Panera Bread 2004 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2004 Panera Bread annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

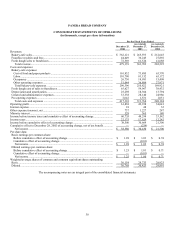

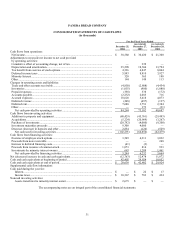

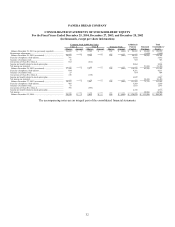

disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses

during the reporting period. Actual results could differ from those estimates.

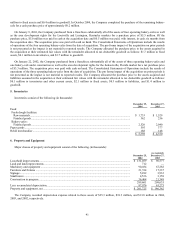

Cash and Cash Equivalents

The Company considers all highly liquid investments with a maturity at the time of purchase of three months or less to be cash

equivalents.

Investments in Government Securities

Investments of $28.4 million and $9.0 million at December 25, 2004 and December 27, 2003, respectively, consist of United

States Treasury notes and mortgage-backed government notes. During 2004, $9.3 million of investments matured or were called by

the issuer and $28.8 million of investments were purchased by the Company. The Company recognized interest income on these

investments of $0.8 million, $0.2 million and $0.1 million, which is net of premium amortization of $0.1 million during fiscal year

2004, 2003 and 2002, respectively, and is classified in “Other Income/Expense” in the Consolidated Statements of Operations. The

Company’s investments are classified as short-term or long-term in the accompanying consolidated balance sheets based upon their

stated maturity dates which range from June 2005 to April 2007.

Management designates the appropriate classification of its investments at the time of purchase based upon its intended holding

period. At December 25, 2004, all investments are classified as held-to-maturity as the Company has the intent and ability to hold the

securities to maturity. Held-to-maturity securities are stated at amortized cost, adjusted for amortization of premiums to maturity using

the effective interest method, which approximates fair value at December 25, 2004.

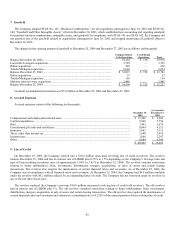

Trade and Other Accounts Receivable

Trade accounts receivable at fiscal year-end consist primarily of amounts due to the Company from its 39 franchise groups for

purchases of fresh dough from the Company’s fresh dough facilities and royalties due to the Company from franchisee sales. The

Company does not require collateral and maintains reserves for potential uncollectible accounts based on historical losses and existing

economic conditions, when relevant. The allowance for doubtful accounts at December 25, 2004 and December 27, 2003 was $0.03

million and $0.05 million, respectively. Other accounts receivable consists primarily of tenant allowances due from landlords.

Inventories

Inventories, which consist of food products, paper goods and supplies, and promotional items, are valued at the lower of cost or

market, determined under the first-in, first-out method.

Property and Equipment

Property, equipment, and leaseholds are stated at cost. Depreciation is provided using the straight-line method over the estimated

useful lives of the assets. Leasehold improvements are amortized using the straight-line method over the shorter of their estimated

useful lives or the related reasonably assured lease term. The estimated useful lives used for financial statement purposes are:

Leasehold improvements...................................................................................................................................................... 15-20 years

Machinery and equipment .................................................................................................................................................... 5-10 years

Furniture and fixtures ........................................................................................................................................................... 3-7 years

Signage ................................................................................................................................................................................. 6 years

Interest, to the extent it is incurred, is capitalized when incurred in connection with the construction of new locations or facilities.

The capitalized interest is recorded as part of the asset to which it relates and is amortized over the asset’s estimated useful life. No

interest was incurred for such purposes in 2004, 2003, or 2002.

Upon retirement or sale, the cost of assets disposed of and their related accumulated depreciation are removed from the accounts.

Any resulting gain or loss is credited or charged to operations. Maintenance and repairs are charged to expense when incurred, while

betterments are capitalized.

34