Nordstrom 2014 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2014 Nordstrom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

Table of Contents

Nordstrom, Inc. and subsidiaries 21

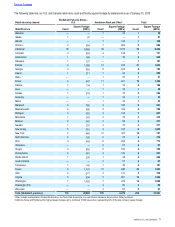

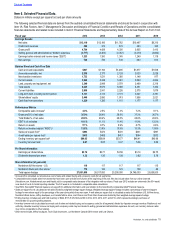

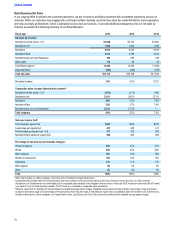

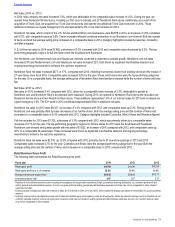

CREDIT SEGMENT

The Nordstrom credit and debit card products are designed to strengthen customer relationships and grow retail sales by providing loyalty

benefits, valuable services and payment products. We believe our credit business allows us to build deeper relationships with our customers

by fully integrating the Nordstrom Rewards program with our retail stores and providing better service, which in turn fosters greater customer

loyalty. Our cardholders tend to visit our stores more frequently and spend more with us than non-cardholders. Our Nordstrom private label

credit and debit cards can be used only at our Nordstrom full-line stores in the U.S., Nordstrom Rack stores and online at Nordstrom.com,

Nordstromrack.com and HauteLook (“inside volume”), while our Nordstrom Visa credit cards also may be used for purchases outside of

Nordstrom (“outside volume”). Cardholders participate in the Nordstrom Rewards program through which cardholders accumulate points for

their purchases. Upon reaching a certain points threshold, cardholders receive Nordstrom Notes®, which can be redeemed for goods or

services at Nordstrom full-line stores in the U.S. and Canada, Nordstrom Rack stores and at Nordstrom.com. Nordstrom Rewards customers

receive reimbursements for alterations, get Personal Triple Points days and have early access to sales events. With increased spending,

they can receive additional amounts of these benefits as well as access to exclusive fashion and shopping events.

In May 2014, we announced our plan to review options for a potential financial partner for our credit card receivables portfolio. We intend to

execute a transaction only if our strategic and financial requirements are met. In the event a transaction is finalized, we will classify the

relevant credit card receivables as held for sale, which could result in a gain or loss upon reclassification.

