GE 2008 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2008 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

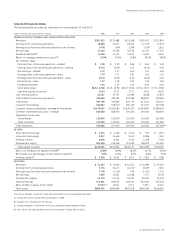

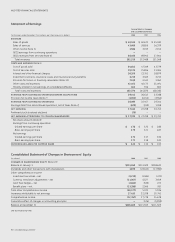

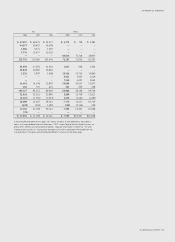

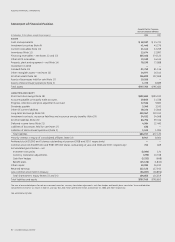

management’s discussion and analsis

ge 2008 annual report 45

received routinely from independent appraisers. Estimated cash

flows from future leases are reduced for expected downtime

between leases and for estimated technical costs required to

prepare aircraft to be redeployed. Fair value used to measure

impairment is based on current market values from independent

appraisers.

We recognized impairment losses on our operating lease

portfolio of commercial aircraft of $0.1 billion in both 2008 and

2007. Provisions for losses on financing receivables related to

commercial aircraft were insignificant in 2008 and 2007.

Further information on impairment losses and our exposure

to the commercial aviation industry is provided in the Operations—

Overview section and in Notes 14 and 31.

Real Estate. We review our real estate investment portfolio for

impairment routinely or when events or circumstances indicate

that the related carrying amounts may not be recoverable. The

cash flow estimates used for both estimating value and the recov-

erability analysis are inherently judgmental, and reflect current

and projected lease profiles, available industry information about

expected trends in rental, occupancy and capitalization rates and

expected business plans, which include our estimated holding

period for the asset. Our portfolio is diversified, both geographi-

cally and by asset type. However, the global real estate market is

subject to periodic cycles that can cause significant fluctuations

in market values. At December 31, 2008, the carrying value of our

Capital Finance Real Estate investments exceeded the estimated

value by about $4 billion. At December 31, 2007, the estimated

value exceeded the carrying value by about $3 billion. This decline

in the estimated value of the portfolio reflected sales of properties

with a book value of $5.8 billion, resulting in pre-tax gains of

$1.9 billion, and also reflected deterioration in current and

expected real estate market liquidity and macroeconomic trends

throughout the year, resulting in declining market occupancy

rates and market rents as well as increases in our estimates of

market capitalization rates based on historical data. Declines in

estimated value of real estate below carrying value result in

impairment losses when the aggregate undiscounted cash flow

estimates used in the estimated value measurement are below

carrying amount. As such, estimated losses in the portfolio will

not necessarily result in recognized impairment losses. When we

recognize an impairment, the impairment is measured based

upon the fair value of the underlying asset which is based upon

current market data, including current capitalization rates.

During 2008, Capital Finance Real Estate recognized pre-tax

impairments of $0.3 billion in its real estate held for investment,

as compared to $0.2 billion in 2007. Continued deterioration in

economic conditions or prolonged market illiquidity may result in

further impairments being recognized. Furthermore, significant

judgment and uncertainty related to forecasted valuation trends,

especially in illiquid markets, results in inherent imprecision in

real estate value estimates. Further information is provided in

the Global Risk Management section and in Note 16.

an adjustment of earnings; such adjustments decreased earnings

by $0.2 billion in 2008 and increased earnings by $0.4 billion and

$0.8 billion in 2007 and 2006, respectively. We provide for probable

losses when they become evident.

Carrying amounts for product services agreements in progress

at both December 31, 2008 and 2007, were $5.5 billion, and are

included in the line, “Contract costs and estimated earnings” in

Note 16.

Further information is provided in Note 1.

ASSET IMPAIRMENT assessment involves various estimates and

assumptions as follows:

Investments. We regularly review investment securities for

impairment using both quantitative and qualitative criteria.

Quantitative criteria include the length of time and magnitude of

the amount that each security is in an unrealized loss position

and, for securities with fixed maturities, whether the issuer is in

compliance with terms and covenants of the security. Qualitative

criteria include the financial health of and specific prospects for

the issuer, as well as our intent and ability to hold the security

to maturity or until forecasted recovery. Our other-than-temporary

impairment reviews involve our finance, risk and asset manage-

ment functions as well as the portfolio management and research

capabilities of our internal and third-party asset managers.

See Note 28, which discusses the determination of fair value of

investment securities.

Further information about actual and potential impairment

losses is provided in the Financial Resources and Liquidity —

Investment Securities section and in Notes 1, 9 and 16.

Long-Lived Assets. We review long-lived assets for impairment

whenever events or changes in circumstances indicate that the

related carrying amounts may not be recoverable. Determining

whether an impairment has occurred typically requires various

estimates and assumptions, including determining which

undiscounted cash flows are directly related to the potentially

impaired asset, the useful life over which cash flows will occur,

their amount, and the asset’s residual value, if any. In turn,

measurement of an impairment loss requires a determination of

fair value, which is based on the best information available.

We derive the required undiscounted cash flow estimates from

our historical experience and our internal business plans. To

determine fair value, we use our internal cash flow estimates

discounted at an appropriate interest rate, quoted market prices

when available and independent appraisals, as appropriate.

Commercial aircraft are a significant concentration of assets in

Capital Finance, and are particularly subject to market fluctuations.

Therefore, we test recoverability of each aircraft in our operating

lease portfolio at least annually. Additionally, we perform quarterly

evaluations in circumstances such as when aircraft are re-leased,

current lease terms have changed or a specific lessee’s credit

standing changes. We consider market conditions, such as global

demand for commercial aircraft. Estimates of future rentals and

residual values are based on historical experience and information