Asus 2008 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2008 Asus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

|

|

91

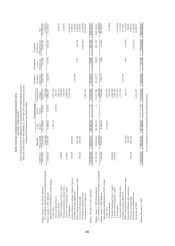

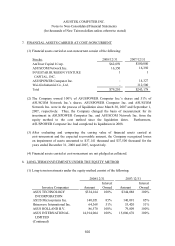

ASUSTEK COMPUTER INC.

Notes to Non-Consolidated Financial Statements

(In thousands of New Taiwan dollars unless otherwise stated)

6. Long-term investments under the equity method

(1) The difference between the acquisition cost and the Company’s share of net assets of the

investee is analyzed and accounted for in the manner similar to acquisition cost

allocation as provided in the R.O.C. SFAS No. 25 “Business Combinations-Accounting

Treatment under Purchase Method” under which goodwill is no longer amortized.

(2) When the Company has control or significant influence over an investee company, the

Company shall account for such investment under the equity method.

(3) If certain long-term equity investments have incurred existing or extremely probable

losses, the Company shall recognize investment loss in proportion to the percentage of

ownership. The investment loss recognized shall first bring down the specific

investment and receivables accounts to zero, then the remaining loss, if any, will be

recorded as “Other liabilities-credit to long-term investments”.

(4) Unrealized intercompany gains or losses arising from transactions between affiliated

companies shall be eliminated. Unrealized gross profits from downstream sales shall be

debited to “unrealized gross profits” and credited to “deferred credits”, whereas

unrealized gross profits from upstream and side-stream sales shall be debited to

“investment loss” and credited to “long-term investments”.

(5) When the Company issues new shares to acquire another company’s shares, the carrying

amount of the investment shall be either the fair market value of the Company’s shares

or the fair market value of the investee’s shares, whichever is more objective and

determinable. If the carrying amount will be over or under the par value of the

Company’s shares, the difference shall be credited to additional paid-in capital or debited

to additional paid-in capital (then debited to retained earnings when additional paid-in

capital is insufficient). The fair market value of the listed shares of investee companies in

which the Company has now obtained control shall be based on the quoted prices over a

reasonable period before or after the announcement of the acquisition is made.

7. Property, plant and equipment and assets held for lease

(1) Property, plant and equipment and assets held for lease are carried at cost.

Expenditures for regular repairs and maintenance are charged against operating income.

However, improvements that materially extend the useful lives of the assets are

capitalized.