Panera Bread 2003 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2003 Panera Bread annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

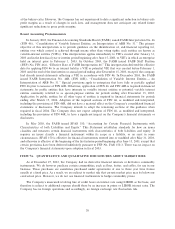

PANERA BREAD COMPANY

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS Ì (Continued)

Interest, to the extent it is incurred, is capitalized when incurred in connection with the construction of

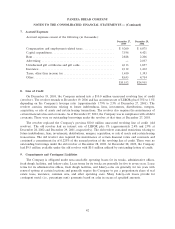

new locations or facilities. The capitalized interest is recorded as part of the asset to which it relates and is

amortized over the asset's estimated useful life. No interest was incurred for such purposes in 2003, 2002, or

2001.

Upon retirement or sale, the cost of assets disposed of and their related accumulated depreciation are

removed from the accounts. Any resulting gain or loss is credited or charged to operations. Maintenance and

repairs are charged to expense when incurred, while betterments are capitalized.

Goodwill

Intangible assets consist of goodwill arising from the excess of cost over the fair value of net assets

acquired from the acquisitions of the Saint Louis Bread Company, franchisee bakery-cafes, and a franchisee

fresh dough facility.

The Company adopted Statement of Financial Accounting Standards No. 141 (""SFAS 141''), ""Business

Combinations'' for all acquisitions subsequent to June 30, 2001 and ""SFAS No. 142, ""Goodwill and Other

Intangible Assets,'' eÅective December 30, 2001, which established new accounting and reporting standards

for purchase business combinations, intangible assets and goodwill. In compliance with SFAS 141 and

SFAS 142, the Company did not amortize any of the goodwill related to acquisitions subsequent to June 30,

2001 and stopped amortizing all goodwill eÅective December 30, 2001. SFAS 142 requires goodwill and

indeÑnite-lived intangible assets recorded in the Ñnancial statements to be evaluated for impairment annually

or when events or circumstances occur indicating that goodwill might be impaired. The Company performs its

impairment assessment by comparing discounted cash Öows from acquired businesses with the carrying value

of the underlying net assets inclusive of goodwill. The Company completed the transitional impairment test as

of December 30, 2001, and our annual impairment tests as of the Ñrst day of the fourth quarter of 2002 and

2003, none of which identiÑed any impairment. Amortization expense was $1.0 million for the year ended

December 29, 2001.

Impairment of Long-Lived Assets

EÅective December 30, 2001, the Company adopted SFAS 144, ""Accounting for the Impairment of

Long-Lived Assets.'' In accordance with SFAS 144, the Company evaluates whether events and circum-

stances have occurred that indicate the remaining estimated useful life of long lived assets may warrant

revision or that the remaining balance of an asset may not be recoverable. The Company determines if there is

an impairment by comparing undiscounted cash Öows from the related long-lived assets of a bakery-cafe or

fresh dough facility with their respective carrying values. The amount of an impairment is determined by

comparing anticipated discounted future operating cash Öows from the related long-lived assets of a bakery-

cafe or a fresh dough facility with their respective carrying values. In performing this analysis, management

considers such factors as current results, trends, future prospects and other economic factors. No impairment

of long-lived assets was determined at December 27, 2003 and December 28, 2002.

Self-Insurance Reserves

The Company is self-insured for a signiÑcant portion of its workers' compensation and general, auto, and

property liability insurance. Liabilities associated with the risks that are retained by the Company are

estimated, in part, by considering historical claims experience of the Company and the industry and other

actuarial assumptions. The estimated accruals for these liabilities could be aÅected if future occurrences and

claims diÅer from these assumptions and historical trends. As of December 27, 2003 and December 28, 2002,

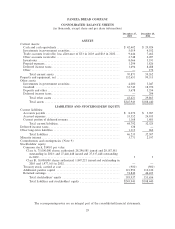

these reserves were $2.1 million and $1.4 million, respectively, and were included in accrued expenses in the

consolidated balance sheets.

35