Panera Bread 2003 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2003 Panera Bread annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

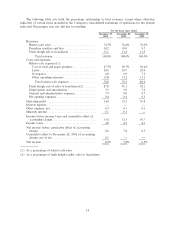

primarily due to the impact of a full year's depreciation of prior year's capital expenditures and increased

capital expenditures in the current year.

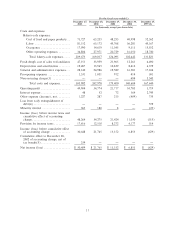

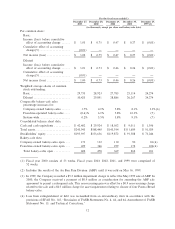

General and administrative expenses were $28.1 million, or 7.9% of total revenue, and $25.0 million, or

9.0% of total revenue, for the Ñfty-two weeks ended December 27, 2003 and December 28, 2002, respectively.

The decrease in the general and administrative expense rate between 2003 and 2002 results primarily from

higher revenues, which help leverage general and administrative expenses, and from decreased bonus costs.

Pre-opening expenses, which consist primarily of labor and food costs incurred during in-store training

and preparation for opening, exclusive of manager training costs which are included in other operating

expenses, of $1.5 million, or 0.4% of total revenue, for the Ñfty-two weeks ended December 27, 2003 were

consistent with the $1.1 million, or 0.4% of total revenue, of pre-opening expenses for the Ñfty-two weeks

ended December 28, 2002.

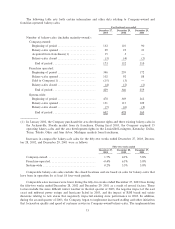

Operating ProÑt

Operating proÑt for the Ñfty-two weeks ended December 27, 2003 increased to $49.9 million, or 14.0% of

total revenue, from $34.8 million, or 12.5% of total revenue, for the Ñfty-two weeks ended December 28, 2002.

Operating proÑt for the Ñfty-two weeks ended December 27, 2003 rose as a result of operating leverage that

results from opening 29 Company bakery-cafes in 2003 as well as the factors described above.

Other Expense

Other expense for the Ñfty-two weeks ended December 27, 2003 increased to $1.2 million, or 0.3% of

total revenue, from $0.3 million, or 0.1% of total revenue, for the Ñfty-two weeks ended December 28, 2002.

The increase in other expense results primarily from increased operating fee payments to the minority interest

owner. See Note 12 for additional information.

Minority Interest

Minority interest represents the portion of the Company's operating proÑt that is attributable to the

ownership interest of our minority interest owner.

Income Taxes

The provision for income taxes increased to $17.6 million for the Ñfty-two weeks ended December 27,

2003 compared to $12.5 million for the Ñfty-two weeks ended December 28, 2002. The tax provisions for the

Ñfty-two weeks ended December 27, 2003 and December 28, 2002 reÖects a consistent combined federal,

state, and local eÅective tax rate of 36.5%.

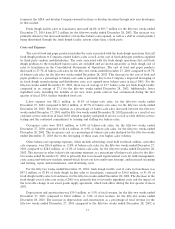

Income Before Cumulative EÅect of Accounting Change

Income before cumulative eÅect of accounting change for the Ñfty-two weeks ended December 27, 2003

increased $8.9 million, or 40.8%, to $30.6 million, or $1.01 per diluted share, compared to income before

cumulative eÅect of accounting change of $21.8 million, or $0.73 per diluted share, for the Ñfty-two weeks

ended December 28, 2002. The increase in income before cumulative eÅect of accounting change in 2003 was

primarily due to the operating leverage from the opening of 23 bakery-cafes in 2002 that were open for a full

year in 2003 and leverage from opening 29 bakery-cafes in 2003.

Cumulative EÅect of Accounting Change

EÅective December 29, 2002, the Company adopted the provisions of SFAS 143, ""Accounting for Asset

Retirement Obligations.'' SFAS 143 addresses Ñnancial accounting and reporting for obligations associated

with the retirement of tangible long-lived assets and the associated asset retirement costs. This Statement

requires the Company to record an estimate for costs of retirement obligations that may be incurred at the end

of lease terms of existing bakery-cafes or other facilities. Upon adoption of SFAS 143, the Company

recognized a one-time cumulative eÅect charge of approximately $0.2 million (net of deferred tax beneÑt of

18