Xcel Energy 2000 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2000 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

|

|

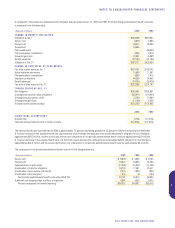

XCEL ENERGY INC. AND SUBSIDIARIES

41

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

In Colorado, PSCo operates under an electric PBRP, which results in an annual earnings test with the sharing of excess earnings between customers and

shareholders. The sharing threshold is earnings in excess of an 11-percent return on equity for 2001 and a 10.50-percent return on equity for 2002. In Texas,

SPS operates under an earnings tests, in which excess earnings above a certain level are returned to the customer.

NSP-Minnesota and PSCo’s rates include monthly adjustments for the recovery of conservation and energy management program costs, which are

reviewed annually.

Trading Operations

Effective with year-end 2000 reporting, Xcel Energy changed its policy for the presentation of energy trading operating results. Previously, trading margins

were recorded net of costs in electric and natural gas revenues. After the merger, Xcel Energy elected to report trading revenues separately from trading costs.

Prior years’ results have been reclassified for consistency with 2000 reporting.

Xcel Energy’s trading operations are conducted mainly by PSCo and e prime. Trading revenues and costs of goods sold do not include the revenue and

production costs associated with energy produced from generation assets or results from NRG.

Property, Plant, Equipment and Depreciation

Property, plant and equipment is stated at original cost. The cost of plant includes direct labor and materials, contracted work, overhead costs and applicable

interest expense. The cost of plant retired, plus net removal cost, is charged to accumulated depreciation and amortization. Significant additions or improvements

extending asset lives are capitalized, while repairs and maintenance are charged to expense as incurred. Maintenance and replacement of items determined

to be less than units of property are charged to operating expenses.

Xcel Energy determines the depreciation of its plant by spreading the original cost equally over the plant’s useful life. Depreciation expense, expressed as

a percentage of average depreciable property, was approximately 3.3 percent for the years ended Dec. 31, 2000, 1999 and 1998.

Property, plant and equipment includes approximately $18 million and $25 million, respectively, for costs associated with the engineering design of the

future Pawnee 2 generating station and certain water rights located in southeastern Colorado, also obtained for a future generating station. PSCo is earning

a return on these investments based on its weighted average cost of debt in accordance with a CPUC rate order.

Allowance for Funds Used During Construction (AFDC)

AFDC, a noncash item, represents the cost of capital used to finance utility construction activity. AFDC is computed by applying a composite pretax rate to

qualified construction work in progress. The amount of AFDC capitalized as a utility construction cost is credited to other income and expense (for equity

capital) and interest charges (for debt capital). AFDC amounts capitalized are included in Xcel Energy’s rate base for establishing utility service rates. In

addition to construction-related amounts, AFDC also is recorded to reflect returns on capital used to finance conservation programs in Minnesota. Interest

capitalized as AFDC was approximately $20 million in 2000, $19 million in 1999 and $25 million in 1998.

Decommissioning

Xcel Energy accounts for the future cost of decommissioning – or permanently retiring – its nuclear generating plants through annual depreciation accruals using

an annuity approach designed to provide for full-rate recovery of the future decommissioning costs. Our decommissioning calculation covers all expenses, including

decontamination and removal of radioactive material, and extends over the estimated lives of the plants. The calculation assumes that NSP-Minnesota and

NSP-Wisconsin will recover those costs through rates. For more information on nuclear decommissioning, see Note 15 to the Financial Statements.

Nuclear Fuel Expense

Nuclear fuel expense, which is recorded as the plant uses fuel, includes the cost of nuclear fuel used and future spent nuclear fuel disposal, based on fees estab-

lished by the U.S. Department of Energy (DOE) and NSP-Minnesota’s portion of the cost of decommissioning or shutting down the DOE’s fuel enrichment facility.

Environmental Costs

We record environmental costs when it is probable Xcel Energy is liable for the costs and we can reasonably estimate the liability. We may defer costs as

a regulatory asset based on our expectation that we will recover these costs from customers in future rates. Otherwise, we expense the costs. If an environmental

expense is related to facilities we currently use, such as pollution control equipment, we capitalize and depreciate the costs over the life of the plant, assuming

the costs are recoverable in future rates or future cash flows.

We record estimated remediation costs, excluding inflationary increases and possible reductions for insurance coverage and rate recovery. The estimates

are based on our experience, our assessment of the current situation and the technology currently available for use in the remediation. We regularly adjust

the recorded costs as we revise estimates and as remediation proceeds. If we are one of several designated responsible parties, we estimate and record

only our share of the cost. We treat any future costs of restoring sites where operation may extend indefinitely as a capitalized cost of plant retirement.

The depreciation expense levels we can recover in rates include a provision for these estimated removal costs.