Avon 2005 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2005 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

|

|

2005ANNUALREPORT57

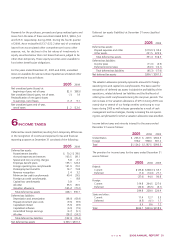

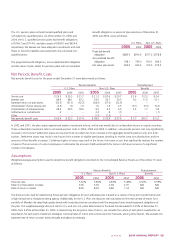

10

EMPLOYEEBENEFITPLANS

Savings Plan

We offer a qualified defined contribution plan for U.S.-based

employees, the Avon Personal Savings Account Plan, which allows

eligible participants to contribute up to 25% of eligible compen-

sation through payroll deductions. Prior to February 2005, we

matched employee contributions dollar for dollar up to the first 3%

of eligible compensation and fifty cents for each dollar contributed

from 4% to 6% of eligible compensation. In February 2005, Avon

temporarily suspended the matching contribution which has been

resumed in 2006. In 2005, 2004 and 2003, matching contributions

approximating $1.8, $14.6 and $14.5, respectively, were made

to this plan in cash, which was then used by the plan to purchase

Avon shares in the open market.

Retirement Plans

Avon and certain subsidiaries have contributory and noncon-

tributory retirement plans for substantially all employees of those

subsidiaries. Benefits under these plans are generally based on

an employee’s years of service and average compensation near

retirement. Plans are funded based on legal requirements and

cash flow.

Effective July 1998, the defined benefit retirement plan covering

U.S.-based employees was converted to a cash balance plan with

benefits determined by pay-based credits related to age and service

and interest credits based on individual account balances and pre-

vailing interest rates. A ten-year transitional period was established

for all employees covered under the pre-existing defined benefit

retirement plan. For the period from July 1, 1998, through June 30,

2008, benefits are calculated under both the former final average

pay formula and the cash balance formula. Employees who were

hired before July 1, 1998 are eligible to receive whichever benefit

(final average pay or cash balance) yields the higher amount. For

employees who were hired before July 1, 1998, however, the ben-

efit calculated under the former final average pay formula is frozen

at June 30, 2008. The cash balance formula continues to accrue

benefits on and after July 1, 2008.

Any pension plan participant who has retired on or after May 1,

2002, but before March 31, 2005 who chose to receive 20% or

more of his or her benefit as an annuity at retirement was eligible

to receive a social security supplement payable until the age of 65.

Postretirement Benefits

We provide health care and life insurance benefits for the majority

of employees who retire under our retirement plans in the United

States and certain foreign countries. The cost of such health care

benefits is shared by us and our retirees for employees hired on or

before January 1, 2005. Employees hired after January 1, 2005,

pay the full cost of the health care benefits.

In August 2005, we announced

that our Board of Directors

authorized us to repurchase

an additional $500.0 of our

common stock. The $500.0

program was completed

during December 2005.