Quest Diagnostics 2012 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2012 Quest Diagnostics annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

|

|

F- 31

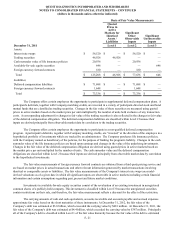

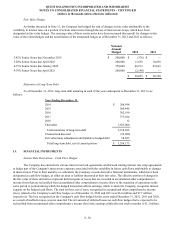

Interest Rate Derivatives – Fair Value Hedges

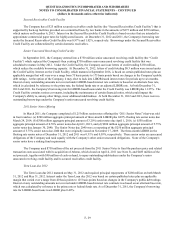

The Company maintains various fixed-to-variable interest rate swaps to convert a portion of the Company's long-term

debt into variable interest rate debt. These derivative financial instruments are accounted for as fair value hedges of a portion of

the Senior Notes due 2016 and a portion of the Senior Notes due 2020. In prior years, the Company entered into various fixed-

to-variable interest rate swap agreements with an aggregate notional amount of $550 million and variable interest rates based on

six-month LIBOR plus 0.54% and one-month LIBOR plus 1.33%. In July 2012, the Company monetized the value of these

interest rate swap assets by terminating the hedging instruments. The asset value, including accrued interest through the date of

termination, was $71.8 million and the amount to be amortized as a reduction of interest expense over the remaining terms of

the hedged debt instruments was $65.2 million. Immediately after the termination of these interest rate swaps, the Company

entered into new fixed-to-variable interest rate swap agreements on the same Senior Notes. The fixed-to-variable interest rate

swap agreements that the Company entered into in July 2012 have an aggregate notional amount of $550 million and variable

interest rates based on six-month LIBOR plus 2.3% and one-month LIBOR plus 3.6%. During the fourth quarter of 2012, the

Company entered into additional fixed-to-variable interest rate swap agreements with an aggregate notional amount of $400

million and variable interest rates based on one-month LIBOR plus a spread ranging from 3.4% to 5.1%. These derivative

financial instruments are accounted for as fair value hedges on a portion of the Senior Notes due 2015 and a portion of the

Senior Notes due 2021.

The interest rate swaps associated with the Senior Notes due 2016 are classified as assets with fair values of $0.8

million and $10.9 million at December 31, 2012 and 2011, respectively. The interest rate swaps associated with the Senior

Notes due 2015, 2020 and 2021 are classified as liabilities with an aggregate fair value of $3.1 million at December 31, 2012.

The interest rate swaps associated with the Senior Notes due 2020 were classified as assets with a fair value of $45.7 million at

December 31, 2011. Since inception, the fair value hedges have been effective or highly effective; therefore, there is no impact

on earnings for the years ended December 31, 2012, 2011 and 2010 as a result of hedge ineffectiveness.

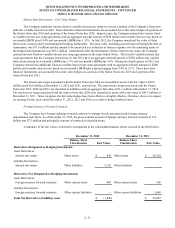

Foreign Currency Forward Contracts

The Company uses foreign exchange forward contracts to manage its risk associated with foreign currency

denominated cash flows. As of December 31, 2012, the gross notional amount of foreign currency forward contracts in U.S.

dollars was $7.3 million and principally consists of contracts in Swedish krona.

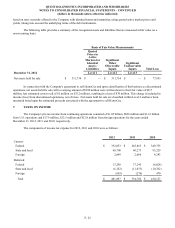

A summary of the fair values of derivative instruments in the consolidated balance sheets is stated in the table below:

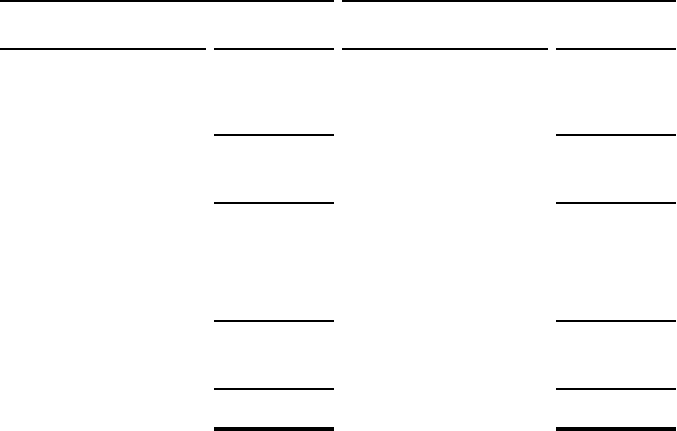

December 31, 2012 December 31, 2011

Balance Sheet

Classification Fair Value

Balance Sheet

Classification Fair Value

Derivatives Designated as Hedging Instruments

Asset Derivatives:

Interest rate swaps Other assets $ 830 Other assets $ 56,520

Liability Derivatives:

Interest rate swaps Other liabilities 3,129 Other liabilities —

Derivatives Not Designated as Hedging Instruments

Asset Derivatives:

Foreign currency forward contracts Other current assets 403 Other current assets 180

Liability Derivatives:

Foreign currency forward contracts Other current liabilities — Other current liabilities 1,648

Total Net Derivatives (Liability) Asset $(1,896) $ 55,052

QUEST DIAGNOSTICS INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS – CONTINUED

(dollars in thousands unless otherwise indicated)