HSBC 2003 Annual Report Download - page 367

Download and view the complete annual report

Please find page 367 of the 2003 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

357 -

358

358 -

359

359 -

360

360 -

361

361 -

362

362 -

363

363 -

364

364 -

365

365 -

366

366 -

367

367 -

368

368 -

369

369 -

370

370 -

371

371 -

372

372 -

373

373 -

374

374 -

375

375 -

376

376 -

377

377 -

378

-

379

-

380

-

381

-

382

-

383

-

384

|

|

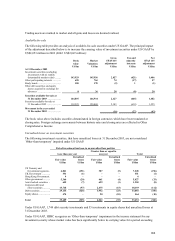

365

At 31 December 2003, the sensitivity of the current fair value of the interest-only strip receivables to an

immediate 10 per cent and 20 per cent unfavourable change in assumptions are presented in the table below.

These sensitivities are based on assumptions used to value interest-only strip receivables at 31 December 2003.

Real Estate

Secured Auto Finance

MasterCard/

Visa

Private

Label

Personal

Non-Credit

Card

Carrying value (fair value) of interest- only

strip receivables (US$ millions)................ 5157301146345

Weighted-average life (in years) ................... 0.7 1.9 0.6 0.7 1.6

Payment speed assumption (annual rate)....... 21.7% 38.1% 80.5% 76.2% 44.2%

Impact on fair value of 10% adverse

change (US$ millions) .......................... – (31) (26) (12) (26)

Impact on fair value of 20% adverse

change (US$ millions) .......................... – (59) (48) (22) (51)

Expected credit losses (annual rate) .............. 1.8% 7.4% 5.4% 5.8% 10.1%

Impact on fair value of 10% adverse

change (US$ millions) .......................... – (52) (28) (18) (66)

Impact on fair value of 20% adverse

change (US$ millions) .......................... (1) (104) (56) (36) (131)

Discount rate on residual cash flows (annual

rate)........................................................... 13.0% 10.0% 9.0% 10.0% 11.0%

Impact on fair value of 10% adverse

change (US$ millions) .......................... – (10) (3) (1) (4)

Impact on fair value of 20% adverse

change (US$ millions) .......................... – (19) (6) (1) (8)

Variable returns to investors (annual rate)..... 1.3% – 1.8% 2.7% 2.2%

Impact on fair value of 10% adverse

change (US$ millions) .......................... – – (10) (9) (14)

Impact on fair value of 20% adverse

change (US$ millions) .......................... – – (19) (17) (28)

These sensitivities are hypothetical and should not be considered to be predictive of future performance. As the

figures indicate, the change in fair value based on a 10 per cent variation in assumptions cannot necessarily be

extrapolated because the relationship of the change in assumption to the change in fair value may not be linear.

Also, in this table, the effect of a variation in a particular assumption on the fair value of the residual cash flow

is calculated independently from any change in another assumption. In reality, changes in one factor may

contribute to changes in another (for example, increases in market interest rates may result in lower

prepayments) which might magnify or counteract the sensitivities. Furthermore, the estimated fair values as

disclosed should not be considered indicative of future earnings on these assets.

Static pool credit losses are calculated by summing actual and projected future credit losses and dividing them

by the original balance of each pool of asset. Due to the short term revolving nature of MasterCard and Visa,

and private label loan balances, the weighted-average percentage of static pool credit losses is not considered to

be materially different from the weighted-average charge-off assumptions used in determining the fair value of

interest-only strip receivables in the table above. At 31 December 2003, static pool credit losses for auto finance

loans securitised in 2003 were estimated to be 11.5 per cent.