HSBC 2003 Annual Report Download - page 335

Download and view the complete annual report

Please find page 335 of the 2003 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

341 -

342

342 -

343

343 -

344

344 -

345

345 -

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

|

|

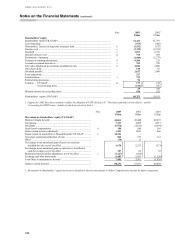

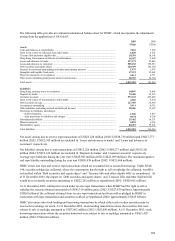

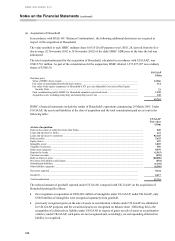

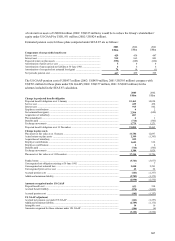

333

Securitisations

UK GAAP

• FRS 5 ‘Reporting the substance of transactions’ requires that the accounting for securitised receivables is

governed by whether the originator has access to the benefits of the securitised assets and exposure to the risks

inherent in those benefits and whether the originator has a liability to repay the proceeds of the note issue:

– The securitised assets should be derecognised in their entirety and a gain or loss on sale recorded where the

originator retains no significant benefits and no significant risks relating to those securitised assets.

– The securitised assets and the related finance should be consolidated under a linked presentation where the

originator retains significant benefits and significant risks relating to those securitised assets but where the

downside exposure is limited to a fixed monetary amount and certain other conditions are met.

– The securitised assets and the related finance should be consolidated on a gross basis where the originator

retains significant benefits and significant risks relating to those securitised assets and does not meet the

conditions required for linked presentation.

US GAAP

• SFAS 140 ‘Accounting for Transfers and Servicing of Finance Assets and Extinguishments of Liabilities’

requires that receivables that are sold to a special purpose entity and securitised can only be derecognised and a

gain or loss on sale recognised if the originator has surrendered control over those securitised assets.

• Control has been surrendered over transferred assets if and only if all of the following conditions are met:

– The transferred assets have been put presumptively beyond the reach of the transferor and its creditors, even

in bankruptcy or other receivership.

– Each holder of interests in the transferee (i.e. holder of issued notes) has the right to pledge or exchange

their beneficial interests, and no condition constrains this right and provides more than a trivial benefit to

the transferor.

– The transferor does not maintain effective control over the assets through either an agreement that obligates

the transferor to repurchase or to redeem them before their maturity or through the ability to unilaterally

cause the holder to return specific assets, other than through a clean-up call.

– If these conditions are not met the securitised assets should continue to be consolidated.

• Where HSBC retains an interest in the securitised assets, such as a servicing right or the right to residual cash

flows from the special purpose entity, HSBC recognises this interest at fair value on sale of the assets.

• There are no provisions for linked presentation of securitised assets and the related finance.

Consolidation of Variable Interest Entities

UK GAAP

• In accordance with FRS 5, entities that fall within the definition of quasi-subsidiaries are consolidated. A quasi-

subsidiary is defined as an entity that is directly or indirectly controlled by HSBC and gives rise to benefits that

are in substance no different from those that would arise were the vehicle a subsidiary. FRS 5 states that this

will arise where HSBC receives the benefits of the net assets of the entity and is exposed to the risks inherent in

those net assets.

US GAAP

• FASB Interpretation 46 ‘Consolidation of Variable Interest Entities’ (‘FIN 46’) requires consolidation of

Variable Interest Entities (‘VIEs’ ) in which HSBC is the primary beneficiary and disclosures in respect of all

other VIEs in which it has a significant variable interest.