Avon 2001 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2001 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

|

|

PAGE 62

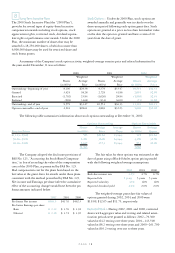

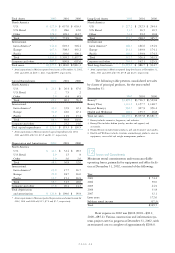

For 2002, the assumed rate of future increases in the

per capita cost of health care benefits (the health care cost

trend rate) was 8% for pre-age 65 claims and post-age 65

claims and will gradually decrease each year thereafter to

5.0% in 2005 and beyond. A one-percentage point change

in the assumed health care cost trend rates would have the

following effects:

1 Percentage 1 Percentage

(In millions) Point Increase Point Decrease

Effect on total of

service and interest

cost components $ .3 $ (.3)

Effect on postretirement

benefit obligation 3.2 (3.2)

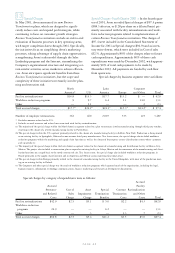

Supplemental Retirement Programs > Avon offers a Deferred

Compensation Plan (the “Plan”) for those employees who

are eligible to participate in the Company’s Long Term

Incentive Plan and are on the U.S. payroll. The Plan is an

unfunded, unsecured plan for which obligations are paid

to participants out of the Company’s general assets,

including assets held in a grantors trust, described below,

and corporate-owned life insurance policies. The Plan

allows for the deferral of all or part of a participant’s base

salary, incentive compensation bonuses and any excess per-

sonal savings account contributions over specified annual

limits up to 6% of base salary. Participants may elect to

have their deferred compensation invested in one or more

of four investment alternatives. Expense associated with

the Plan for the years ended December 31, 2002, 2001

and 2000, was $5.3, $5.4 and $5.0, respectively. At

December 31, 2002, the accrued cost for deferred compen-

sation plan was $75.9 (2001–$72.0) and was included in

Other liabilities.

Avon maintains a supplemental retirement program

consisting of a Supplemental Executive Retirement and

Life Plan (“SERP”) and a Benefits Restoration Pension

Plan (“Restoration Plan”) under which non-qualified sup-

plemental pension benefits are paid to higher paid

employees in addition to amounts received under Avon’s

qualified retirement plan which is subject to IRS limita-

tions on covered compensation. The annual cost of this

program has been included in the determination of the net

periodic benefit cost shown above and in 2002 amounted

to $9.7 (2001–$10.5, 2000–$10.2). The benefit obliga-

tion under this program at December 31, 2002 was $40.6

(2001–$35.5) and was primarily included in Employee

Benefit Plans.

Avon also maintains a Supplemental Life Insurance

Plan (“SLIP”) under which additional death benefits rang-

ing from $.35 to $2.0 are provided to certain active and

retired officers.

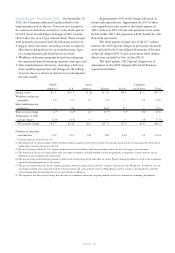

Avon established a grantors trust to provide funding

for the benefits payable under the SERP and SLIP and to

provide for funding of obligations under Avon’s Deferred

Compensation Plan. The trust is irrevocable and, although

subject to creditors’ claims, assets contributed to the trust

can only be used to pay such benefits with certain excep-

tions. The assets held in the trust at December 31, 2002,

amounting to $77.2 (2001–$88.7), consisted of a fixed-

income portfolio, a managed portfolio of equity securities,

corporate-owned life insurance policies and cash and cash

equivalents. These assets are included in Other assets. The

cash surrender value of the corporate-owned life insurance

policies at December 31, 2002 was $27.6 (2001–$26.6).

Additionally, Avon held assets at December 31,

2002 amounting to $10.1 to fund other benefit payments.

The assets consisted of corporate-owned life insurance

policies with a cash surrender value of $8.3 and mutual

funds with a market value of $1.8.

The equity securities and fixed-income portfolio

included in the grantors trust and the mutual funds, dis-

cussed above, are classified as available-for-sale and

recorded at current market value. In 2002 and 2001, net

unrealized gains and losses on these securities were

recorded in Accumulated other comprehensive loss (see

Note 5, Accumulated Other Comprehensive Loss).

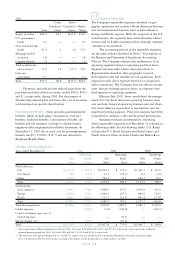

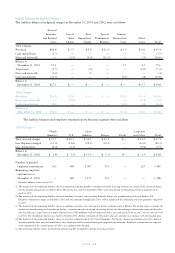

The cost, gross unrealized gains and losses and

market value of the available-for-sale securities as of

December 31, were as follows:

2002

Gross Gross

Unrealized Unrealized Market

Cost Gains Losses Value

Equity securities $44.0 $ .7 $(20.8) $23.9

U.S. government

bonds* 2.3 .1 — 2.4

State and municipal

bonds* 20.1 1.0 — 21.1

Mortgage backed

securities* .7 .1 — .8

Other 3.8 — (1.2) 2.6

Total available-for-

sale securities 70.9 1.9 (22.0) 50.8

Cash and

equivalents .6 — — .6

Total $71.5 $1.9 $(22.0) $51.4

* At December 31, 2002, investments with scheduled maturities in two to

five years totaled $11.0 and after five years totaled $12.1.

Payments, proceeds and net realized losses from the

purchases and sales of these securities totaled $30.4, $33.8

and $.5, respectively, during 2002.