TCF Bank 2001 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2001 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

|

|

67

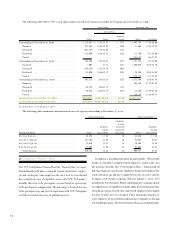

loans held for sale. In accordance with fair value hedge accounting

under SFAS No. 133, the forward sales contracts hedging the resi-

dential loans held for sale are recorded at fair value, with changes in

fair value recognized in gains on sales of loans held for sale as is the

offsetting change in the fair value of the hedged loans.

The impact of adopting SFAS No. 133 on TCF’s financial posi-

tion was not material. A transition adjustment of $117,000 was

recorded in other income in the consolidated statements of income

on January 1, 2001. During 2001, the ineffectiveness of the fair

value hedges was not material. Forward mortgage loan sales commit-

ments totaled $490.9 million and $121.7 million at December 31,

2001 and 2000, respectively.

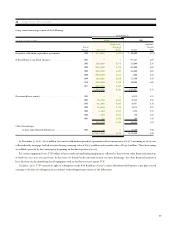

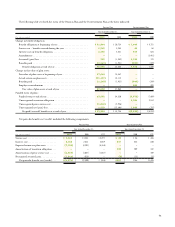

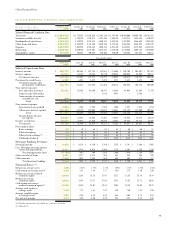

19 Financial Instruments with

Off-Balance-Sheet Risk

TCF is a party to financial instruments with off-balance-sheet risk,

primarily to meet the financing needs of its customers. These finan-

cial instruments, which are issued or held by TCF for purposes other

than trading, involve elements of credit and interest-rate risk in

excess of the amount recognized in the Consolidated Statements of

Financial Condition.

TCF’s exposure to credit loss in the event of non-performance

by the counterparty to the financial instrument for commitments to

extend credit and standby letters of credit is represented by the con-

tractual amount of the commitments. TCF uses the same credit poli-

cies in making these commitments as it does for on-balance-sheet

instruments. TCF evaluates each customer’s creditworthiness on a

case-by-case basis. The amount of collateral obtained is based on

management’s credit evaluation of the customer.

COMMITMENTS TO EXTEND CREDIT – Commitments to

extend credit are agreements to lend to a customer provided there is

no violation of any condition in the contract. These commitments

generally have fixed expiration dates or other termination clauses and

may require payment of a fee. At December 31, 2001 these commit-

ments totaled $1.6 billion and consisted of consumer commitments

of $955.7 million, commercial commitments of $494.5 million,

leasing and equipment financing commitments of $71.6 million and

other commitments of $32.5 million. At December 31, 2000 these

commitments totaled $1.2 billion and consisted of consumer com-

mitments of $706.9 million, commercial commitments of $411.3

million, leasing and equipment finance commitments of $71.6 mil-

lion and other commitments of $47 million. Since certain of the

commitments are expected to expire without being drawn upon, the

total commitment amounts do not necessarily represent future cash

requirements. Collateral predominantly consists of residential and

commercial real estate and personal property.

STANDBY LETTERS OF CREDIT – Standby letters of credit are

conditional commitments issued by TCF guaranteeing the perfor-

mance of a customer to a third party. The standby letters of credit

expire in various years through the year 2003 and totaled $12.7 mil-

lion and $28.8 million at December 31, 2001 and 2000, respec-

tively. Collateral held primarily consists of commercial real estate

mortgages. Since the conditions under which TCF is required to

fund standby letters of credit may not materialize, the cash require-

ments are expected to be less than the total outstanding commitments.

VA LOANS SERVICED WITH PARTIAL RECOURSE – TCF

services VA loans on which it must cover any principal loss in excess of

the VA’s guarantee if the VA elects its “no-bid” option upon the fore-

closure of a loan. The liability relating to the loans serviced with par-

tial recourse was $100,000 and $100,000 at December 31, 2001 and

2000, respectively and was recorded in other liabilities. The serviced

loans are collateralized by residential real estate and totaled $179.7 mil-

lion and $182.1 million at December 31, 2001 and 2000, respectively.

FEDERAL HOME LOAN BANK ADVANCES – FORWARD

SETTLEMENTS – TCF enters into forward settlements of FHLB

advances in the course of asset and liability management and to manage

interest rate risk. There were no forward settlements of FHLB advances

at December 31, 2001. Forward settlements of FHLB advances totaled

$300 million at December 31, 2000.

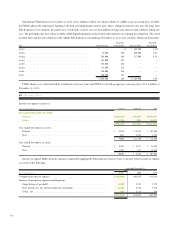

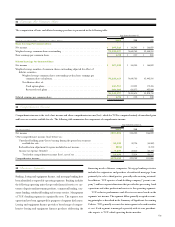

20 Fair Values of Financial Instruments

TCF is required to disclose the estimated fair value of financial instru-

ments, both assets and liabilities on and off the balance sheet, for which

it is practicable to estimate fair value. Fair value estimates are made at

a specific point in time, based on relevant market information and

information about the financial instruments. Fair value estimates are

subjective in nature, involving uncertainties and matters of signifi-

cant judgment, and therefore cannot be determined with precision.

Changes in assumptions could significantly affect the estimates.

The carrying amounts of cash and due from banks, investments and

accrued interest payable and receivable approximate their fair values

due to the short period of time until their expected realization. Securities

available for sale are carried at fair value, which is based on quoted mar-

ket prices. Certain financial instruments, including lease financings

and discounted lease rentals, and all non-financial instruments are

excluded from fair value of financial instrument disclosure requirements.

The following methods and assumptions are used by the Company

in estimating fair value disclosures for its remaining financial instru-

ments, all of which are issued or held for purposes other than trading.