HSBC 2003 Annual Report Download - page 342

Download and view the complete annual report

Please find page 342 of the 2003 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

341 -

342

342 -

343

343 -

344

344 -

345

345 -

346

346 -

347

347 -

348

348 -

349

349 -

350

350 -

351

351 -

352

352 -

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

|

|

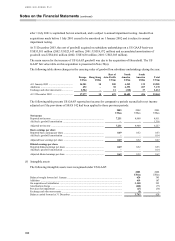

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

340

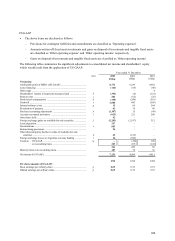

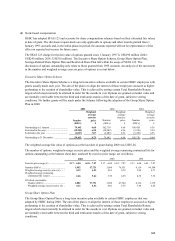

No goodwill on the acquisition of Household was deductible for tax purposes.

UK GAAP US GAAP

US$m US$m

Amount of goodwill by reportable geographic customer group

North America

–Commercial banking ........................................................................................................... 59 56

–Consumer finance ...............................................................................................................9,382 6,077

Europe

–Consumer finance ...............................................................................................................567 484

Total amount of goodwill ........................................................................................................ 10,008 6,617

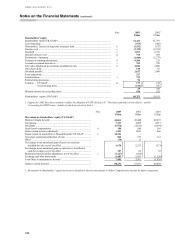

(b) Shareholders’ interest in long-term assurance fund

Under UK GAAP, the value of the shareholders’ interest in the in-force life assurance and fund pensions

policies of the long-term assurance fund are valued at the net present value of the profits inherent in such

policies. The net present value of such profits is not recognised under US GAAP.

US GAAP requires the application of different accounting treatments in a number of areas of accounting for the

long-term assurance fund. In particular, the definition and amortisation of deferred acquisition costs and the

methodology for determining actuarial reserves vary between US and UK GAAP.

Net pre-tax income under US GAAP would have been US$394 million lower than under UK GAAP, as a result

of differences in accounting for the shareholder’ s interest in the log term assurance fund. The reduction in

income is greater than in previous years, because of an increase in the net present value of in force policies in

the UK, due in part to a reduction in the risk discount rate, new business in Hong Kong (profits on new business

are recognised sooner under UK GAAP) and certain refinements to the models underlying the US GAAP

calculation.

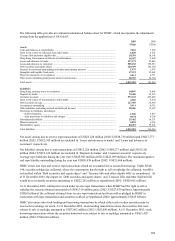

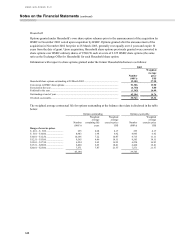

(c) Pension and post-retirement costs

Pensions

For the purpose of the above reconciliations, the provisions of SFAS 87 ‘Employers’ Accounting for Pensions’

have been applied to HSBC’s main pension plans, which make up approximately 95 per cent of all HSBC’ s

schemes by plan assets. For non-US schemes, HSBC has applied SFAS 87 ‘Employers’ Accounting for

Pensions’ with effect from 30 June 1992 as it was not feasible to apply it as at 1 January 1989, the date specified

in the standard.

The projected benefit obligation in excess of plan assets at 30 June 1992 for the HSBC Bank (UK) Pension

Scheme has been recognised as a liability under the purchase accounting requirements of APB 16 ‘Business

Combinations’ . For other pension plans, the excess of the projected benefit obligation over plan assets at 30

June 1992 is recognised as a charge to pension expense over 15 years.

The projected benefit obligation in excess of plan assets at 28 July 2000 for CCF was recognised as a liability

under the purchase accounting adjustments of APB 16 ‘Business combinations’ .

When the accumulated benefit obligation on a pension plan (the value of the benefits accrued based on

employee service up to the balance sheet date) exceeds the fair value of plan assets, the employer recognises an

additional minimum pension liability equal to this excess, so long as the excess is greater than any accrual

which has already been established for unfunded pension costs. At the same time, an intangible asset is

established equal to the lower of the liability recognised for the unfunded benefit obligation or the amount of

any unrecognised prior service cost.

At 31 December 2003, HSBC recognised an additional minimum pension liability of US$2,789 million (2002:

US$1,175 million) in respect of its unfunded accumulated benefit obligations. This liability is partially offset by

an intangible asset of US$14 million. (2002: US$16 million). The net impact of these items, after taking account