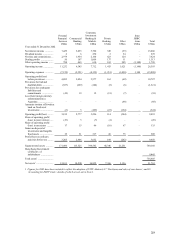

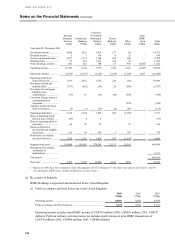

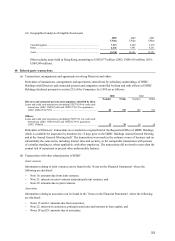

HSBC 2003 Annual Report Download - page 333

Download and view the complete annual report

Please find page 333 of the 2003 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

341 -

342

342 -

343

343 -

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

|

|

331

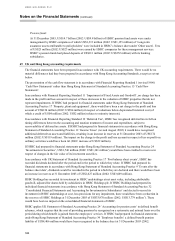

Foreign currency

UK GAAP

• A company’ s local currency is the currency of the primary economic environment in which it operates and

generates net cash flows. Foreign exchange differences arising when translating non-local currency assets and

liabilities into the local currency are reported in the profit and loss account (SSAP 20 ‘Foreign currency

translation’ ).

US GAAP

• An entity’ s functional currency is the currency of the primary economic environment in which it operates. An

entity operating in a single economic environment may have only one functional currency. Foreign exchange

differences arising when translating non-functional currency assets and liabilities into the local currency are

reported in the profit and loss account (SFAS 52 ‘Foreign Currency Translation’ ).

Own shares held

UK GAAP

• The adoption of UITF Abstracts 37 and 38 has required a change in the presentation of shares in HSBC Holdings

held by HSBC. HSBC Holdings shares are now deducted from shareholders’ funds (including those HSBC

Holdings shares held within ‘Long term assurance assets attributable to policyholders’ ). No profits or losses are

recognised on own shares held. Previously, own shares held were classified as an asset. The change in

accounting policy has been reflected by way of a prior period adjustment.

US GAAP

• AICPA Accounting Research Bulletin 43 ‘Restatement and Revision of Accounting Research Bulletins’

requires a reduction in shareholders’ equity for own shares held. HSBC shares held within ‘Long-term assurance

assets attributable to policyholders’ remain classified as an asset where the criteria for classification as ‘separate

accounts’ are met.

Dividends payable

UK GAAP

• Dividends declared after the period end are recorded in the period to which they relate.

US GAAP

• Dividends are recorded in the period in which they are declared.

Deferred taxation

UK GAAP

• Deferred tax is generally provided in the accounts for all timing differences subject to exceptions in FRS 19 and

the assessment of the recoverability of deferred tax assets.

• Fair value adjustments on acquisition are treated as if they were timing differences arising in the acquired

entity’ s own accounts. Deferred tax is recognised on fair value adjustments where they give rise to deferral or

acceleration of taxable cash flows.

US GAAP

• Deferred tax liabilities and assets are recognised in respect of all temporary differences. A valuation allowance

is raised against any deferred tax asset where it is more likely than not that the asset, or a part thereof, will not

be realised (SFAS 109 ‘Accounting for Income Taxes’ ).