EasyJet 2010 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2010 EasyJet annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

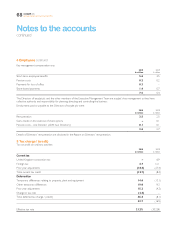

Overview Business review Governance Accounts Other information

easyJet plc

Annual report and accounts 2010

63

Financial instruments

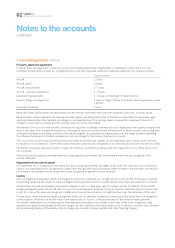

Financial instruments are recognised when easyJet becomes a party to the contractual provisions of the relevant instrument and

derecognised when it ceases to be a party to such provisions.

Where market values are not available, the fair value of financial instruments is calculated by discounting cash flows at prevailing interest

rates and by applying year end exchange rates.

Non-derivative financial assets

Non-derivative financial assets are recorded at amortised cost and include loan notes, trade receivables, cash and money market deposits.

Investments in equity instruments are carried at cost where fair value cannot be reliably measured due to significant variability in the range

of reasonable fair value estimates.

Restricted cash comprises cash deposits which have restrictions governing their use and is classified as a current or non-current asset based

on the estimated remaining length of the restriction. Cash and cash equivalents comprise cash held in bank accounts with no access

restrictions and bank or money market deposits repayable on demand or maturing within three months of inception. Interest income

on cash and money market deposits is recognised using the effective interest method.

Impairment losses are recognised on financial assets carried at amortised cost where there is objective evidence that an impairment loss

has been incurred. The amount of the loss is measured as the difference between the asset’s carrying amount and the present value of

future cash flows, discounted at the original effective interest rate.

If, subsequently, the amount of the impairment loss decreases, and the decrease can be related objectively to an event that occurred after

the impairment was recognised, the appropriate portion of the loss is reversed. Both impairment losses and reversals are recognised in the

income statement as components of net finance charges.

Non-derivative financial liabilities

Non-derivative financial liabilities are initially recorded at fair value less directly attributable transaction costs, and subsequently at amortised

cost. Interest expense on loans is recognised using the effective interest method.

Borrowings are classified as current liabilities unless there is an unconditional right to defer settlement of the liability for at least 12 months

after the balance sheet date.

Derivative financial instruments

Derivative financial instruments are measured at fair value.

Derivative financial instruments designated as cash flow hedges are used to mitigate operating and investing transaction exposures to

movements in jet fuel prices and currency exchange rates. Hedge accounting is applied to these instruments.

Changes in intrinsic fair value are recognised in other comprehensive income to the extent that the cash flow hedges are determined

to be effective. All other changes in fair value are recognised immediately in the income statement. Where the hedged item results in a

non-financial asset or liability the accumulated gains and losses previously recognised in other comprehensive income form part of the

initial carrying amount of the asset or liability. Otherwise accumulated gains and losses are recognised in the income statement in the

same period in which the hedged items affect the income statement.

Hedge accounting is discontinued when a hedging instrument is derecognised (e.g. through expiry or disposal), or no longer qualifies

for hedge accounting. Where the hedged item is a highly probable forecast transaction, the related gains and losses remain in other

comprehensive income until the transaction takes place.

When a hedged future transaction is no longer expected to occur, any related gains and losses previously recognised in other

comprehensive income are immediately recognised in the income statement.

Financial guarantees

If a claim on a financial guarantee given to a third party becomes probable, the obligation is recognised at fair value. For subsequent

measurement, the carrying amount is the higher of initial measurement and best estimate of the expenditure required to settle the

obligation on the statement of financial position date.