Foot Locker 2009 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2009 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

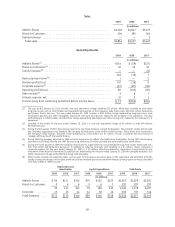

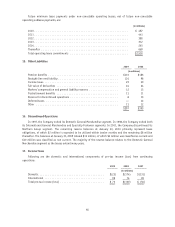

Items that gave rise to significant portions of the deferred tax accounts are as follows:

2009 2008

(in millions)

Deferred tax assets:

Tax loss/credit carryforwards and capital loss .................... $106 $ 37

Employee benefits ...................................... 66 102

Reserve for discontinued operations .......................... 4 5

Repositioning and restructuring reserves ....................... 1 1

Property and equipment .................................. 177 184

Allowance for returns and doubtful accounts ..................... 1 1

Straight-line rent ....................................... 27 25

Goodwill ............................................. 23 25

Other ............................................... 32 28

Total deferred tax assets .................................... 437 408

Valuation allowance ..................................... (12) (13)

Total deferred tax assets, net ............................. 425 395

Deferred tax liabilities:

Inventories ........................................... 46 22

Other ............................................... 5 8

Total deferred tax liabilities ................................. 51 30

Net deferred tax asset ..................................... $374 $365

Balance Sheet caption reported in:

Deferred taxes ......................................... $362 $358

Other current assets ..................................... 17 29

Other current liabilities ................................... (5) (10)

Other liabilities ........................................ — (12)

$374 $365

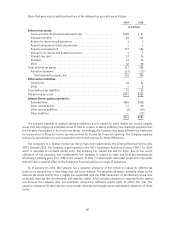

The Company operates in multiple taxing jurisdictions and is subject to audit. Audits can involve complex

issues that may require an extended period of time to resolve. A taxing authority may challenge positions that

the Company has adopted in its income tax filings. Accordingly, the Company may apply different tax treatments

for transactions in filing its income tax returns than for income tax financial reporting. The Company regularly

assesses its tax positions for such transactions and records reserves for those differences.

The Company’s U.S. Federal income tax filings have been examined by the Internal Revenue Service (the

‘‘IRS’’) through 2008. The Company is participating in the IRS’s Compliance Assurance Process (‘‘CAP’’) for 2009,

which is expected to conclude during 2010. The Company has started the CAP for 2010. Due to the recent

utilization of net operating loss carryforwards, the Company is subject to state and local tax examinations

effectively including years from 1996 to the present. To date, no adjustments have been proposed in any audits

that will have a material effect on the Company’s financial position or results of operations.

As of January 30, 2010, the Company has a valuation allowance of $12 million to reduce its deferred tax

assets to an amount that is more likely than not to be realized. The valuation allowance primarily relates to the

deferred tax assets arising from a capital loss associated with the 2008 impairment of the Northern Group note

receivable, state tax loss carryforwards, and state tax credits. A full valuation allowance is required for the capital

loss because the Company does not anticipate recognizing sufficient capital gains to utilize this loss. The

valuation allowance for state tax loss carryforwards decreased principally due to anticipated expirations of those

losses.

48