WeightWatchers 2009 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2009 WeightWatchers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

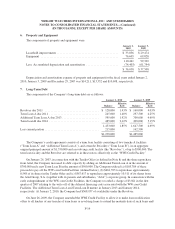

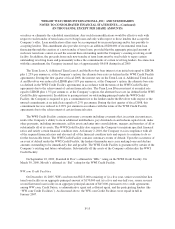

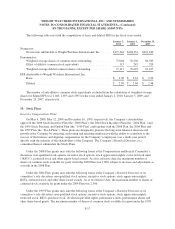

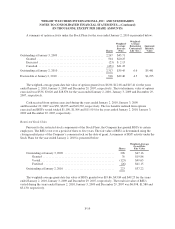

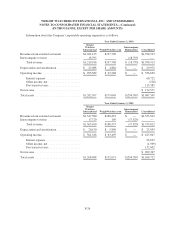

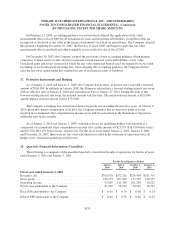

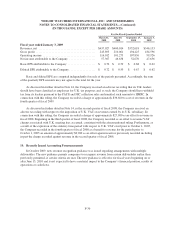

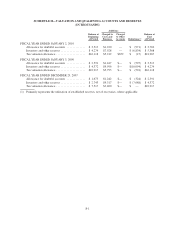

WEIGHT WATCHERS INTERNATIONAL, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(IN THOUSANDS, EXCEPT PER SHARE AMOUNTS)

Accordingly, the Company filed notices of appeal with the VAT Tribunal against the U.K. VAT assessments

issued for the periods October 1, 2005 to December 31, 2005, January 1, 2006 to March 31, 2006, April 1, 2006

to June 30, 2006 and July 1, 2006 to September 30, 2006 in March 2009, April 2009, July 2009 and October

2009, respectively.

U.K. Self-Employment Matter

In July 2007, HMRC issued to the Company notices of determination and decisions that, for the period April

2001 to April 2007, its leaders and certain other service providers should have been classified as employees for

tax purposes and, as such, the Company should have withheld tax from the leaders and certain other service

providers pursuant to the “Pay As You Earn” (“PAYE”) and national insurance contributions (“NIC”) collection

rules and remitted such amounts to HMRC. HMRC also issued a claim to the Company in October 2008 in

respect of NIC which corresponds to the prior notices of assessment with respect to PAYE previously raised by

HMRC.

In September 2007, the Company appealed HMRC’s notices as to these classifications and against any

amount of PAYE and NIC liability claimed to be owed by the Company and, in July 2008, filed this appeal with

the U.K. First Tier Tribunal (Tax Chamber) (the “First Tier Tribunal”). The Company’s appeal was heard by the

First Tier Tribunal in June 2009 and October 2009. In February 2010, the First Tier Tribunal issued a ruling that

the Company’s U.K. leaders should have been classified as employees for U.K. tax purposes and, as such, the

Company should have withheld tax from its leaders pursuant to the PAYE and NIC collection rules for the period

from April 2001 to April 2007 with respect to services performed by the leaders for the Company.

In light of this adverse ruling and in accordance with accounting guidance for contingencies, the Company

recorded in the fourth quarter of fiscal 2009 a charge in the amount of approximately $36.7 million for the period

from April 2001 through the end of fiscal 2009, inclusive of estimated accrued interest. Although the Company

intends to seek an appeal of this adverse ruling, in accordance with accounting guidance for contingencies, the

Company will record a reserve each quarter beginning in the first quarter of fiscal 2010 for U.K. withholding

taxes with respect to its U.K. leaders consistent with the First Tier Tribunal’s ruling.

Sabatino v. Weight Watchers North America, Inc.

In September 2009, a lawsuit was filed in the Superior Court of California by one of the Company’s former

leaders alleging violations of certain California wage and hour laws on behalf of herself, and, if approved by the

Court, other leaders and those employees who have performed the location coordinator function in California

since September 17, 2005. In this matter, the plaintiff is seeking unpaid wages and certain other damages. In

October 2009, the Company answered the complaint and removed the case to the U.S. District Court for the

Northern District of California. Although the Company disagrees with the allegations that it has violated

California wage and hour laws and the Company believes it has valid defenses with respect to this matter,

litigation is inherently unpredictable. At this time, it is not possible to determine the outcome of, or estimate the

liability related to, this action and the Company has not made any provision for losses in connection with it.

Hanson-Kelly & Jackson v. Weight Watchers North America, Inc. and Weight Watchers International, Inc.

In January 2010, a lawsuit was filed in the U.S. District Court for the Middle District of North Carolina by

two leaders alleging violations of certain federal and North Carolina wage and hour laws on behalf of

themselves, and, if approved by the Court, other leaders and receptionists in North Carolina since January 25,

2007. In this matter, the plaintiffs are seeking unpaid wages and certain other damages. Although the Company

F-24