Pottery Barn 2011 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2011 Pottery Barn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

NEW ACCOUNTING PRONOUNCEMENTS

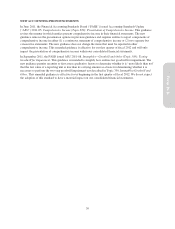

In June 2011, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update

(“ASU”) 2011-05, Comprehensive Income (Topic 220): Presentation of Comprehensive Income. This guidance

revises the manner in which entities present comprehensive income in their financial statements. The new

guidance removes the presentation options in previous guidance and requires entities to report components of

comprehensive income in either (1) a continuous statement of comprehensive income or (2) two separate but

consecutive statements. The new guidance does not change the items that must be reported in other

comprehensive income. This amended guidance is effective for our first quarter of fiscal 2012 and will only

impact the presentation of comprehensive income within our consolidated financial statements.

In September 2011, the FASB issued ASU 2011-08, Intangibles—Goodwill and Other (Topic 350): Testing

Goodwill for Impairment. This guidance is intended to simplify how entities test goodwill for impairment. The

new guidance permits an entity to first assess qualitative factors to determine whether it is “more likely than not”

that the fair value of a reporting unit is less than its carrying amount as a basis for determining whether it is

necessary to perform the two-step goodwill impairment test described in Topic 350, Intangibles-Goodwill and

Other. This amended guidance is effective for us beginning in the first quarter of fiscal 2012. We do not expect

the adoption of this standard to have a material impact on our consolidated financial statements.

39

Form 10-K