Asus 2008 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2008 Asus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

|

|

93

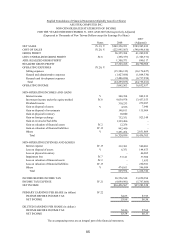

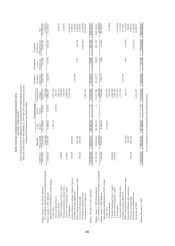

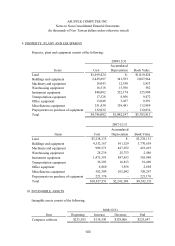

ASUSTEK COMPUTER INC.

Notes to Non-Consolidated Financial Statements

(In thousands of New Taiwan dollars unless otherwise stated)

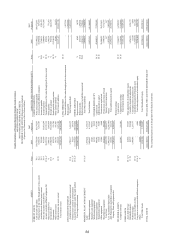

As the bondholder exercises the right to convert the bonds, the book value of the

bonds and the related assets and liabilities are transferred to capital stock and paid-in

capital; no gain or loss is recognized on bond conversion under the par value method.

(2) For bonds issued after January 1, 2006, the policy conforming with the R.O.C. SFAS No.

36 and Interpretation No. 95-290, 97-331, 98-046 by Accounting Research and

Development Foundation consists of the following:

The issuance costs are allocated to the related liability and equity components based

on the proportion of the initially recognized amounts.

Convertible bonds with the clause of adjusting price based on market price do not

include the equity component. In the aspect of the liability component, the fair value

of conversion right with clause of adjusting price and call/put options shall be

measured first; then the book value of main liability is assigned with the residual

amount after deducting the fair value of conversion right with clause of adjusting

price and call/put options from issue price.

Convertible bonds are subsequently measured at amortized cost. Derivatives with

call/put options and conversion right with clause of adjusting price are recognized as

“financial liabilities at fair value through profit or loss” and are subsequently measured

at the fair value. The movements in the fair value of the derivatives would be

recognized as “gain/(loss) on valuation of financial liabilities”.

As the bondholder exercises the right to convert the bonds ahead of the due date of

the bonds, the Company shall adjust the book value of the liability components to the

value on the conversion date, which would be the recording basis of common stocks

to be issued without recognizing conversion gain and loss.

If the bondholder could exercise the put option within one year, the bonds payable

should be reclassified as current liability. Those bonds payable could be reclassified

as long-term liability when the put option expires and the liability meets the definition

of long-term liability.

11. Accrued pension liability

The Company makes monthly contributions to the pension fund at 2% of the total monthly

salaries and wages as required by the Labor Standards Laws. The fund is administrated by

the Employees Retirement Fund Committee. The pension fund mentioned above is

considered absolutely separate from the Company after contribution; therefore, it is not

included in the accompanying financial statements.