HSBC 2003 Annual Report Download - page 354

Download and view the complete annual report

Please find page 354 of the 2003 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

344 -

345

345 -

346

346 -

347

347 -

348

348 -

349

349 -

350

350 -

351

351 -

352

352 -

353

353 -

354

354 -

355

355 -

356

356 -

357

357 -

358

358 -

359

359 -

360

360 -

361

361 -

362

362 -

363

363 -

364

364 -

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

|

|

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

352

• non-recognition of residual interests in securitisation vehicles existing at acquisition under UK GAAP.

Instead, the assets and liabilities of the securitisation vehicles are recognised on the UK GAAP balance

sheet, and credit provisions are established against the loans and advances. This GAAP adjustment existing

at acquisition unwinds over the life of the securitisation vehicles; and

• certain costs which under UK GAAP, relate to either post-acquisition management decisions or certain

decisions made prior to the acquisition are required to be expensed to the post acquisition profit and loss

account and cannot be capitalised as goodwill, or included within the fair value of the liabilities of the

acquired entity.

(i) Accruals accounted derivatives

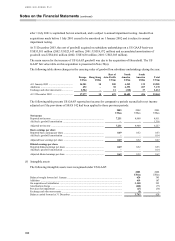

Under UK GAAP, internal derivatives used to hedge banking book transactions may be accruals accounted but,

under US GAAP, all derivatives are held at fair value. With the exception of certain subsidiaries in North

America, HSBC has not elected to satisfy the more prescriptive hedge documentation requirements of SFAS

133 in respect of external derivative contracts. Internal derivative contracts are not recognised for hedge

accounting purposes under US GAAP.

Fair value hedges

At 1 January 2001 contracts which had previously qualified as fair value hedges under US GAAP were marked

to market with a corresponding revaluation of the hedged item. There was no material ineffectiveness of these

hedges and therefore no adjustment was required to US GAAP reported income.

HSBC’ s North American operating subsidiaries designate certain derivative financial instruments as qualifying

SFAS 133 fair value hedges of certain fixed rate assets and liabilities. Where the critical terms of the hedge

instrument are identical at the hedge inception date, the short-cut method of accounting is utilised for these

hedging relationships. As a result, no retrospective or prospective assessment of effectiveness is required and no

hedge ineffectiveness is recognised.

For a small number of fair value hedges of fixed rate liabilities, the short-cut method of accounting cannot be

utilised. Ineffectiveness of such fair value hedges recognised in US GAAP reported net income was a loss of

US$0.4 million (2002: nil; 2001: nil).

Additionally, since 2002, HSBC’ s US mortgage bank has hedged fixed rate closed residential mortgage loans

held for sale with forward sale commitments. In order to satisfy the retrospective and prospective assessment of

effectiveness for SFAS 133, the cumulative dollar offset method is utilised. Ineffectiveness is recognised in the

income statement on a monthly basis. Ineffectiveness on these hedging activities recognised in US GAAP

reported net income was a gain of US$0.2 million (2002: gain of US$7.6 million; 2001: nil).

Cash flow hedges

There were no significant contracts at 1 January 2001 which had previously qualified as cash flow hedges under

US GAAP.

HSBC’ s North American operating subsidiaries designate certain derivative financial instruments, including

interest rate swaps and future contracts, as qualifying FAS 133 cash flow hedges of the forecast repricing of

certain deposit liabilities, issues of debt and variable rate commercial loans. In order to initially qualify,

assessment of hedge effectiveness is demonstrated on a prospective basis utilising both statistical regression

analysis and the cumulative dollar offset method. In order to satisfy the retrospective assessment of

effectiveness for FAS 133, the cumulative dollar offset method is utilised and ineffectiveness is recognised in

the income statement on a monthly basis. The time value component of the derivative contracts is excluded from

the assessment of hedge effectiveness.

Ineffectiveness of cash flow hedging activities recognised in US GAAP reported net income was a gain of

US$3.6 million (2002: gain of US$12.7 million; 2001: gain of US$8.5 million). The adjustment to US GAAP