CarMax 2008 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2008 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

|

|

59

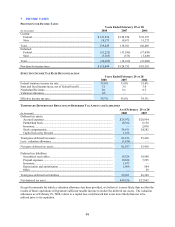

(D) Advertising Expense

Selling, general and administrative expenses included advertising expense of $108.8 million in fiscal 2008, $97.8

million in fiscal 2007 and $86.7 million in fiscal 2006. Advertising expenses were 1.3% of net sales and operating

revenues for fiscal 2008, 2007 and 2006.

15. CONTINGENT LIABILITIES

(A) Litigation

On June 12, 2007, Ms. Regina Hankins filed a putative class action lawsuit against CarMax, Inc., in Baltimore

County Circuit Court, Maryland. We operate five stores in the state of Maryland. The plaintiff alleges that, since

May 25, 2004, CarMax has not properly disclosed its vehicles’ prior rental history, if any. The plaintiff seeks

compensatory damages, punitive damages, injunctive relief and the recovery of attorneys’ fees. At this time, we

continue to evaluate the allegations and our defenses. We are unable to make a reasonable estimate of the amount or

range of loss that could result from an unfavorable outcome in this matter.

We are involved in various other legal proceedings in the normal course of business. Based upon our evaluation of

information currently available, we believe that the ultimate resolution of any such proceedings will not have a

material adverse effect, either individually or in the aggregate, on our financial condition or results of operations.

(B) Other Matters

In accordance with the terms of real estate lease agreements, we generally agree to indemnify the lessor from certain

liabilities arising as a result of the use of the leased premises, including environmental liabilities and repairs to

leased property upon termination of the lease. Additionally, in accordance with the terms of agreements entered into

for the sale of properties, we generally agree to indemnify the buyer from certain liabilities and costs arising

subsequent to the date of the sale, including environmental liabilities and liabilities resulting from the breach of

representations or warranties made in accordance with the agreements. We do not have any known material

environmental commitments, contingencies or other indemnification issues arising from these arrangements.

As part of our customer service strategy, we guarantee the used vehicles we retail with a 30-day limited warranty. A

vehicle in need of repair within 30 days of the customer's purchase will be repaired free of charge. As a result, each

vehicle sold has an implied liability associated with it. Accordingly, we record a provision for estimated repairs

during the guarantee period for each vehicle sold based on historical trends. The liability for this guarantee was $3.2

million as of February 29, 2008, and $2.4 million as of February 28, 2007, and is included in accrued expenses and

other current liabilities.

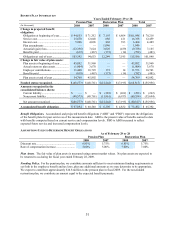

16. RECENT ACCOUNTING PRONOUNCEMENTS

In September 2006, the FASB issued SFAS No. 157, “Fair Value Measurements” (“SFAS 157”), which defines fair

value, establishes a framework for measuring fair value in U.S. generally accepted accounting principles and

expands disclosures about fair value measurements. The statement does not require new fair value measurements,

but is applied to the extent that other accounting pronouncements require or permit fair value measurements.

Companies will be required to disclose the extent to which fair value is used to measure assets and liabilities, the

inputs used to develop the measurements and the effect of certain of the measurements on earnings (or changes in

net assets) for the period. In February 2008, the FASB issued FASB Staff Position (FSP) Financial Accounting

Standard (FAS) 157-1 that removes leasing from the scope of SFAS 157, and FSP FAS 157-2 that delays the

effective date of SFAS 157 for all nonfinancial assets and nonfinancial liabilities, except those that are recognized or

disclosed at fair value in the financial statements on a recurring basis (at least annually), until our fiscal year

beginning March 1, 2009. CarMax was required to adopt SFAS 157 as amended as of March 1, 2008. As of the date

of adoption, the fair value of the majority of our financial assets within the scope of SFAS 157 was determined using

significant unobservable inputs. The adoption of SFAS 157 has not had a material impact on our results of

operations, financial condition or cash flows.

In February 2007, the FASB issued SFAS No. 159, “The Fair Value Option for Financial Assets and Financial

Liabilities – including an amendment of FASB Statement No. 115” (“SFAS 159”), which permits all entities to

choose to measure many financial instruments and certain other items at fair value and consequently report

unrealized gains and losses on these items in earnings. SFAS 159 was effective for our fiscal year beginning March

1, 2008. We have not elected to adopt SFAS 159.

In December 2007, the FASB issued Statement SFAS No. 141(R), “Business Combinations” (“SFAS 141(R)”).

SFAS 141(R) replaces SFAS No. 141, “Business Combinations” (“SFAS 141”), but retains the requirement that the

purchase method of accounting for acquisitions be used for all business combinations. SFAS 141(R) expands on the