TCF Bank 2000 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 2000 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

|

|

4

TCF

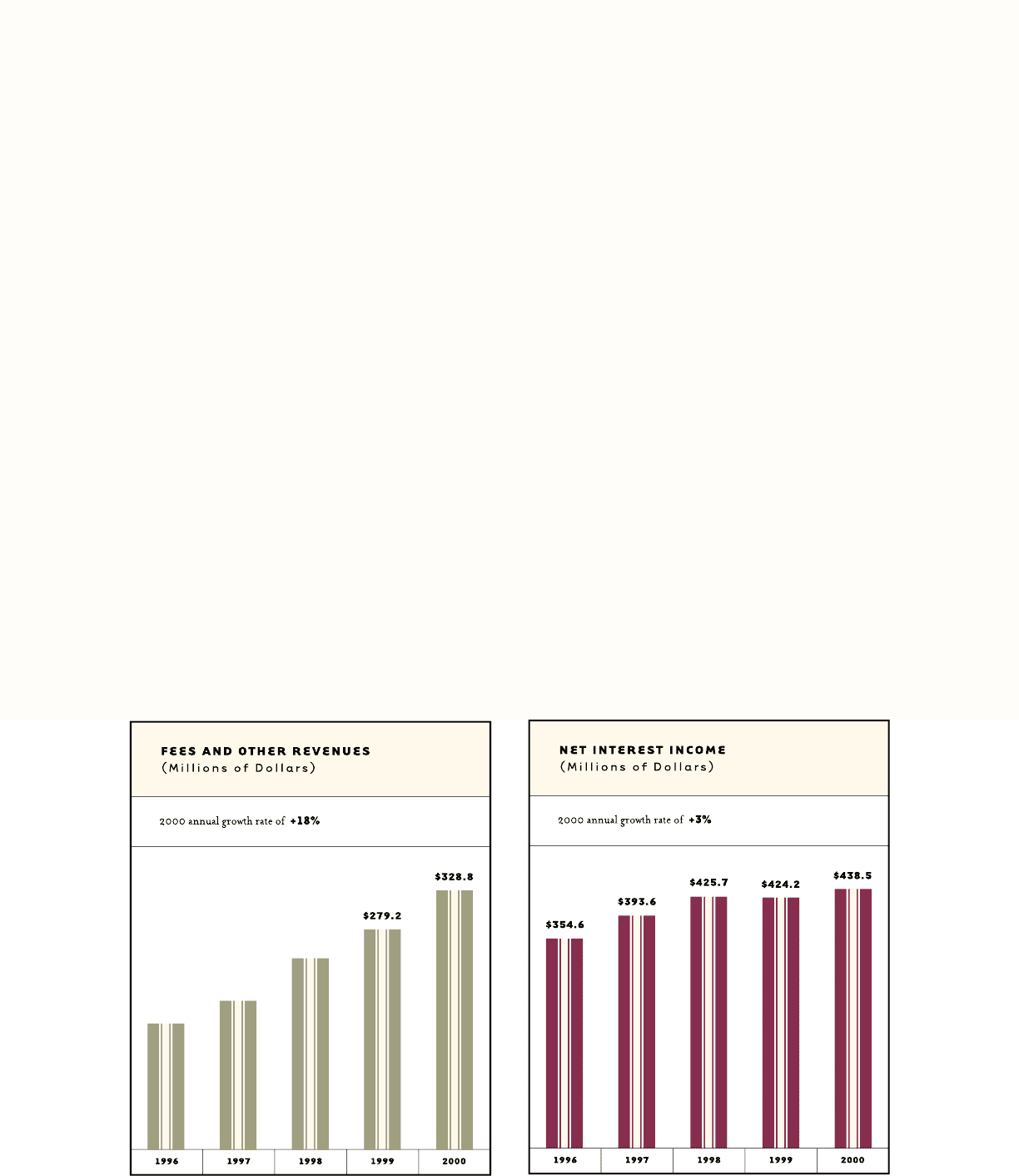

for us. It demonstrates that we are growing our core

businesses, not just cutting expenses as many of our

competitors are doing. We believe that growing busi-

nesses generate premium price-to-earnings ratios.

Growth in top-line revenue results from increas-

ing Power Assets and Power Liabilities. Net interest

income growth is driven by a changed balance sheet.

Fee income growth is fueled by expanding the num-

ber of fee income producing products and services

while growing the overall customer base. TCF added

nearly 100,000 new checking accounts in 2000,

bringing our total to 1,131,000. We now have 1.1 mil-

lion debit cards outstanding (the 16th largest Visa

debit card issuer in the United States).

TCF believes in attracting a large number of cus-

tomers from all economic levels. We believe that

each of these customers contributes incrementally

to our profitability. Unlike many of our competi-

tors, we do not believe in the old 80/20 rule which

suggests that banks earn 80 percent of their profits

from the wealthiest 20 percent of the customer base.

At TCF, a big number multiplied by a little num-

ber is a big number.

Power Assets and Power Liabilities We enjoyed record

growth in our Power Assets, up $896.8 million for

the year, a 23 percent increase from year-end 1999.

Commercial lending, consumer lending, and leas-