Foot Locker 2009 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2009 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

12. Revolving Credit Facility

On March 20, 2009, the Company entered into a credit agreement (the ‘‘2009 Credit Agreement’’) with its

banks, providing for a $200 million asset-based revolving credit facility maturing on March 20, 2013, which

replaced the Company’s prior credit agreement. The 2009 Credit Agreement also provides for an incremental

facility of up to $100 million under certain circumstances. The 2009 Credit Agreement provides for a security

interest in certain of the Company’s domestic assets, including certain inventory assets. The Company is not

required to comply with any financial covenants as long as there are no outstanding borrowings. If the Company

is borrowing, then it may not make Restricted Payments, such as dividends or share repurchases, unless there is at

least $50 million of Excess Availability (as defined in the 2009 Credit Agreement), and the Company’s projected

fixed charge coverage ratio, which is a Non-GAAP financial ratio pursuant to the 2009 Credit Agreement designed

as a measure of the Company’s ability to meet current and future obligations (Consolidated EBITDA less capital

expenditures less cash taxes divided by Debt Service Charges and Restricted Payments), is at least 1.1 to 1.0. The

Company’s management does not currently expect to borrow under the facility in 2010.

At January 30, 2010, the Company had unused domestic lines of credit of $190 million pursuant to its

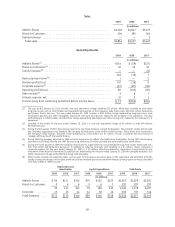

$200 million revolving credit agreement, of which $10 million was committed to support standby letters of credit.

The letters of credit are primarily used for insurance programs.

Deferred financing fees are amortized over the life of the facility on a straight-line basis, which is

comparable to the interest method. The unamortized balance at January 30, 2010 is $6.6 million. Interest is

based on the LIBOR rate in effect at the time of the borrowing plus a 3.25 to 3.75 percent applicable margin, as

defined in the 2009 Credit Agreement. The quarterly facility fees paid on the unused portion ranged from

0.40 percent to 0.75 percent for 2009 and 2008. There were no short-term borrowings during 2009 or 2008. The

amounts paid prior to March 20, 2009 relate to the predecessor credit agreement. Interest expense, including

facility fees, related to the revolving credit facility was $3 million and $2 million in 2009 and 2008, respectively.

13. Long-Term Debt

The Company’s long-term debt reflects the Company’s 8.50 percent debentures payable in 2022. The

Company has historically employed various interest rate swaps to minimize its exposure to interest rate

fluctuations. During the first quarter of 2009, the Company terminated the interest rate swaps for a gain of

$19 million. The gain is being amortized as part of interest expense over the remaining term of the debt, using

the effective-yield method. This amortization totaled $1 million in 2009.

The Company’s long term debt was $138 million and $142 million for the years ended January 30, 2010 and

January 31, 2009, respectively. During 2009, the Company purchased and retired $3 million of its 8.50 percent

debentures. Interest expense related to long-term debt, including the effect of the interest rate swaps and the

amortization of the associated debt issuance costs, was $9 million in each of 2009 and 2008, and $18 million in

2007.

14. Leases

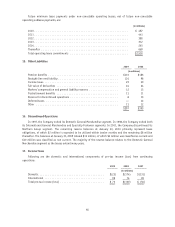

The Company is obligated under operating leases for almost all of its store properties. Some of the store

leases contain renewal options with varying terms and conditions. Management expects that in the normal

course of business, expiring leases will generally be renewed or, upon making a decision to relocate, replaced by

leases on other premises. Operating lease periods generally range from 5 to 10 years. Certain leases provide for

additional rent payments based on a percentage of store sales. Most of the Company’s leases require the payment

of certain executory costs such as insurance, maintenance, and other costs in addition to the future minimum

lease payments. These costs totaled $138 million, $147 million, and $151 million in 2009, 2008 and 2007,

respectively. Included in the amounts below, are non-store expenses that totaled $15 million in both 2009 and

2008 and $16 million in 2007. 2009 2008 2007

(in millions)

Minimum rent ................................... $514 $527 $521

Contingent rent based on sales ....................... 14 14 17

Sublease income ................................. (2) (2) (1)

$526 $539 $537

45