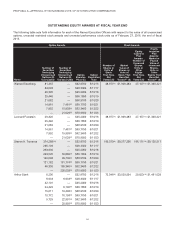

Bed, Bath and Beyond 2015 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2015 Bed, Bath and Beyond annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

PROPOSAL 4—SHAREHOLDER PROPOSAL REGARDING PROXY ACCESS BYLAWS

We have been notified that the following shareholder proposal will be presented for consideration at the Annual Meeting.

Promptly upon receipt of an oral or written request we will provide you with the name and address of, and number of shares

held by, each proponent.

RESOLVED: Shareholders of Bed Bath & Beyond Inc. (the “Company”) ask the board of directors (“the Board”) to take the

steps necessary to adopt a “proxy access” bylaw. Such a bylaw shall require the Company to include in proxy materials

prepared for a shareholder meeting at which directors are to be elected the name, Disclosure and Statement (as defined

herein) of any person nominated for election to the board by a shareholder or group (the “Nominator”) that meets the criteria

established below. The Company shall allow shareholders to vote on such nominee on the Company’s proxy card.

The number of shareholder-nominated candidates appearing in proxy materials shall not exceed one quarter of the directors

then serving. This bylaw, which shall supplement existing rights under Company bylaws, should provide that a Nominator

must:

(a) have beneficially owned 3% or more of the Company’s outstanding common stock continuously for at least three

years before submitting the nomination;

(b) give the Company, within the time period identified in its bylaws, written notice of the information required by the

bylaws and any Securities and Exchange Commission rules about (i) the nominee, including consent to being named

in the proxy materials and to serving as director if elected; and (ii) the Nominator, including proof it owns the required

shares (the “Disclosure”); and

(c) certify that (i) it will assume liability stemming from any legal or regulatory violation arising out of the Nominator’s

communications with the Company shareholders, including the Disclosure and Statement; (ii) it will comply with all

applicable laws and regulations if it uses soliciting material other than the Company’s proxy materials; and (iii) to the

best of its knowledge, the required shares were acquired in the ordinary course of business and not to change or

influence control at the Company.

The Nominator may submit with the Disclosure a statement not exceeding 500 words in support of each nominee (the

“Statement”). The Board shall adopt procedures for promptly resolving disputes over whether notice of a nomination was

timely, whether the Disclosure and Statement satisfy the bylaw and applicable federal regulations, and the priority to be given

to multiple nominations exceeding the one-quarter limit.

SUPPORTING STATEMENT

We believe proxy access is a fundamental shareholder right that will make directors more accountable and enhance

shareholder value. A 2014 CFA Institute study concluded that proxy access would “benefit both the markets and corporate

boardrooms, with little cost or disruption” and could raise overall US market capitalization by up to $140.3 billion if adopted

market-wide. (http://www.cfapubs.org/doi/pdf/10.2469/ccb.v2014.n9.1)

The proposed terms are similar to those in vacated SEC Rule 14a-11 (https://www.sec.gov/rules/final/2010/33-9136.pdf). The

SEC, following extensive analysis and input from companies and investors, determined that those terms struck the proper

balance of providing shareholders with a viable proxy access right while containing appropriate safeguards.

The proposed terms enjoy strong support. Through October 2015, votes on more than 100 similar proposals averaged 55%

and at least 60 companies enacted bylaws with similar terms.

We urge shareholders to vote FOR this proposal.

The Board of Directors Recommends a Vote Against Proposal 4

The Board of Directors recognizes that proxy access is an important development in corporate governance. Our directors, and

particularly our Nominating and Corporate Governance Committee, have discussed and will continue to discuss proxy access

developments with shareholders as part of the Company’s shareholder engagement program.

Based on discussions with our shareholders, we know that not all shareholders support proxy access. Among those who do

support proxy access, there are differing views of the features that are appropriate for a proxy access bylaw. Additionally,

based on our review of proxy access bylaws that have been adopted by other companies, there is an array of approaches on

structure and fundamental terms. For example, there is not a market consensus on the percentage of shareholder-nominated

candidates that can appear in the Company’s proxy materials, which we believe is a fundamental term. The proposal requires

44