Frontier Communications 2007 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2007 Frontier Communications annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

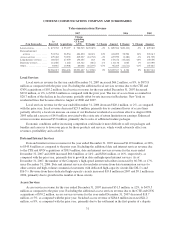

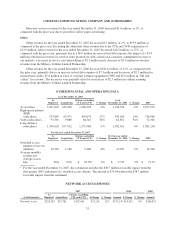

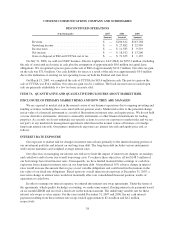

CITIZENS COMMUNICATIONS COMPANY AND SUBSIDIARIES

DISCONTINUED OPERATIONS

($ in thousands) 2007 2006 2005

Amount Amount Amount

Revenue ...................................... $ — $100,612 $163,768

Operating income ..............................$—$27,882 $ 22,969

Income taxes ..................................$—$11,583 $ 9,519

Net income ...................................$—$18,912 $ 13,266

Gain on disposal of ELI and CCUSA, net of tax ......$—$71,635 $ 1,167

On July 31, 2006, we sold our CLEC business, Electric Lightwave, LLC (ELI) for $255.3 million (including

the sale of associated real estate) in cash plus the assumption of approximately $4.0 million in capital lease

obligations. We recognized a pre-tax gain on the sale of ELI of approximately $116.7 million. Our after-tax gain

on the sale was $71.6 million. Our cash liability for taxes as a result of the sale was approximately $5.0 million

due to the utilization of existing tax net operating losses on both the Federal and state level.

On March 15, 2005, we completed the sale of CCUSA for $43.6 million in cash. The pre-tax gain on the

sale of CCUSA was $14.1 million. Our after-tax gain was $1.2 million. The book income taxes recorded upon

sale are primarily attributable to a low tax basis in assets sold.

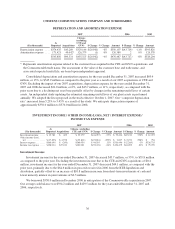

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

DISCLOSURE OF PRIMARY MARKET RISKS AND HOW THEY ARE MANAGED

We are exposed to market risk in the normal course of our business operations due to ongoing investing and

funding activities, including those associated with our pension assets. Market risk refers to the potential change

in fair value of a financial instrument as a result of fluctuations in interest rates and equity prices. We do not hold

or issue derivative instruments, derivative commodity instruments or other financial instruments for trading

purposes. As a result, we do not undertake any specific actions to cover our exposure to market risks and we are

not party to any market risk management agreements other than in the normal course of business or to hedge

long-term interest rate risk. Our primary market risk exposures are interest rate risk and equity price risk as

follows:

INTEREST RATE EXPOSURE

Our exposure to market risk for changes in interest rates relates primarily to the interest-bearing portion of

our investment portfolio and interest on our long-term debt. The long-term debt includes various instruments

with various maturities and weighted average interest rates.

Our objectives in managing our interest rate risk are to limit the impact of interest rate changes on earnings

and cash flows and to lower our overall borrowing costs. To achieve these objectives, all but $148.5 million of

our borrowings have fixed interest rates. Consequently, we have limited material future earnings or cash flow

exposures from changes in interest rates on our long-term debt. A hypothetical 10% adverse change in interest

rates would increase the amount that we pay on our variable obligations and could result in fluctuations in the

fair value of our fixed rate obligations. Based upon our overall interest rate exposure at December 31, 2007, a

near-term change in interest rates would not materially affect our consolidated financial position, results of

operations or cash flows.

In order to manage our interest expense, we entered into interest rate swap agreements. Under the terms of

the agreements, which qualify for hedge accounting, we made semi-annual, floating interest rate payments based

on six month LIBOR and received a fixed rate on the notional amount. The underlying variable rate for these

interest rate swaps is set in arrears. For the years ended December 31, 2007 and 2006, the net cash interest

payment resulting from these interest rate swaps totaled approximately $2.4 million and $4.2 million,

respectively.

38