HSBC 2003 Annual Report Download - page 332

Download and view the complete annual report

Please find page 332 of the 2003 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

341 -

342

342 -

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

|

|

HSBC HOLDINGS PLC

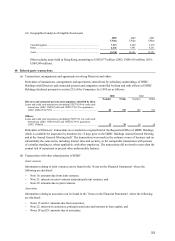

Notes on the Financial Statements (continued)

330

– For a derivative designated as hedging exposure to variable cash flows of a recognised asset or liability, or

of a forecast transaction, the derivative’ s gain or loss associated with the effective portion of the hedge is

initially reported as a component of other comprehensive income and subsequently reclassified into

earnings when the forecast transaction affects earnings. The ineffective portion is reported in earnings

immediately.

– For net investment hedges in which derivatives hedge the foreign currency exposure of a net investment in

a foreign operation, the change in fair value of the derivative associated with the effective portion of the

hedge is included as a component of other comprehensive income, together with the associated loss or gain

on the hedged item. The ineffective portion is reported in earnings immediately.

– In order to apply hedge accounting it is necessary to comply with documentation requirements and to

demonstrate the effectiveness of the hedge on an ongoing basis.

– For a derivative not designated as a hedging instrument, the gain or loss is recognised in earnings in the

period of change in fair value.

Investment securities

UK GAAP

• Debt securities and equity shares intended to be held on a continuing basis are disclosed as investment securities

and are included in the balance sheet at cost less provision for any permanent diminution in value. Other

participating interests are accounted for on the same basis. Premiums or discounts on dated investment securities

purchased at other than face value are amortised through the profit and loss account over the period from date of

purchase to date of maturity and are included in ‘interest income’ . Any profit or loss on realisation of these

securities is recognised in the profit and loss account as it arises and included in ‘Gains on disposal of

investment securities’ .

• SSAP 20 ‘Foreign currency translation’ requires foreign currency exchange differences on foreign currency-

denominated monetary items, including securities, to be recognised in the profit and loss account.

• Other debt securities and equity shares held for trading purposes are included in the balance sheet at market

value. Changes in the market value of such assets are recognised in the profit and loss account as ‘Dealing

profits’ .

US GAAP

• All debt securities and equity shares are classified and disclosed within one of the following three categories:

held-to-maturity; available-for-sale; or trading (SFAS 115 ‘Accounting for Certain Investments in Debt and

Equity Securities’ ).

• Held-to-maturity debt securities are measured at amortised cost.

• Available-for-sale securities are measured at fair value with unrealised holding gains and losses excluded from

earnings and reported net of applicable taxes and minority interests in a separate component of shareholders’

funds. Foreign exchange gains or losses on foreign currency denominated available-for-sale securities are also

excluded from earnings and recorded as part of the same separate component of shareholders’ funds.

• A decline considered other than temporary in fair value below cost of an available-for-sale or held-to-maturity

security is treated as a realised loss and included in earnings. This lower fair value is then treated as the cost

basis for the security.

• Trading securities are measured at fair value with unrealised holding gains and losses included in earnings.