TCF Bank 2011 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2011 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

1972

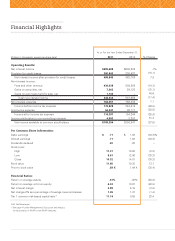

In 1972, TCF eclipsed $1 billion in total assets. Today, TCF

has nearly $19 billion in total assets including a loan and lease

portfolio that is well-diversied by both type and geography.

Retail lending loan balances totaled

$6.9 billion at year-end, down 3.7

percent from 2010. With the continued

depressed home values and a more

competitive environment for borrowers

who meet TCF’s underwriting criteria,

we have reduced the consumer real

estate portfolio and made investments

in other higher-yielding asset catego-

ries. Despite the current economic

conditions, TCF continued to fund new

consumer real estate loans to credit-

worthy customers during 2011. The

new loans have performed well with

low delinquencies and minimal

charge-offs. We expect to have more

opportunities to add loans in this

portfolio as home values stabilize.

Wholesale Banking

TCF’s Wholesale Banking division

consists of commercial banking and

specialty finance (TCF Equipment

Finance, Winthrop Resources

Corporation, TCF Inventory Finance

and Gateway One). Loan balances

decreased 5.4 percent in our commercial

portfolio, which totaled $3.4 billion at

year-end, largely due to higher levels

of payments exceeding increased

new origination volume. Demand

for commercial loans has remained

somewhat tempered by the sluggish

economy but we are seeing some signs

of growing demand. We saw many of

our peers being much more competi-

tive from a pricing perspective on the

commercial deals that were available

during the year. As a result of our

various avenues for asset growth

in specialty finance, we have not

been forced to compete for deals

with substandard pricing. Overall, our

commercial portfolio is performing well

in the current economic environment

largely as a result of our conservative

underwriting philosophy and our

commitment to relationship banking

with long-term customers.

Loan and lease balances in specialty

finance decreased 4.5 percent to $3.8

billion at year-end. In specialty finance,

home to TCF’s highest yielding loans

and leases, we were able to minimize

concentration risk by diversifying our

businesses by industry, transaction

size, geography and collateral type.

We continue to emphasize specialty

finance as a key vehicle for asset

growth because of our proven expertise

in acquiring, integrating and operating

these national niche businesses.

TCF’s leasing and equipment finance

business balances decreased by

.4 percent from 2010 as past portfolio

purchases continue to run off. Excluding

this run-off activity, the core portfolio

continues to grow as balances increased

6 percent from 2010. Our $3.1 billion

leasing and equipment finance portfolio

is well-diversified by equipment type,

transaction size and geography.

Our leasing and equipment finance

operation, which is comprised of TCF

Equipment Finance and Winthrop

Resources Corporation, is the 28th

largest in the U.S. and the 13th largest

bank-affiliated leasing company in

the U.S. Despite the overall decrease

in leasing and equipment finance

balances, 2011 originations were up

19.2 percent from 2010. Future growth

opportunities are strong as we have an

uninstalled backlog of $455.3 million

at year-end. The portfolio is currently

yielding 6 percent.

TCF Inventory Finance, Inc. (TCFIF)

continues to be a business where we

052011 Annual Report