HSBC 2003 Annual Report Download - page 326

Download and view the complete annual report

Please find page 326 of the 2003 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

316 -

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

|

|

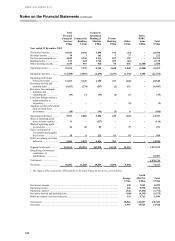

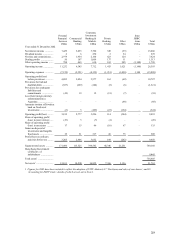

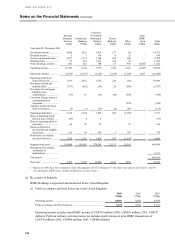

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

324

Pension funds

At 31 December 2003, US$14.7 billion (2002: US$9.8 billion) of HSBC pension fund assets were under

management by HSBC companies of which US$1,315 million (2002: US$1,155 million) of ‘Long-term

assurance assets attributable to policyholders’ were included in HSBC’ s balance sheet under ‘Other assets’ . Fees

of US$23 million (2002: US$23 million) were earned by HSBC companies for these management services.

HSBC’ s pension funds had placed deposits of US$211 million (2002: US$252 million) with its banking

subsidiaries.

49 UK and Hong Kong accounting requirements

The financial statements have been prepared in accordance with UK accounting requirements. There would be no

material differences had they been prepared in accordance with Hong Kong Accounting Standards, except as set out

below.

The presentation of the cash flow statement is in accordance with Financial Reporting Standard 1 (revised 1996)

‘Cash Flow Statements’ rather than Hong Kong Statement of Standard Accounting Practice 15 ‘Cash Flow

Statements’ .

In accordance with Financial Reporting Standard 11 ‘Impairment of Fixed Assets and Goodwill’ , no charge has been

made in the profit and loss account in respect of those decreases in the valuation of HSBC properties that do not

represent impairments. If HSBC had prepared its financial statements under Hong Kong Statement of Standard

Accounting Practice 17 ‘Property, plant and equipment’ , there would have been a net charge to the profit and loss

account of US$154 million (2002: US$94 million) in respect of valuations below depreciated historical cost (of

which a credit of US$4 million (2002: US$2 million) relates to minority interests).

In accordance with Financial Reporting Standard 19 ‘Deferred Tax’ , HSBC has recognised deferred tax in full on

timing differences between the accounting and taxation treatment of income and expenditure, subject to

recoverability of deferred tax assets. If HSBC had prepared its financial statements in accordance with Hong Kong

Statement of Standard Accounting Practice 12 ‘Income Taxes’ (revised August 2002) it would have recognised

additional deferred tax assets and liabilities, resulting in an increase in reserves at 31 December 2003 of US$174

million (2002: US$119 million). The impact on the charge to the profit and loss account in respect of tax on profit on

ordinary activities would have been nil (2002: increase of US$22 million).

If HSBC had prepared its financial statements under Hong Kong Statement of Standard Accounting Practice 24

‘Investments in Securities’ , US$1,746 million (2002: US$1,341 million1) would have been credited to reserves in

respect of changes in the fair value of its investment securities.

In accordance with UK Statement of Standard Accounting Practice 17 ‘Post balance sheet events’ , HSBC has

recorded dividends declared after the period end in the period to which they relate. If HSBC had prepared its

financial statements in accordance with Hong Kong Statement of Standard Accounting Practice 9 ‘Events after the

balance sheet date’ , dividends would be recorded in the period in which they are declared and there would have been

an increase in reserves at 31 December 2003 of US$2,627 million (2002: US$3,069 million).

HSBC Holdings has recorded its investment in HSBC undertakings at net asset value, including attributable

goodwill, adjusted for shares held by subsidiaries in HSBC Holdings plc. If HSBC Holdings had prepared its

individual financial statements in accordance with Hong Kong Statement of Standard Accounting Practice 32

‘Consolidated Financial Statements and Accounting for Investments in Subsidiaries’ and elected to record its

investment in HSBC undertakings at cost, less provisions for any impairment, there would have been a reduction in

the reserves of HSBC Holdings at 31 December 2003 of US$33,970 million (2002: US$13,779 million1). There

would have been no impact on the consolidated financial statements of HSBC.

HSBC applies UK Statement of Standard Accounting Practice 24 ‘Accounting for pension costs’ to defined benefit

schemes, which requires that the cost of providing pensions be recognised on a systematic and rational basis over the

period during which benefit is gained from the employees’ services. If HSBC had prepared its financial statements

under Hong Kong Statement of Standard Accounting Practice 34 ‘Employee benefits’ a defined benefit pension

liability of US$4,406 million would have been recognised in the balance sheet at 31 December 2003 (2002: