Tyson Foods 2015 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2015 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

|

|

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Marketriskrelatingtoouroperationsresultsprimarilyfromchangesincommodityprices,interestratesandforeignexchangerates,aswellascreditrisk

concentrations.Toaddresscertainoftheserisks,weenterintovariousderivativetransactionsasdescribedbelow.Ifaderivativeinstrumentisaccountedforasa

hedge,dependingonthenatureofthehedge,changesinthefairvalueoftheinstrumenteitherwillbeoffsetagainstthechangeinfairvalueofthehedgedassets,

liabilitiesorfirmcommitmentsthroughearnings,orberecognizedinothercomprehensiveincome(loss)untilthehedgeditemisrecognizedinearnings.The

ineffectiveportionofaninstrument’schangeinfairvalueisrecognizedimmediately.Additionally,weholdcertainpositions,primarilyingrainandlivestock

futuresthateitherdonotmeetthecriteriaforhedgeaccountingorarenotdesignatedashedges.Withtheexceptionofnormalpurchasesandnormalsalesthatare

expectedtoresultinphysicaldelivery,werecordthesepositionsatfairvalue,andtheunrealizedgainsandlossesarereportedinearningsateachreportingdate.

Changesinmarketvalueofderivativesusedinourriskmanagementactivitiesrelatingtoforwardsalescontractsarerecordedinsales.Changesinmarketvalueof

derivativesusedinourriskmanagementactivitiessurroundinginventoriesonhandoranticipatedpurchasesofinventoriesarerecordedincostofsales.

Thesensitivityanalysespresentedbelowarethemeasuresofpotentiallossesoffairvalueresultingfromhypotheticalchangesinmarketpricesrelatedto

commodities.Sensitivityanalysesdonotconsidertheactionswemaytaketomitigateourexposuretochanges,nordotheyconsidertheeffectssuchhypothetical

adversechangesmayhaveonoveralleconomicactivity.Actualchangesinmarketpricesmaydifferfromhypotheticalchanges.

Commodities Risk: Wepurchasecertaincommodities,suchasgrainsandlivestockinthecourseofnormaloperations.Aspartofourcommodityrisk

managementactivities,weusederivativefinancialinstruments,primarilyfuturesandoptions,toreducetheeffectofchangingpricesandasamechanismto

procuretheunderlyingcommodity.However,asthecommoditiesunderlyingourderivativefinancialinstrumentscanexperiencesignificantpricefluctuations,any

requirementtomark-to-marketthepositionsthathavenotbeendesignatedordonotqualifyashedgescouldresultinvolatilityinourresultsofoperations.

Contracttermsofahedgeinstrumentcloselymirrorthoseofthehedgeditemprovidingahighdegreeofriskreductionandcorrelation.Contractsdesignatedand

highlyeffectiveatmeetingthisriskreductionandcorrelationcriteriaarerecordedusinghedgeaccounting.Thefollowingtablepresentsasensitivityanalysis

resultingfromahypotheticalchangeof10%inmarketpricesasofOctober3,2015,andSeptember27,2014,onthefairvalueofopenpositions.Thefairvalueof

suchpositionsisasummationofthefairvaluescalculatedforeachcommoditybyvaluingeachnetpositionatquotedfuturesprices.Themarketriskexposure

analysisincludedhedgeandnon-hedgederivativefinancialinstruments.

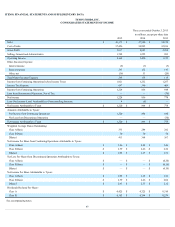

Effectof10%changeinfairvalue inmillions

2015

2014

Livestock:

Cattle $ 13

$ 42

Hogs 12

32

Grain 3

10

Interest Rate Risk: AtOctober3,2015,wehadvariableratedebtof$1,057millionwithaweightedaverageinterestrateof1.5%.Ahypothetical10%increase

ininterestrateseffectiveatOctober3,2015,andSeptember27,2014,wouldhaveaminimaleffectoninterestexpense.

Additionally,changesininterestratesimpactthefairvalueofourfixed-ratedebt.AtOctober3,2015,wehadfixed-ratedebtof$5,668millionwithaweighted

averageinterestrateof4.4%.Marketriskforfixed-ratedebtisestimatedasthepotentialincreaseinfairvalue,resultingfromahypothetical10%decreasein

interestrates.Ahypothetical10%decreaseininterestrateswouldhaveincreasedthefairvalueofourfixed-ratedebtbyapproximately$87millionatOctober3,

2015,and$109millionatSeptember27,2014.Thefairvaluesofourdebtwereestimatedbasedonquotedmarketpricesand/orpublishedinterestrates.

Wehaveinterestrateriskassociatedwithourpensionandpost-retirementbenefitobligations.Changesininterestratesimpacttheliabilitiesassociatedwiththese

benefitplansaswellastheamountofincomeorexpenserecognizedfortheseplans.Declinesinthevalueoftheplanassetscoulddiminishthefundedstatusofthe

pensionplansandpotentiallyincreasetherequirementstomakecashcontributionstotheseplans.SeePartII,Item8,NotestoConsolidatedFinancialStatements,

Note15:PensionsandOtherPostretirementBenefitsforadditionalinformation.

Foreign Currency Risk: Wehaveforeignexchangeexposurefromfluctuationsinforeigncurrencyexchangeratesprimarilyasaresultofcertainreceivableand

payablebalances.TheprimarycurrencieswehaveexposuretoaretheBrazilianreal,theBritishpoundsterling,theCanadiandollar,theChineserenminbi,the

Europeaneuro,theJapaneseyenandtheMexicanpeso.Weperiodicallyenterintoforeignexchangeforwardandoptioncontractstohedgesomeportionofour

foreigncurrencyexposure.Ahypothetical10%changeinforeignexchangerateseffectiveatOctober3,2015,andSeptember27,2014,relatedtotheforeign

exchangeforwardandoptioncontractswouldhavea$3millionand$9millionimpact,respectively,onpretaxincome.

43