CVS 2010 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2010 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

|

|

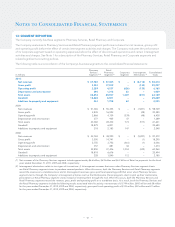

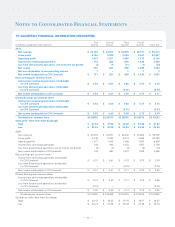

9: PENSION PLANS AND OTHER POSTRETIREMENT BENEFITS

DEFINED CONTRIBUTION PLANS

The Company sponsors voluntary 401(k) savings plans that cover substantially all employees who meet plan eligibility require-

ments. The Company makes matching contributions consistent with the provisions of the plans.

At the participant’s option, account balances, including the Company’s matching contribution, can be moved without restriction

among various investment options, including the Company’s common stock. The Company also maintains a nonqualified,

unfunded Deferred Compensation Plan for certain key employees. This plan provides participants the opportunity to defer

portions of their eligible compensation and receive matching contributions equivalent to what they could have received under

the CVS Caremark 401(k) and Employee Stock Ownership Plan absent certain restrictions and limitations under the Internal

Revenue Code. The Company’s contributions under the previously defined contribution plans totaled $186 million, $173 million

and $117 million in 2010, 2009 and 2008, respectively.

OTHER POSTRETIREMENT BENEFITS

The Company provides postretirement health care and life insurance benefits to certain retirees who meet eligibility require-

ments. The Company’s funding policy is generally to pay covered expenses as they are incurred. For retiree medical plan

accounting, the Company reviews external data and its own historical trends for health care costs to determine the health

care cost trend rates. As of December 31, 2010 and 2009, the Company’s postretirement medical plans have an accumulated

postretirement benefit obligation of $17 million. Net periodic benefit costs related to these postretirement medical plans were

approximately $1 million for 2010, 2009 and 2008, respectively.

PENSION PLANS

The Company sponsors nine defined benefit pension plans that cover certain full-time employees. Three of the plans are

tax-qualified plans that are funded based on actuarial calculations and applicable federal laws and regulations. The other six

plans are unfunded nonqualified supplemental retirement plans. All of the plans were frozen in prior periods, except one of

the nonqualified plans.

As of December 31, 2010, the Company’s pension plans had a projected benefit obligation of $659 million and plan assets of

$426 million. As of December 31, 2009, the Company’s pension plans had a projected benefit obligation of $612 million and plan

assets of $372 million. Net periodic pension costs related to these pension plans were $36 million, $16 million and $9 million in

2010, 2009 and 2008, respectively. The net periodic pension costs for 2010 includes settlements of $12 million.

The discount rate is determined by examining the current yields observed on the measurement date of fixed-interest, high

quality investments expected to be available during the period to maturity of the related benefits on a plan by plan basis. The

discount rate for the plans was 5.5% in 2010 and 6.0% in 2009. The expected long-term rate of return on plan assets is deter-

mined by using the plan’s target allocation and historical returns for each asset class on a plan by plan basis. The expected

long-term rate of return for all plans was 7.25% in 2010 and 8.5% in 2009 and 2008.

Historically, the Company used an investment strategy, which emphasized equities in order to produce higher expected returns,

and in the long run, lower expected expense and cash contribution requirements. The qualified pension plan asset allocation

targets were 60% equity and 40% fixed income. As the result of a detailed asset liability study performed during 2009, the

Company revised the pension plan target asset allocation to 50% equity and 50% fixed income with the transition to the new

targets to begin during 2010.

As of December 31, 2010, the Company’s qualified defined benefit pension plan assets consisted of 57% equity, 42% fixed

income, and 1% money market securities of which 71% were classified as Level 1 and 29% as Level 2 in the fair value hierarchy.

The Company’s qualified defined benefit pension plan assets as of December 31, 2009 consisted of 64% equity, 35% fixed

income, and 1% money market securities of which 67% were classified as Level 1 and 33% as Level 2 in the fair value hierarchy.

The Company contributed $65 million, $50 million and $8 million to the pension plans during 2010, 2009 and 2008, respectively.

The Company plans to make approximately $90 million in contributions to the pension plans during 2011.

Pursuant to various labor agreements, the Company is also required to make contributions to certain union-administered

pension and health and welfare plans that totaled $58 million, $57 million and $49 million in 2010, 2009 and 2008, respectively.

– 63 –