HSBC 2003 Annual Report Download - page 336

Download and view the complete annual report

Please find page 336 of the 2003 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

341 -

342

342 -

343

343 -

344

344 -

345

345 -

346

346 -

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

|

|

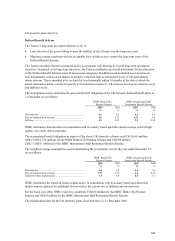

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

334

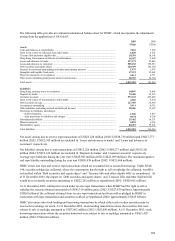

• A modified version of FIN 46 (‘FIN 46R’ ) addresses certain implementation issues that arose under FIN 46 and

changes some of the criteria used to determine whether HSBC is the primary beneficiary of an entity. HSBC has

applied FIN 46R to its assessment of certain entities where the impact of the modifications in FIN 46R is

known. HSBC is still assessing the impact of FIN 46R on other entities, and will adopt FIN 46R in 2004 for all

interests in VIEs for accounting periods ending after 15 March 2004.

• A VIE is an entity in which equity investors do not hold an investment with the characteristics of a controlling

financial interest or do not have sufficient equity at risk for the entity to finance its activities. HSBC is the

primary beneficiary of a VIE if its variable interests absorb a majority of the entity’ s expected losses. Variable

interests are contractual, ownership or other pecuniary interests in an entity that change with changes in the fair

value of an entity’ s net assets exclusive of variable interests. If no party absorbs a majority of the entity’ s

expected losses, HSBC consolidates the VIE if it receives a majority of the expected residual returns of the

entity.

• Under the transitional provisions of FIN 46R, HSBC is only required to consolidate VIEs where it is the primary

beneficiary if HSBC’ s involvement in the VIE was created or acquired after 31 January 2003 and it had

previously applied FIN 46 to those entities. For VIEs created or acquired before this date, disclosure that HSBC

is the primary beneficiary is sufficient. HSBC will be required to consolidate all VIEs where it is the primary

beneficiary from 1 January 2004.

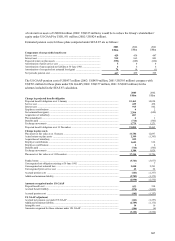

Restructuring provisions

UK GAAP

• In accordance with FRS 12 ‘Provisions, contingent liabilities and contingent assets’ , provisions are made for

any direct costs and net future operating losses arising from a business that management is committed to

restructure, sell or terminate, has a detailed formal plan to exit, and has raised a valid expectation of carrying out

that plan.

US GAAP

• SFAS 146 ‘Accounting for Costs Associated with Exit or Disposal Activities’ , requires that the fair value of a

liability for a cost associated with an exit or disposal activity be recognised when the liability is incurred.

Accordingly, provisions are recognised upon the implementation of the restructuring plan.

Acceptances

UK GAAP

• Acceptances outstanding are not included in the consolidated balance sheet.

US GAAP

• Acceptances outstanding and matching customer liabilities are included in the consolidated balance sheet.

Profit and loss presentation

UK GAAP

• The following items are separately disclosed in the profit and loss account:

– Provisions for contingent liabilities and commitments.

– Amounts written off fixed asset investments.

– Gains on disposal of investments and tangible fixed assets.