Supercuts 2011 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2011 Supercuts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

|

|

Table of Contents

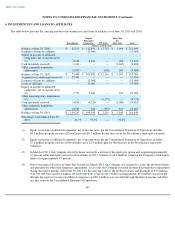

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

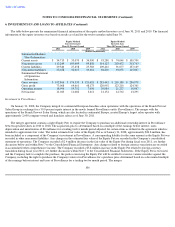

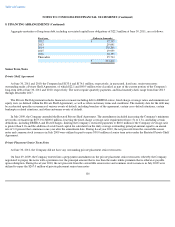

6. INVESTMENTS IN AND LOANS TO AFFILIATES (Continued)

agreement also contains an option (Equity Call) whereby the Company can acquire additional ownership interest in Provalliance between

specific dates in 2018 to 2020 at an acquisition price determined consistent with the Equity Put.

In December 2010, a portion of the Equity Put was exercised. In March of 2011, the Company elected to honor and settle a portion of the

Equity Put and acquired approximately 17 percent additional equity interest in Provalliance for $57.3 million (approximately € 40.4 million),

bringing the Company's total equity interest to 46.7 percent. Upon the acquisition of the additional ownership interest, the Company recognized a

net gain of approximately $2.4 million representing the reversal of the Equity Put liability that was extinguished upon settlement, partially offset

by an increase in the fair value of the remaining Equity Put. The Company's liability under the Equity Put to purchase the remainder of the equity

interest in Provalliance continues to exist through 2018 and is valued at $22.7 million as of June 30, 2011.

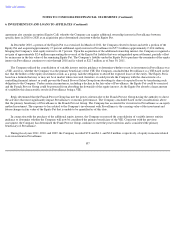

The Company utilized the consolidation of variable interest entities guidance to determine whether or not its investment in Provalliance was

a VIE, and if so, whether the Company was the primary beneficiary of the VIE. The Company concluded that Provalliance is a VIE based on the

fact that the holders of the equity investment at risk, as a group, lack the obligation to absorb the expected losses of the entity. The Equity Put is

based on a formula that may or may not be at market when exercised, therefore, it could provide the Company with the characteristic of a

controlling financial interest or could prevent the Franck Provost Salon Group from absorbing its share of expected losses by transferring such

obligation to the Company. Under certain circumstances, including a decline in the fair value of Provalliance, the Equity Put could be exercised

and the Franck Provost Group could be protected from absorbing the downside of the equity interest. As the Equity Put absorbs a large amount

of variability this characteristic results in Provalliance being a VIE.

Regis determined that the Franck Provost Group has met the power criterion due to the Franck Provost Group having the authority to direct

the activities that most significantly impact Provalliance's economic performance. The Company concluded based on the considerations above

that the primary beneficiary of Provalliance is the Franck Provost Group. The Company has accounted for its interest in Provalliance as an equity

method investment. The exposure to loss related to the Company's involvement with Provalliance is the carrying value of the investment and

future changes in fair value of the Equity Put that is unable to be quantified as of this date.

In connection with the purchase of the additional equity interest, the Company reassessed the consolidation of variable interest entities

guidance to determine whether the Company will now be considered the primary beneficiary of the VIE. Consistent with the previous

assessment, the Company has determined the Frank Provost Group continues to meet the power criterion and is considered the primary

beneficiary of Provalliance.

During fiscal years 2011, 2010, and 2009, the Company recorded $7.8 and $4.1, and $2.0 million, respectively, of equity in income related

to its investment in Provalliance.

107