Experian 2012 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2012 Experian annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

97

Governance Financial statementsBusiness reviewBusiness overview

5. Significant accounting policies (continued)

Available for sale financial assets

Available for sale financial assets are non-derivative financial assets that are either designated to this category or not classified in the other

financial asset categories.

Available for sale financial assets are carried at fair value and are included in non-current assets unless management intends to dispose of the

assets within one year of the balance sheet date. Purchases and disposals of such assets are accounted for at settlement date. Unrealised gains

and losses on available for sale financial assets are recognised directly in other comprehensive income. On disposal or impairment of such

assets, the gains and losses in equity are reclassified through the Group income statement. Gains and losses recognised on disposal exclude

dividend and interest income.

At each balance sheet date, the Group assesses whether there is objective evidence to suggest that available for sale financial assets are

impaired. In the case of equity securities, a significant or prolonged decline in the fair value of the security below its cost is considered in

determining whether the security is impaired. If any such evidence exists, the cumulative loss is removed from equity and recognised in the

Group income statement. Impairment losses recognised in the Group income statement on equity instruments are not subsequently reversed

through the Group income statement.

(h) Trade receivables

Trade receivables are initially recognised at fair value and subsequently measured at this value less any provision for impairment. Where the

time value of money is material, receivables are then carried at amortised cost using the effective interest rate method, less any provision for

impairment.

A provision for impairment of trade receivables is established when there is objective evidence that the Group will not be able to collect all

amounts due according to the original terms of receivables. Such evidence is based primarily on the pattern of cash received compared to the

terms upon which the trade receivable is contracted. The amount of the provision is the difference between the carrying amount and the value

of estimated future cash flows. Any charge or credit in respect of such provisions is recognised in the Group income statement within other

operating charges. The cost of any irrecoverable trade receivables not included in the provision is recognised in the Group income statement

immediately within other operating charges. Subsequent recoveries of amounts previously written off are credited in the Group income

statement within other operating charges.

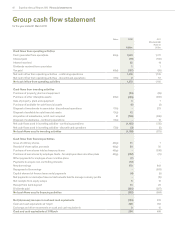

(i) Cash and cash equivalents

Cash and cash equivalents include cash in hand, term and call deposits held with banks and other short-term highly liquid investments with

original maturities of three months or less. Bank overdrafts are shown within borrowings in current liabilities on the Group balance sheet. For the

purposes of the Group cash flow statement, cash and cash equivalents are reported net of bank overdrafts.

(j) Borrowings and borrowing costs

Borrowings are recognised initially at fair value, net of any transaction costs incurred. Borrowings are subsequently stated at amortised cost

except where they are hedged by an effective fair value hedge, in which case the carrying value is adjusted to reflect the fair value movements

associated with the hedged risk.

Borrowings are classified as non-current to the extent that the Group has an unconditional right to defer settlement of the liability for at least one

year after the balance sheet date.

Incremental transaction costs which are directly attributable to the issue of debt are capitalised and amortised over the expected life of the

borrowing using the effective interest rate method. All other borrowing costs are expensed in the year in which they are incurred.

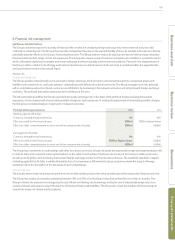

(k) Derivative financial instruments

The Group uses derivative financial instruments to manage its exposures to fluctuations in foreign exchange rates, interest rates and certain

obligations, including social security obligations, relating to share-based payments. Derivative instruments utilised by the Group include interest

rate swaps, cross currency swaps, foreign exchange contracts and equity swaps. These are recognised as assets or liabilities as appropriate.

Derivative financial instruments are initially recognised at their fair value at the date a contract is entered into, and are subsequently remeasured

at their fair value at each reporting date. Depending on the type of the derivative financial instrument, fair value calculation techniques include,

but are not limited to, quoted market value, present value of estimated future cash flows (of which the valuation of interest rate swaps is an

example) and exchange rates at the balance sheet date (of which the valuation of foreign exchange contracts is an example). The method of

recognising the resulting gain or loss depends on whether the derivative is designated as a hedging instrument and, if so, the nature of the

hedge relationship. The Group designates certain derivatives as:

•Fair value hedges - hedges of the fair value of a recognised asset or liability or a firm commitment; or

•Cash flow hedges - hedges of a particular risk associated with a recognised asset or liability or a highly probable forecast transaction; or

•Net investment hedges - hedges of a net investment in an operation whose functional currency is not US dollars.