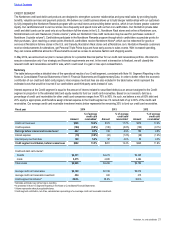

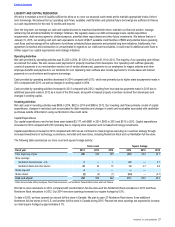

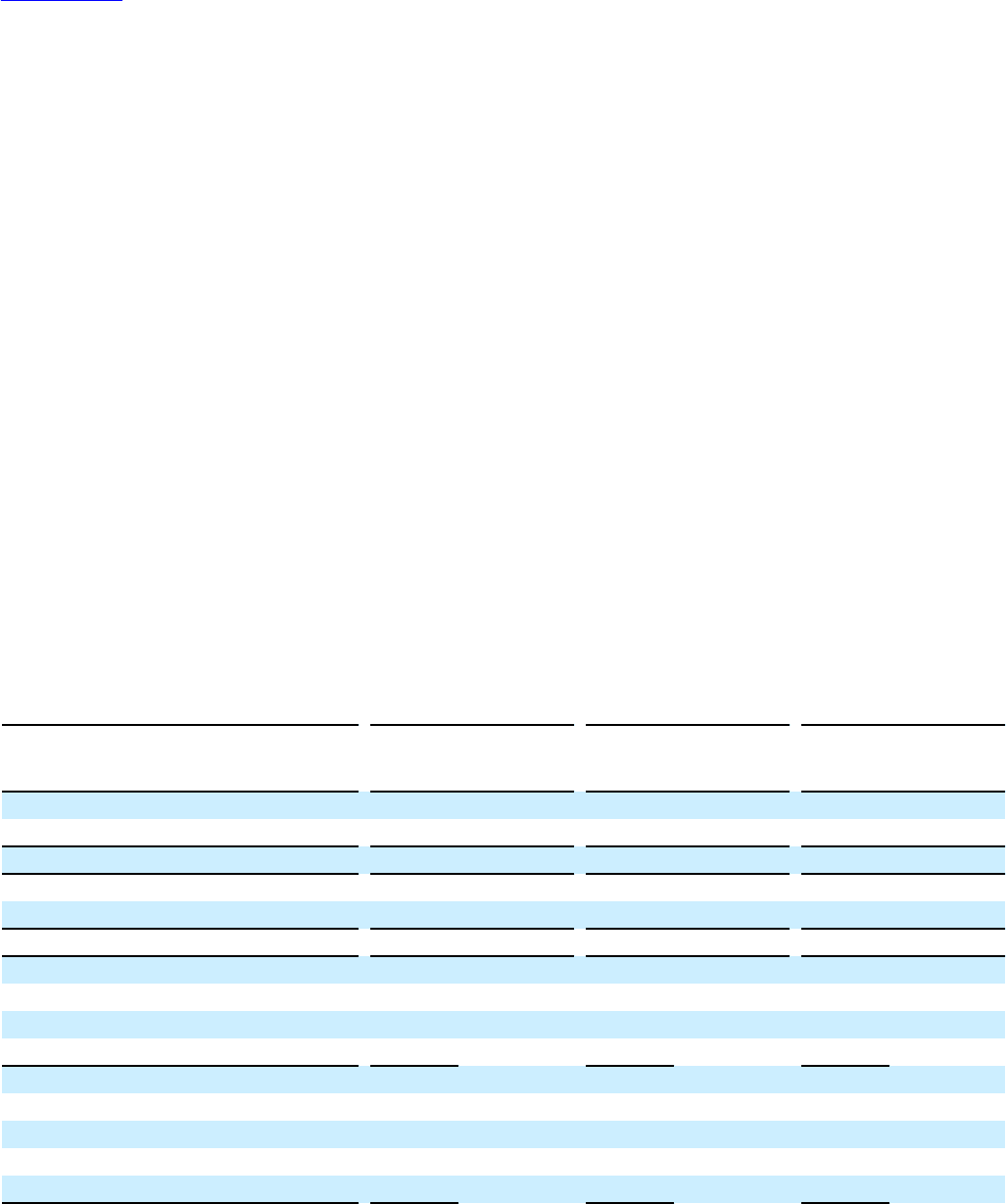

Summary

The table below provides a detailed view of the operational results of our Credit segment, consistent with Note 16: Segment Reporting in the

Notes to Consolidated Financial Statements of Item 8: Financial Statements and Supplementary Data. In order to better reflect the economic

contribution of our credit and debit card program, intercompany merchant fees are also included in the table below, which represent the

estimated costs that would be incurred if our cardholders used third-party cards instead of ours.

Interest expense at the Credit segment is equal to the amount of interest related to securitized debt plus an amount assigned to the Credit

segment in proportion to the estimated debt and equity needed to fund our credit card receivables. Based on our research, debt as a

percentage of credit card receivables for other credit card companies ranges from 70% to 90%. As such, we believe a mix of 80% debt and

20% equity is appropriate, and therefore assign interest expense to the Credit segment as if it carried debt of up to 80% of the credit card

receivables. Our average credit card receivable investment metric below represents the remaining 20% to fund our credit card receivables.

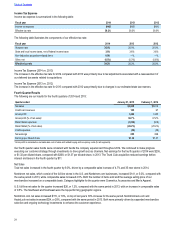

Fiscal year 2014 2013 2012

Amount

% of average

credit card

receivables1Amount

% of average

credit card

receivables1Amount

% of average

credit card

receivables1

Credit card revenues $396 18.2% $374 17.7% $372 17.9%

Credit expenses (194) (8.9%) (186) (8.8%) (190) (9.1%)

Earnings before interest and income taxes2202 9.3% 188 8.9% 182 8.8%

Interest expense (18) (0.8%) (24) (1.2%) (26) (1.2%)

Intercompany merchant fees 108 5.0% 97 4.6% 89 4.3%

Credit segment contribution, before income taxes $292 13.5% $261 12.4% $245 11.8%

Credit and debit card volume3:

Outside $4,331 $4,273 $4,305

Inside 5,475 4,935 4,484

Total volume $9,806 $9,208 $8,789

Average credit card receivables $2,169 $2,108 $2,076

Average credit card receivable investment 434 422 415

Credit segment contribution440.9% 38.2% 36.6%

1 Subtotals and totals may not foot due to rounding.

2 As presented in Note 16: Segment Reporting in the Notes to Consolidated Financial Statements.

3 Volume represents sales plus applicable taxes.

4 Credit segment contribution, net of tax, calculated as a percentage of our average credit card receivable investment.