TCF Bank 2001 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2001 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

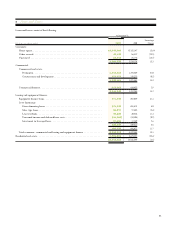

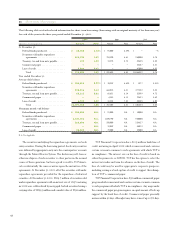

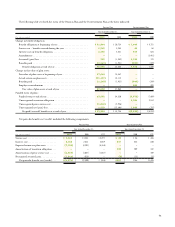

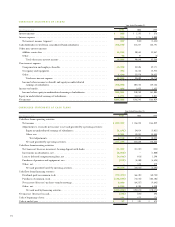

At December 31, 2001, TCF and its bank subsidiaries exceeded

their regulatory capital requirements and are considered “well-

capitalized” under guidelines established by the FRB and the OCC

pursuant to the Federal Deposit Insurance Corporation Improvement

Act of 1991.

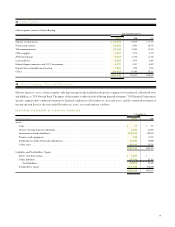

16 Stock Option and Incentive Plan

The TCF Financial 1995 Incentive Stock Program (the “Program”)

was adopted to enable TCF to attract and retain key personnel. Under

the Program, no more than 5% of the shares of TCF common stock

outstanding on the date of initial shareholder approval may be

awarded. At December 31, 2001, there were 2,881,069 shares reserved

for issuance under the Program, including 370,125 shares related to

outstanding stock options.

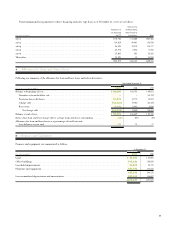

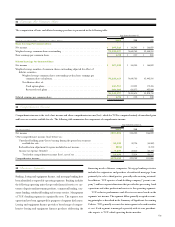

Restricted stock granted to certain executive officers in 2000 will

vest only if certain earnings per share goals are achieved by 2008.

Failure to achieve the goals will result in all or a portion of the shares

being forfeited. Other restricted stock grants generally vest over peri-

ods from three to eight years.

TCF also has prior programs with options that remain outstand-

ing. Those options are included in the following tables. Options gen-

erally become exercisable over a period of one to 10 years from the

date of the grant and expire after 10 years. All outstanding options

have a fixed exercise price equal to the market price of TCF common

stock on the date of grant.

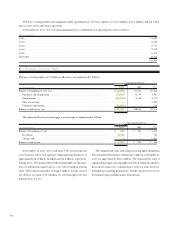

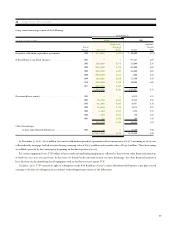

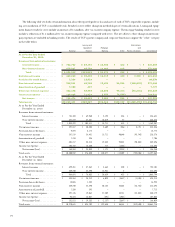

ACCOUNTING FOR STOCK-BASED COMPENSATION –

Effective January 1, 2000, TCF adopted the recognition provisions

of SFAS No. 123, “Accounting for Stock-Based Compensation,” for

stock-based grants beginning in 2000. Under SFAS No. 123, the

fair value of an option or similar equity instrument on the date of

grant is amortized to expense over the vesting period of the grant.

The recognition provisions of SFAS No. 123 were applied prospec-

tively upon adoption. TCF applied the intrinsic value based method

of accounting prescribed by Accounting Principles Board (“APB”)

Opinion No. 25, “Accounting for Stock Issued to Employees,” as

amended, for stock-based transactions through December 31, 1999.

Accordingly, no compensation expense was recognized prior to 2000

for TCF’s stock option grants.

TCF believes the fair value method of accounting more appro-

priately reflects the substance of the transaction between an entity

that issues stock options, or other stock-based instruments, and its

employees; that is, an entity has granted something of value to an

employee generally in return for their continued employment and

services. The fair value based method is designated as the preferred

method of accounting by SFAS No. 123.

Compensation expense for restricted stock under SFAS No. 123

and APB Opinion No. 25 is recorded over the vesting periods, and

totaled $11.1 million, $9.4 million and $9.5 million in 2001, 2000

and 1999, respectively.

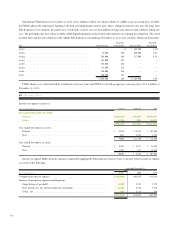

Had compensation expense for all periods been determined based

on the fair value at the grant dates for awards under the Program con-

sistent with the method of SFAS No. 123, TCF’s pro forma net income

and diluted earnings per common share would have been $164.6 mil-

lion and $1.98, respectively, for the year ended December 31, 1999.

The fair value of each option grant is estimated on the grant date

using the Black-Scholes option pricing model, with the following

weighted-average assumptions used for 1999: risk-free interest rates

of 5.03%; dividend yield of 2.7%; expected lives of 7 years; and

volatility of 27.0%.

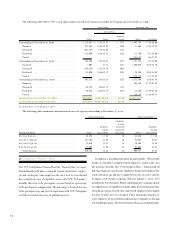

The weighted-average grant date fair value of options was $6.59

and $7.02 in 2000 and 1999, respectively. No options were granted

in 2001. The weighted-average grant date fair value of restricted stock

was $39.53, $24.60 and $25.94 in 2001, 2000 and 1999, respectively.

63