Tyson Foods 2015 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2015 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

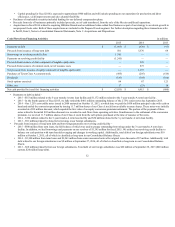

|

|

Impairment of goodwill and indefinite life intangible assets

Description: Goodwillisevaluatedforimpairmentbyfirstperformingaqualitativeassessmenttodeterminewhetheraquantitativegoodwilltestisnecessary.Ifit

isdetermined,basedonqualitativefactors,thefairvalueofthereportingunitmaybemorelikelythannotlessthancarryingamountorifsignificantchangesto

macro-economicfactorsrelatedtothereportingunithaveoccurredthatcouldmateriallyimpactfairvalue,aquantitativegoodwillimpairmenttestwouldbe

required.Wecanelecttoforgothequalitativeassessmentandperformthequantitativetest.

Thequantitativegoodwillimpairmenttestisperformedusingatwo-stepprocess.Thefirststepistoidentifyifapotentialimpairmentexistsbycomparingthefair

valueofareportingunitwithitscarryingamount,includinggoodwill.Ifthefairvalueofareportingunitexceedsitscarryingamount,goodwillofthereporting

unitisnotconsideredtohaveapotentialimpairmentandthesecondstepofthequantitativeimpairmenttestisnotnecessary.However,ifthecarryingamountofa

reportingunitexceedsitsfairvalue,thesecondstepisperformedtodetermineifgoodwillisimpairedandtomeasuretheamountofimpairmentlosstorecognize,

ifany.

Thesecondstepcomparestheimpliedfairvalueofgoodwillwiththecarryingamountofgoodwill.Iftheimpliedfairvalueofgoodwillexceedsthecarrying

amount,thengoodwillisnotconsideredimpaired.However,ifthecarryingamountofgoodwillexceedstheimpliedfairvalue,animpairmentlossisrecognizedin

anamountequaltothatexcess.

Theimpliedfairvalueofgoodwillisdeterminedinthesamemannerastheamountofgoodwillrecognizedinabusinesscombination(i.e.,thefairvalueofthe

reportingunitisallocatedtoalltheassetsandliabilities,includinganyunrecognizedintangibleassets,asifthereportingunithadbeenacquiredinabusiness

combinationandthefairvalueofthereportingunitwasdeterminedastheexitpriceamarketparticipantwouldpayforthesamebusiness).

Forindefinitelifeintangibleassets,aqualitativeassessmentcanalsobeperformedtodeterminewhethertheexistenceofeventsandcircumstancesindicatesitis

morelikelythannotanintangibleassetisimpaired.Similartogoodwill,wecanalsoelecttoforgothequalitativetestforindefinitelifeintangibleassetsand

performthequantitativetest.Uponperformingthequantitativetest,ifthecarryingvalueoftheintangibleassetexceedsitsfairvalue,animpairmentlossis

recognizedinanamountequaltothatexcess.Weelectedtoforgothequalitativeassessmentsonourindefinitelifeintangibleassetsforthefiscal2015impairment

test.

Wehaveelectedtomakethefirstdayofthefourthquartertheannualimpairmentassessmentdateforgoodwillandindefinitelifeintangibleassets.However,we

couldberequiredtoevaluatetherecoverabilityofgoodwillandindefinitelifeintangibleassetspriortotherequiredannualassessmentif,amongotherthings,we

experiencedisruptionstothebusiness,unexpectedsignificantdeclinesinoperatingresults,divestitureofasignificantcomponentofthebusinessorasustained

declineinmarketcapitalization.

Judgments and Uncertainties: Weestimatethefairvalueofourreportingunits,usingvariousvaluationtechniques,withtheprimarytechniquebeinga

discountedcashflowanalysis,whichusessignificantunobservableinputs,orLevel3inputs,asdefinedbythefairvaluehierarchy.Adiscountedcashflow

analysisrequiresustomakevariousjudgmentalassumptionsaboutsales,operatingmargins,growthratesanddiscountrates.

Weincludeassumptionsaboutsales,operatingmarginsandgrowthrateswhichconsiderourbudgets,businessplansandeconomicprojections,andarebelievedto

reflectmarketparticipantviewswhichwouldexistinanexittransaction.Assumptionsarealsomadeforvaryingperpetualgrowthratesforperiodsbeyondthe

long-termbusinessplanperiod.Generally,weutilizenormalizedoperatingmarginassumptionsbasedonfutureexpectationsandoperatingmarginshistorically

realizedinthereportingunits'industries.Forthefiscal2015impairmenttestofmaterialreportingunits,ourBeefandPreparedFoodsreportingunitsutilized

operatingmarginsinfutureyearsinexcessoftheoperatingmarginrealizedinthemostrecentyear.

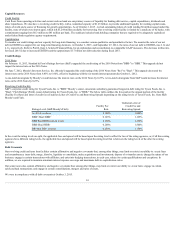

OurBeefreportingunit,whichisourBeefoperatingsegment,hadgoodwillatOctober3,2015,totaling$676million.Wegenerallyassumedoperatingmarginsin

futureyearswouldbeinournormalizedrangeof1.5%to3%,aswebelievethisisconsistentwithmarketparticipantviewsinanexittransaction.Hadweassumed

futureoperatingmarginsconsistentwiththoserealizedinthecurrentfiscalyear,wewouldhavefailedthefirststepoftheannualimpairmenttest,whichwould

haverequiredthesecondsteptobeperformedandmayhaveresultedinamaterialgoodwillimpairmentloss.ThecurrentyearBeefreportingunitresultswerenot

indicativeoffuturemarketparticipantexpectationsinanexittransaction,primarilyduetounusualitemsinfiscal2015includingunfavorablemarketconditions

associatedwithatemporarydeclineinsupplywhichdroveuplivecattleprices,exportmarketdisruptions,andlossesfrommark-to-marketopenderivative

positionsandlower-of-cost-or-marketinventoryadjustmentsduetoalargeandrapiddeclineinlivecattlefuturesinSeptemberoffiscal2015.Topassthefirststep

oftheannualimpairmenttestinfiscal2015,theBeefreportingunit’sprojectedoperatingmarginshadtoaverage1.2%(breakeven).Although,theBeefreporting

unit’sactualperformanceinfiscal2015wasbelowthisamount,ithasperformedabovethe1.2%breakevenoperatingmarginlevelineachoftheprevioussix

yearsandisexpectedtoperformatorabovethislevelinfiscal2016.ValuingtheBeefreportingunitutilizingprojectedoperatingmarginsaveraginglessthan

1.2%(breakeven),ora62%increaseinthediscountrateusedinfiscal2015,wouldhavecausedthecarryingvalueoftheBeefreportingunittobeinexcessoffair

value,whichwouldhaverequiredthesecondsteptobeperformed.

41