Quest Diagnostics 2012 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2012 Quest Diagnostics annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

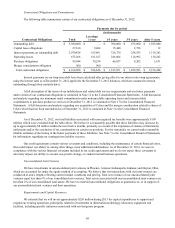

|

|

64

The increase in the effective income tax rate for the year ended December 31, 2011 is primarily due to the Medi-Cal

charge recorded in the first quarter of 2011 associated with the California Lawsuit (see Note 17 to the Consolidated Financial

Statements), a portion for which a tax benefit has not been recorded.

Income tax expense for the year ended December 31, 2011 included discrete income tax benefits of $18.2 million,

primarily associated with certain state tax planning initiatives and the favorable resolution of certain tax contingencies. For the

year ended December 31, 2010, income tax expense included discrete income tax benefits of $22.1 million, primarily

associated with the favorable resolution of certain tax contingencies.

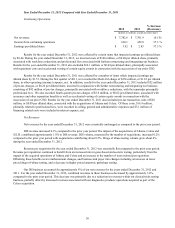

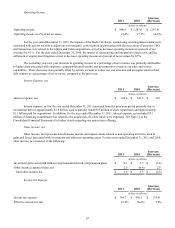

Discontinued Operations

Discontinued operations includes HemoCue, OralDNA and NID, a test kit manufacturing subsidiary. The results of

operations for HemoCue, OralDNA and NID have been classified as discontinued operations for all periods presented. See

Note 18 for further details regarding discontinued operations.

The following table summarizes our income from discontinued operations, net of taxes:

Increase

(Decrease) 2011 2010

(dollars in millions)

Net revenues $ 118.6 $ 108.8 $ 9.8

Income from discontinued operations before taxes 7.1 9.3 (2.2)

Income tax benefit (4.5)(2.8)(1.7)

Income from discontinued operations, net of taxes $ 11.6 $ 12.1 $ (0.5)

Quantitative and Qualitative Disclosures About Market Risk

We address our exposure to market risks, principally the market risk of changes in interest rates, through a controlled

program of risk management that includes the use of derivative financial instruments. We do not hold or issue derivative

financial instruments for speculative purposes. We believe that our exposures to foreign exchange impacts and changes in

commodity prices are not material to our consolidated financial condition or results of operations. See Note 13 to the

Consolidated Financial Statements for additional discussion of our financial instruments and hedging activities.

At December 31, 2012 and 2011, the fair value of our debt was estimated at approximately $3.8 billion and $4.4

billion, respectively, using quoted active market prices and yields for the same or similar types of borrowings, taking into

account the underlying terms of the debt instruments. At December 31, 2012 and 2011, the estimated fair value exceeded the

carrying value of the debt by $481 million and $387 million, respectively. A hypothetical 10% increase in interest rates

(representing 48 basis points and 41 basis points at December 31, 2012 and 2011, respectively) would potentially reduce the

estimated fair value of our debt by approximately $98 million and $112 million at December 31, 2012 and 2011, respectively.

Borrowings under our floating rate senior notes due 2014, our senior unsecured revolving credit facility and our

secured receivables credit facility are subject to variable interest rates. Interest on our secured receivables credit facility is

based on rates that are intended to approximate commercial paper rates for highly-rated issuers. Interest on our senior

unsecured revolving credit facility is subject to a pricing schedule that can fluctuate based on changes in our credit ratings. As

such, our borrowing cost under this credit arrangement will be subject to both fluctuations in interest rates and changes in our

credit ratings. At December 31, 2012, the borrowing rates under these debt instruments were: for our floating rate senior notes

due 2014, LIBOR plus 0.85%; for our senior unsecured revolving credit facility, LIBOR plus 1.125%; and for our secured

receivables credit facility, 0.97%. At December 31, 2012, the weighted average LIBOR was 0.3%. As of December 31, 2012,

$200 million was outstanding under our floating rate senior notes due 2014. There were no borrowings outstanding under our

$525 million secured receivables credit facility or our $750 million senior unsecured revolving credit facility as of

December 31, 2012.

We seek to mitigate the variability in cash outflows that result from changes in interest rates by maintaining a balanced

mix of fixed-rate and variable-rate debt obligations. In order to achieve this objective, we have entered into interest rate swaps.

Interest rate swaps involve the periodic exchange of payments without the exchange of underlying principal or notional

amounts. Net settlements are recognized as an adjustment to interest expense.