GE 2008 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2008 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

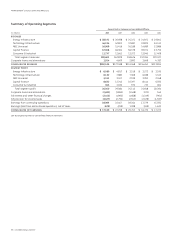

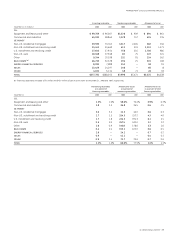

management’s discussion and analsis

34 ge 2008 annual report

FINANCING RECEIVABLES is our largest category of assets and

represents one of our primary sources of revenues. A discussion

of the quality of certain elements of the financing receivables

portfolio follows. For purposes of that discussion, “delinquent”

receivables are those that are 30 days or more past due; and

“nonearning” receivables are those that are 90 days or more past

due (or for which collection has otherwise become doubtful).

Our portfolio of financing receivables is diverse and not

directly comparable to major U.S. banks. Historically, we have

had less consumer exposure, which over time has had higher

loss rates than commercial exposure. Our consumer exposure is

largely non-U.S. and primarily comprises mortgage, sales finance,

auto and personal loans in various European and Asian countries.

Our U.S. consumer financing receivables comprise 7% of our

total portfolio. Of those, approximately 42% relate primarily to

credit cards, which are often subject to profit and loss sharing

arrangements with the retailer (the results of which are reflected

in GECS revenues), and have a smaller average balance and lower

loss severity as compared to bank cards. The remaining 58% are

sales finance receivables, which provide electronics, recreation,

medical and home improvement financing to customers. In 2007,

we exited the U.S. mortgage business and we have no U.S. auto

or student loans.

Our commercial portfolio primarily comprises senior, secured

positions with comparatively low loss history. The secured

receivables in this portfolio are collateralized by a variety of asset

classes, including industrial-related facilities and equipment;

commercial and residential real estate; vehicles, aircraft, and

equipment used in many industries, including the construction,

manufacturing, transportation, telecommunications and health-

care industries. In addition, 2% of this portfolio is unsecured

corporate debt.

Losses on financing receivables are recognized when they

are incurred, which requires us to make our best estimate of

probable losses inherent in the portfolio. Such estimate requires

consideration of historical loss experience, adjusted for current

conditions, and judgments about the probable effects of relevant

observable data, including present economic conditions such

as delinquency rates, financial health of specific customers and

market sectors, collateral values, and the present and expected

future levels of interest rates. Our risk management process

includes standards and policies for reviewing major risk expo-

sures and concentrations, and evaluates relevant data either for

individual loans or financing leases, or on a portfolio basis, as

appropriate.

in an unrealized loss position at December 31, 2008, we intend

to hold them at least until such time as their individual fair values

exceed their amortized cost and we have the ability to hold all

such debt securities until their maturities. The fair values used to

determine these unrealized gains and losses are those defined

by relevant accounting standards and are not a forecast of

future gains or losses. For additional information, see Note 9.

FAIR VALUE MEASUREMENTS. Effective January 1, 2008, we

adopted Financial Accounting Standards Board (FASB) Statement

of Financial Accounting Standards (SFAS) 157, Fair Value

Measurements, for all financial instruments and non-financial

instruments accounted for at fair value on a recurring basis.

Adoption of SFAS 157 did not have a material effect on our

financial position or results of operations. During the fourth

quarter, our methodology remained consistent with prior quarters

for measuring fair value of financial instruments trading in

volatile markets. Additional information about our application of

SFAS 157 is provided in Note 28.

WORKING CAPITAL, representing GE current receivables and

inventories, less GE accounts payable and progress collections,

was $3.9 billion at December 31, 2008, down $2.5 billion from

December 31, 2007, reflecting higher progress collections at

Energy. As Energy delivers units out of its backlog over the next

few years, progress collections of $13.1 billion at December 31,

2008, will be earned, affecting working capital adversely.

Nonetheless, our performance is expected to improve in 2009 as

a result of our Operating Council’s initiatives (e.g., lean projects

on cycle time), which will significantly offset the decrease in

progress collections.

We discuss current receivables and inventories, two important

elements of working capital, in the following paragraphs.

CURRENT RECEIVABLES for GE amounted to $15.1 billion at both

the end of 2008 and 2007, and included $11.3 billion due from

customers at the end of 2008 compared with $11.0 billion at the

end of 2007. GE current receivables turnover was 7.5 in 2008,

compared with 7.3 in 2007. See Note 10.

INVENTORIES for GE amounted to $13.6 billion at December 31,

2008, up $0.8 billion from the end of 2007. This increase reflected

higher inventories from purchases at Energy Infrastructure. GE

inventory turnover was 8.0 and 8.3 in 2008 and 2007, respectively.

See Note 11.