 2004 53

2002 January 25, 2003 52

The accounts of Renner are on a calendar-year basis.

Reclassifications

Certain reclassifications have been made to prior year amounts

to conform to the current year presentation. None of the reclassifi-

cations impacted the Company’s net income/(loss) in any period.

Merchandise and Services Revenue Recognition

Revenue, net of estimated returns, is recorded at the point of

sale when payment is made and customers take possession of

the merchandise in department stores, at the point of shipment of

merchandise ordered through Catalog/Internet or, in the case of

services, the customer has received the benefit of the service,

such as salon, portrait, optical or custom decorating.

Commissions earned on sales generated by licensed depart-

ments are included as a component of retail sales. Shipping and

handling fees charged to customers are also recorded as retail

sales with related costs recorded as cost of goods sold. The

Company provides for estimated future returns based on histori-

cal return rates and sales levels.

Advertising

Advertising costs, which include newspaper, television, radio

and other media advertising, are expensed either as incurred or

the first time the advertising occurs. Total advertising costs, net of

cooperative advertising agreements, were $1,234 million, $1,178

million and $1,081 million for 2004, 2003 and 2002, respectively.

These totals include catalog book costs of $268 million, $264 mil-

lion and $260 million for 2004, 2003 and 2002, respectively.

Catalog book preparation and printing costs, which are considered