Nordstrom 2014 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2014 Nordstrom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

Table of Contents

26

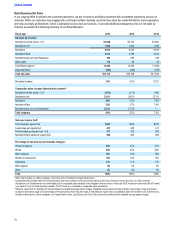

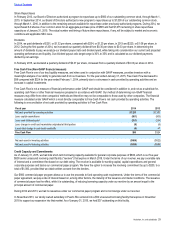

Return on Invested Capital (“ROIC”) (Non-GAAP financial measure)

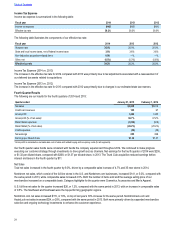

We believe that ROIC is a useful financial measure for investors in evaluating the efficiency and effectiveness of our use of capital and

believe ROIC is an important component of shareholders’ return over the long term. In addition, we incorporate ROIC in our executive

incentive compensation measures. For the 12 fiscal months ended January 31, 2015, our ROIC decreased to 12.6% compared with 13.6%

for the 12 fiscal months ended February 1, 2014. Our ROIC decreased compared with the prior year primarily due to the acquisition of Trunk

Club in addition to ongoing store expansion and increased technology investments.

ROIC is not a measure of financial performance under generally accepted accounting principles (“GAAP”) and should be considered in

addition to, and not as a substitute for, return on assets, net earnings, total assets or other financial measures prepared in accordance with

GAAP. Our method of determining non-GAAP financial measures may differ from other companies’ methods and therefore may not be

comparable to those used by other companies. The financial measure calculated under GAAP which is most directly comparable to ROIC is

return on assets. The following is a reconciliation of the components of ROIC and return on assets:

12 Fiscal months ended

January 31, 2015 February 1, 2014 February 2, 2013 January 28, 2012 January 29, 2011

Net earnings $720 $734 $735 $683 $613

Add: income tax expense 465 455 450 436 378

Add: interest expense 139 162 162 132 128

Earnings before interest and income tax

expense 1,324 1,351 1,347 1,251 1,119

Add: rent expense 137 125 105 78 62

Less: estimated depreciation on

capitalized operating leases1(74) (67) (56) (42) (32)

Net operating profit 1,387 1,409 1,396 1,287 1,149

Less: estimated income tax expense2(544)(539) (530) (501) (439)

Net operating profit after tax $843 $870 $866 $786 $710

Average total assets3$8,860 $8,398 $8,274 $7,890 $7,091

Less: average non-interest-bearing

current liabilities4(2,730) (2,430) (2,262) (2,041) (1,796)

Less: average deferred property

incentives3(502)(489) (494) (504) (487)

Add: average estimated asset base of

capitalized operating leases51,058 929 724 555 425

Average invested capital $6,686 $6,408 $6,242 $5,900 $5,233

Return on assets 8.1%8.7% 8.9% 8.7% 8.6%

ROIC 12.6%13.6% 13.9% 13.3% 13.6%

1 Capitalized operating leases is our best estimate of the asset base we would record for our leases that are classified as operating if they had met the criteria for a capital lease

or we had purchased the property. Asset base is calculated as described in footnote 5 below.

2 Based upon our effective tax rate multiplied by the net operating profit for the 12 fiscal months ended January 31, 2015, February 1, 2014, February 2, 2013, January 28, 2012

and January 29, 2011.

3 Based upon the trailing 12-month average.

4 Based upon the trailing 12-month average for accounts payable, accrued salaries, wages and related benefits, and other current liabilities.

5 Based upon the trailing 12-month average of the monthly asset base. The asset base for each month is calculated as the trailing 12 months of rent expense multiplied by eight.

The multiple of eight times rent expense is a commonly used method of estimating the asset base we would record for our capitalized operating leases described in footnote 1.