Radio Shack 2010 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2010 Radio Shack annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

54

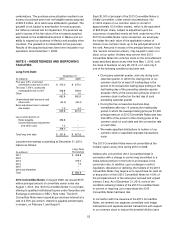

conversion of the 2013 Convertible Notes (collectively

referred to as the “Call Spread Transactions”). The

convertible note hedges and warrants will generally have

the effect of increasing the economic conversion price of

the 2013 Convertible Notes to $36.60 per share of our

common stock, representing a 100% conversion premium

based on the closing price of our common stock on August

12, 2008. See Note 6 - “Stockholders’ Equity,” for more

information on the Call Spread Transactions.

Because the principal amount of the 2013 Convertible

Notes will be settled in cash upon conversion, the 2013

Convertible Notes will only affect diluted earnings per share

when the price of our common stock exceeds the

conversion price (initially $24.25 per share). We will include

the effect of the additional shares that may be issued from

conversion in our diluted net income per share calculation

using the treasury stock method.

When accounting for the 2013 Convertible Notes, we apply

accounting guidance related to the accounting for

convertible debt instruments that may be settled in cash

upon conversion. This guidance requires us to account

separately for the liability and equity components of our

convertible notes in a manner that reflects our nonconvertible

debt borrowing rate when interest cost is recognized in

subsequent periods. This guidance requires bifurcation of a

component of the debt, classification of that component in

equity, and then accretion of the resulting discount on the

debt as part of interest expense being reflected in the income

statement.

Accordingly, we recorded an adjustment to reduce the

carrying value of our 2013 Convertible Notes by $73.0

million and recorded this amount in stockholders’ equity.

This adjustment was based on the calculated fair value of a

similar debt instrument in August 2008 (at issuance) that

did not have an associated equity component. The annual

interest rate calculated for a similar debt instrument in

August 2008 was 7.6%. The resulting discount is being

amortized to interest expense over the remaining term of

the convertible notes. The carrying value of the 2013

Convertible Notes was $330.8 million and $315.8 million at

December 31, 2010 and 2009, respectively. We recognized

interest expense of $9.4 million in both 2010 and 2009

related to the stated 2.50% coupon. We recognized non-

cash interest expense of $15.0 million, $13.8 million, and

$5.0 million in 2010, 2009 and 2008, respectively, for the

amortization of the discount on the liability component.

Debt issuance costs of $7.5 million were capitalized and

are being amortized to interest expense over the term of

the 2013 Convertible Notes. Unamortized debt issuance

costs were $3.7 million at December 31, 2010. Debt

issuance costs of $1.9 million were related to the equity

component and were recorded as a reduction of additional

paid-in capital.

For federal income tax purposes, the issuance of the 2013

Convertible Notes and the purchase of the convertible note

hedges are treated as a single transaction whereby we are

considered to have issued debt with an original issue

discount. The amortization of this discount in future periods

is deductible for tax purposes.

2011 Long-Term Notes: On May 11, 2001, we issued

$350 million of 10-year 7.375% notes (“2011 Notes”) in a

private offering to qualified institutional buyers under SEC

Rule 144A. In August 2001, under the terms of an

exchange offering filed with the SEC, we exchanged

substantially all of these notes for a similar amount of

publicly registered notes. The exchange resulted in

substantially all of the notes becoming registered with the

SEC and did not result in additional debt being issued.

The annual interest rate on the notes is 7.375% per annum,

with interest payable on November 15 and May 15 of each

year. The notes contain certain non-financial covenants and

mature on May 15, 2011. In September 2009, we completed

a tender offer to purchase for cash any and all of these

notes. Upon expiration of the offer, $43.2 million of the

aggregate outstanding principal amount of the notes was

validly tendered and accepted. We paid a total of $46.6

million, which consisted of the purchase price of $45.4 million

for the tendered notes plus $1.2 million in accrued and

unpaid interest, to the holders of the tendered notes. We

incurred $0.2 million in expenses and adjusted the carrying

value of the tendered notes by an incremental $0.8 million to

reflect a proportionate write-off of the balance associated

with our fair value hedge included in long-term debt. This

transaction resulted in a loss of $1.6 million classified as

other loss on our consolidated statements of income.

A portion of these notes were hedged by our interest rate

swaps. Upon repurchase of these notes, we were required to

discontinue the hedge accounting treatment associated with

these derivative instruments, which used the short-cut

method. The remaining balance associated with our fair

value hedge was recorded as an adjustment to the carrying

value of these notes and is being amortized to interest

expense over the remaining term of the notes. At December

31, 2010, this carrying value adjustment was $1.2 million.

See Note 11 - “Derivative Financial Instruments,” for more

information on our interest rate swaps.

On January 4, 2011, we announced our intention to redeem

any and all outstanding 2011 Notes on March 4, 2011. See

Note 15 - “Subsequent Events” for more information.

Credit Facilities: Our $325 million credit facility provided

us a source of liquidity. Interest charges under this facility

were derived using a base LIBOR rate plus a margin that

changed based on our credit ratings. This facility had

customary terms and covenants, and we were in

compliance with these covenants at December 31, 2010.