Avon 2005 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2005 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

|

|

NOTESTOCONSOLIDATEDFINANCIALSTATEMENTS

For the years ended December 31, 2005 and 2004, cash flow

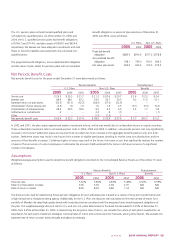

hedges impacted Accumulated other comprehensive loss as follows:

2005 2004

Net derivative losses at beginning of year $ (4.7) $(1.6)

Net losses on derivative instruments,

net of taxes of $3.4 and $.5 (17.6) (1.6)

Reclassification of net losses (gains)

to earnings, net of taxes of $5.8 and $1.5 21.0 (1.5)

Net derivative losses at end of year,

net of taxes of $.4 and $2.8 $ (1.3) $(4.7)

We use foreign currency forward contracts and foreign currency-

denominated debt to hedge the foreign currency exposure related to

the net assets of certain of our foreign subsidiaries. At December 31,

2005, we had a Japanese yen-denominated note payable to hedge

our net investment in our Japanese subsidiary (see Note 4, Debt and

Other Financing). For the years ended December 31, 2005, 2004 and

2003, $8.0, $10.4 and $9.2, respectively, related to the effective por-

tions of these hedges were included in foreign currency translation

adjustments within accumulated other comprehensive loss on the

Consolidated Balance Sheets.

During 2005 and 2004, we held foreign currency forward

contracts and options to protect against the adverse effects that

exchange rate fluctuations may have on the earnings of certain of

our foreign subsidiaries. These derivatives do not qualify for hedge

accounting and, therefore, the gains and losses on these deriva-

tives have been recognized in earnings each reporting period and

are not material to the Consolidated Financial Statements.

At December 31, 2005 and 2004, we held foreign currency

forward contracts and option contracts with fair values total-

ing $2.5 and $5.0, respectively, recorded in accounts payable.

Additionally, certain of our international subsidiaries hold U.S.

dollar-denominated assets, primarily to minimize foreign-currency

risk and provide liquidity.

Credit and Market Risk

We attempt to minimize our credit exposure to counterparties by

entering into interest rate swap and foreign currency forward rate

and option agreements only with major international financial

institutions with “A” or higher credit ratings as issued by Standard

& Poor’s Corporation. Our foreign currency and interest rate

derivatives are comprised of over-the-counter forward contracts,

swaps or options with major international financial institutions.

Although our theoretical credit risk is the replacement cost at the

then estimated fair value of these instruments, we believe that the

risk of incurring credit risk losses is remote and that such losses, if

any, would not be material.

Non-performance of the counterparties on the balance of all the

foreign exchange and interest rate agreements would result in a

write-off of $5.2 at December 31, 2005. In addition, in the event

of non-performance by such counterparties, we would be exposed

to market risk on the underlying items being hedged as a result of

changes in foreign exchange and interest rates.

Fair Value of Financial Instruments

The fair value of a financial instrument is the amount at which the

instrument could be exchanged in a current transaction between

willing parties, other than in a forced sale or liquidation.

The methods and assumptions used to estimate fair value are

as follows:

Equity and fixed-income securities The fair values of these invest-

ments were based on the quoted market prices for issues listed on

securities exchanges.

Debt maturing within one year and long-term debt The fair values

of all debt and other financing were determined based on quoted

market prices.

Foreign exchange forward and option contracts The fair values of

forward and option contracts were determined based on quoted

market prices from banks.

Interest rate swap and treasury lock agreements The fair values of

interest rate swap and treasury lock agreements were estimated

based on quotes from market makers of these instruments and

represent the estimated amounts that we would expect to receive

or pay to terminate the agreements.

The asset (liability) amounts recorded in the balance sheet (carry-

ing amount) and the estimated fair values of financial instruments

at December 31 consisted of the following:

2005 2004

Carrying Fair Carrying Fair

Amount Value Amount Value

Cash and cash equivalents $1,058.7 $1,058.7 $ 769.6 $ 769.6

Equity securities – – 34.1 34.1

Fixed-income securities 17.1 17.1 17.9 17.9

Grantor trust cash and

cash equivalents 34.4 34.4 .3 .3

Debt maturing within

one year (882.5) (882.5) (51.7) (51.7)

Long-term debt, net of related

discount or premium (766.1) (776.1) (865.7) (903.5)

Foreign exchange forward

and option contracts 2.5 2.5 5.0 5.0

Interest rate swap and treasury

lock agreements 2.7 2.7 22.5 22.5

Unrealized gains of $0 and $3.0 on equity securities were recorded

in accumulated other comprehensive loss at December 31, 2005

and 2004, respectively.